Keeping track of the money your business owes its suppliers and vendors is crucial to its financial health and long-term viability. That’s why all businesses need an accounts payable reporting process that provides visibility into their cash flow and outstanding debts. We’ll explain accounts payable reporting, why it’s essential, and how accounting software can make the process easier.

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What is accounts payable reporting?

Accounts payable reporting is the process of tracking and reporting your business expenses. It’s an ongoing reporting process that ensures your business maintains accurate financial records.

Accounts payable reporting is closely tied to accounts payable (AP), which refers to the money your business owes vendors and suppliers. These purchases may include overhead costs, inventory, and other business operational expenses. When you make a purchase, the vendor or supplier invoices you. You then make the payment at a later date.

“Accounts payable is more than just paying bills,” said Swapnil Shinde, CEO of bookkeeping software company Zeni. “It’s a systematic process that starts when an invoice is received or a purchase is made until the financial obligation is closed by settling the payment.”

Types of accounts payable reports

Here’s a look at standard accounts payable reports, what they represent, and how they can help your business stay on top of its finances.

Invoice aging report

An invoice aging report includes a list of all unpaid accounts payable invoices. The information can help determine how much the business owes and which invoices must be paid first.

An invoice aging report includes details such as:

- Vendor names

- The amount you owe each vendor

- When the invoice is due

- How long you’ve held the debt

An invoice aging report will help you spot missed payments and see how far past due an invoice is. To avoid getting behind on vendor payments, you should run an invoice aging report daily or weekly.

AP trial balance

The AP trial balance lists the ending balance in each general ledger account and includes any unpaid or partially paid invoices. The report ensures a business’s debts match its credits and that all journal entries are accurate.

Generating an AP trial balance is similar to balancing a checkbook. It reviews all payments to ensure they match the total amount due. If you accidentally overpay a vendor or miss a payment altogether, your AP trial balance will help you catch the issue. If your credits and debits don’t match, it could be because your business received inventory but hasn’t yet received the invoice. Once you’ve received the invoice, your accounts will reflect that.

Invoice aging reports can help you

manage cash flow, plan for future expenses, determine which vendors to pay first, and find ways to negotiate payment terms.

Voucher activity report

A payment voucher is a document businesses use to track supporting information needed to approve an invoice payment. It’s an internal auditing control that ensures each invoice is paid and the company receives the goods and services it purchased.

A voucher activity report includes the following information:

- A vendor’s name

- The company’s purchase order

- The total amount due

- The due date

- Discount terms offered

A voucher activity report tracks payment vouchers made over a specific period. It can help you see how much the business spent on a particular project or how much you’re spending in different departments.

It’s a good idea to generate an AP trial balance monthly or quarterly. Running the report too soon could lead to inaccurate

financial accounting information.

Open reconciliation report

The open reconciliation report shows all accounting activity concerning payment vouchers over a specific period. The report helps you determine whether your business makes accurate and timely payments to its vendors.

You can use the open reconciliation report to check for unpaid liabilities. The report will also show whether you’re sending payments to the correct vendor.

Inaccurate reporting and missed payments can cause differences in the ledger. Business bank account reconciliation can help you identify discrepancies and spot any issues with fraud.

Payment history report

A payment history report details payments you’ve made over a specific period. The report can help you see how much you’ve paid a particular vendor. It can also help with budget planning, because you can see how much you’ve spent in a certain category.

Recurring invoice report

Every company has monthly recurring bills, such as rent, insurance payments, or software subscriptions. A recurring invoice report helps ensure these bills are paid on time and makes forecasting spending easier. The report can also help the AP department flag any unusually high or low bills.

Discount report

Many vendors offer an early payment discount to companies that pay invoices in full before the due date. A discount report can help your business take advantage of early payment discounts. It will show you the early payment discounts you’re currently receiving from vendors and identify opportunities to save you may have previously overlooked.

Credit memo report

A credit memo is an adjustment that either reduces the amount of a current vendor bill or lowers future bills. Credit memos can be issued for various reasons, including product returns or incorrect pricing. A credit memo report shows how many credits are currently available so your company can apply them to future invoices.

Top vendor report

A top vendor report ranks your company’s top suppliers based on transaction volume and value. The report can help you determine which vendors are most crucial to your business and which invoices should be paid first. It can also help you negotiate more favorable terms with your suppliers.

AP turnover report

An AP turnover report tracks the efficiency of your company’s AP process and shows how quickly your business pays its vendors and creditors. A high turnover ratio means your company is paying its bills quickly, while a low ratio could indicate it’s having difficulty paying its bills.

Why is accounts payable reporting important?

Businesses of all sizes can benefit from an accounts payable process that includes accurate reporting, but an accurate accounts payable reporting process is particularly crucial for small business accounting. You must know whether you’re paying invoices on time and paying the correct amounts.

Here are a few reasons accounts payable reporting matters:

- Accounts payable reporting ensures bills have been paid. Accounts payable reporting helps a business track credit spending and ensures bills are paid on time. If your business consistently pays its vendors late, your credit rating could suffer. A poor business credit score can negatively impact future lending decisions.

- Accounts payable reporting prepares you for tax season. For small business owners, taxes matter all year ― not just during tax season. Accounts payable reporting ensures all your financial information is up to date and streamlines tax preparation. An accurate accounts payable reporting process makes collaborating with your accountant and meeting tax deadlines easier.

- Accounts payable reporting helps you maintain a good relationship with suppliers. Staying on top of your accounts payable reporting helps your business maintain positive, trusting relationships with suppliers. “A solid, well-kept relationship with suppliers helps when it comes to asking for better payment terms, which has a direct effect on a startup’s financial health and cash flow,” Shinde said.

- Accounts payable reporting ensures accurate financial records. Accounts payable reporting ensures your company’s financial data is correct. Accurate information can help you gauge your working capital, determine which invoices must be paid, and document issues as they arise.

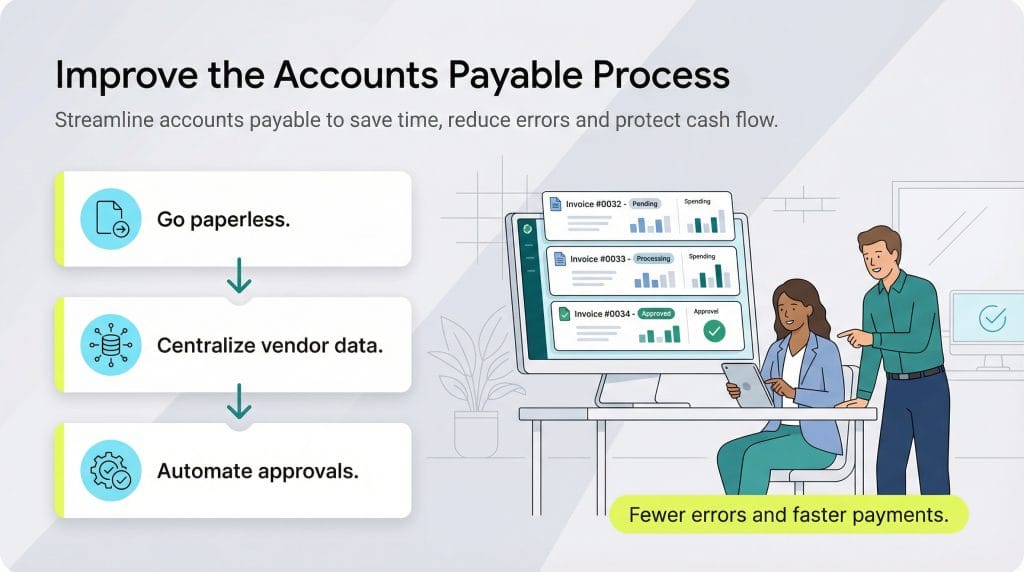

How to improve the accounts payable process

Improving the AP process can help your company free up working capital and reduce business expenses overall. Below are some steps you can take to improve the AP process.

- Go paperless: If you haven’t already, your company should consider switching to electronic statements and invoices. “Traditional paper invoices have multiple risks — they can be lost, damaged, and sometimes duplicated in error,” Shinde said. “They also contribute to clutter and require physical storage solutions.” Going paperless will make it easier to track your outstanding bills and reduce the risk of human error.

- Store vendor data in one location: Create a centralized database to store vendor information and contract details. It’s best to store the information electronically so you can easily update it if anything changes. “A fully electronic system stores vital invoice data securely in the cloud or on a server,” Shinde said. “This practically eliminates the risk of physical loss. It also makes the risk of duplicate paper invoices a thing of the past.”

- Evaluate vendor relationships: It’s a good idea to regularly review your existing vendor relationships and look for opportunities to negotiate better payment terms. This evaluation can also help you discover ways to improve those relationships.

- Create better workflows: Look for ways to improve your existing workflows and streamline the efficiency of your AP process. Even minor improvements can help you reduce bottlenecks and minimize the time your team spends on accounts payable.

Automating your accounts payable process can improve efficiency and oversight while helping you avoid common

accounting mistakes.

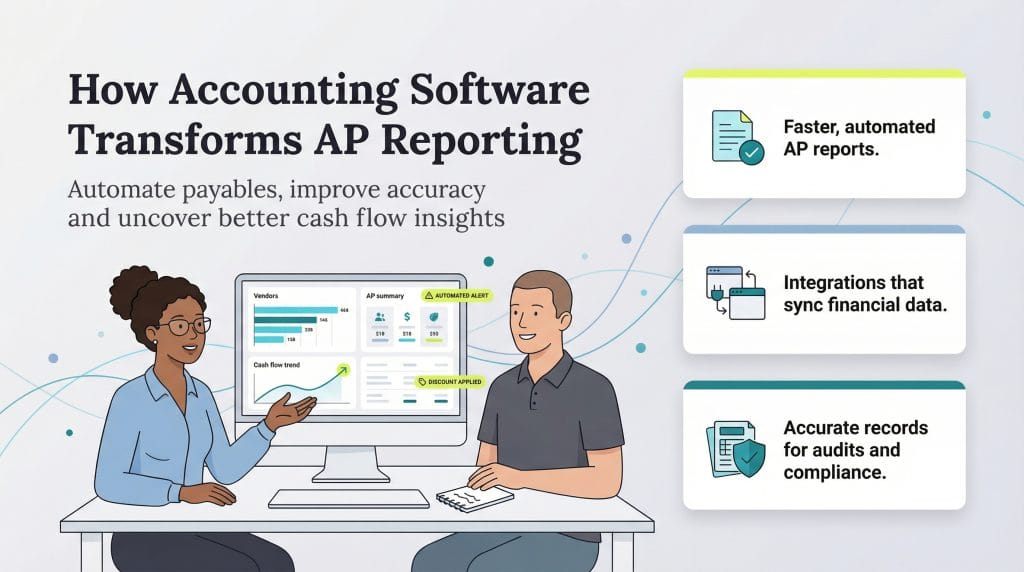

How accounting software can help with accounts payable reporting

Accounting software is an excellent way to stay on top of your AP reporting. Instead of manually entering your financial data, the best accounting software can do the heavy lifting for you while automatically generating reports and displaying payment trends over time.

“Accounting software using AI streamlines workloads and improves efficiencies for highly structured and repetitive tasks, like reporting, with a high degree of speed and accuracy,” said Paul Wnek, founder and CEO of accounts payable app ExpandAP.

Here are a few ways accounting software can benefit your business:

- View vendor information. Use accounting software to view information about a specific vendor. You can see how much you currently owe and how much your business has paid that vendor over the past year. You can also see if your company has any opportunities to save money by taking advantage of early payment discounts.

- Retain accurate financial records. Entering your financial information manually is tedious and error-prone. Accounting software automatically syncs to your bank account and reconciles your financial transactions for you.

- Protect your business from an audit. If your company is ever audited, accounting software will save you significant time because you’ll already have the financial data on hand. “AP software can assist in this regard by organizing and retrieving necessary documents, ensuring compliance with financial regulations, and providing detailed reports on financial transactions,” Wnek said. “This not only streamlines the audit process, but also enhances transparency and accountability within the finance department.”

- Generate reports automatically. You can use your accounting software to generate financial reports for your business automatically. The reports help with financial tracking, so you can track business expenses and see how much the company currently owes.

- Integrate with other business software. Accounting software can integrate with your other business software to streamline operations. You could integrate your accounting solution with one of the best CRM software platforms, for example, to generate and send invoices. “Using payment gateways like PayPal and Stripe, businesses can process transactions and accept credit card payments securely and directly within the platform,” Wnek said.

Accounting software can streamline the AP process

As a business owner, you must keep up with your accounts payable reporting. Tracking the most pertinent reports will ensure you’re aware of outstanding invoices, maintain excellent vendor relationships, and keep accurate financial records.

If you need help with your AP reporting, the right accounting software can make the process easier. Accounting software reduces the risk of human error and automatically generates the reports for you. That way, you know your financial records are always accurate and up to date.