Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

A profit and loss statement summarizes a business's revenue and expenses. Learn how to use one to gain deeper insight into your business.

At some point, you’ve probably heard the phrase, “It takes money to make money.” But if you’re not careful, it’s easy for expenses to spiral out of control — and you could end up making little to no profit. That’s why every business should track revenue and expenses with a profit and loss (P&L) statement. A P&L statement helps you measure your company’s financial health and see how your business is really performing.

Here’s a look at what a P&L statement is, what it includes, and how to use one to gain valuable insights into your business.

A P&L statement is a financial report that summarizes a company’s revenue, expenses and profit or loss over a specific reporting period, such as a month, quarter or fiscal year. When you read a P&L statement, you’ll see whether the company is generating sales, managing expenses and earning a profit.

The two main categories outlined in a P&L statement are income and expenses. Income includes things like product sales, interest earned, commissions and rental income. Expenses include the cost of goods sold (COGS), marketing and advertising fees and taxes.

“A P&L statement is important for businesses because it gives them a picture of how their business is doing during a given period of time,” explained Jackie Rockwell, co-founder of Brass Jacks, an online bookkeeping academy. “Business owners are often most interested in the bottom line — what is left over after the expenses have been subtracted from the income.”

P&L statements typically follow one of two formats: single-step or multistep. The type you’ll use depends on your business size, complexity and reporting needs.

There are two common methods of preparing P&L statements: cash accounting and accrual accounting.

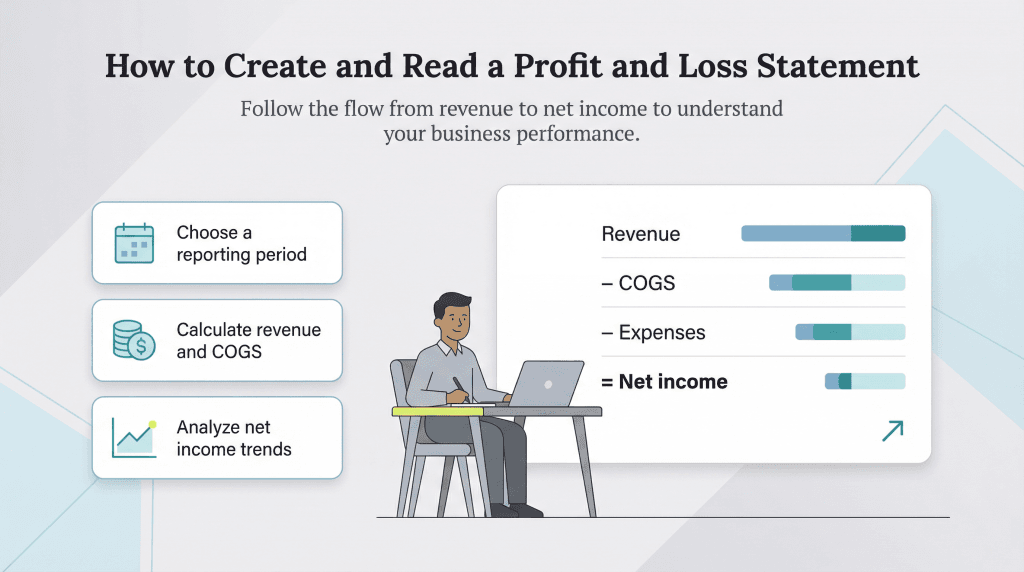

A P&L statement is a straightforward and insightful tool that shows how your business is performing financially over a set period. Whether you’re building one from scratch or reviewing a report generated by your accounting software, here’s how to create and interpret a P&L statement.

Start by selecting the time frame you want to review — usually monthly, quarterly or annually. This period will define which income and expenses you include in the report.

List all sources of income during the reporting period. This includes revenue from your core business activities (like selling products or services) and nonoperating income (like interest earned or gains from the sale of business assets).

This is the top line of your P&L.

Next, determine the direct costs involved in producing your goods or services. This might include materials, production labor or product packaging. If you run a service business, COGS may include things like subcontractor fees or billable labor tied directly to client work, while general employee salaries are typically treated as operating expenses.

For inventory-based businesses, a basic COGS formula is:

Beginning Inventory + Purchases – Ending Inventory = COGS

Although COGS is an expense, it’s listed separately for tax purposes — the IRS allows you to deduct COGS from your income before calculating taxable profit. This distinction matters when you’re preparing your annual tax return or applying for a business loan.

Next, you’ll find your gross profit with this formula:

Revenue – COGS = Gross Profit

This number shows how much you earned from sales after covering direct production costs. It’s a key indicator of your business’s core profitability.

Now, list your day-to-day operating expenses. These include overhead costs like rent, marketing, utilities, payroll, office supplies, insurance and software.

These are the costs required to keep your business running day to day. They aren’t directly tied to producing the goods or services you sell, but they’re essential to operations.

Next, you’ll subtract your operating expenses — along with any additional costs, such as interest payments or one-time expenses — from gross profit to find your net income.

Gross Profit – Expenses = Net Income

This is your “bottom line” — what remains after covering all your business costs. Depending on your accounting method and reporting format, your P&L may also reflect additional deductions like interest, taxes, depreciation and amortization. A positive net income means your business turned a profit; a negative figure means you operated at a loss during that period.

Reading a P&L isn’t just about the numbers; it’s about understanding what they say.

Ask yourself the following questions when reviewing your P&L statement:

Your P&L can help you spot patterns, adjust your budget and make smarter financial decisions moving forward.

Now that we’ve covered how to create a P&L, it helps to see everything that might appear on one in a single view. Depending on how detailed your report is, a profit and loss statement may include:

A P&L focuses only on income and expenses for a specific period. It doesn’t include your business’s assets, liabilities or equity — those appear on your balance sheet.

Below is a copy of Costco Wholesale Corporation’s 2025-2023 P&L statement, which the company refers to as its consolidated statement of income.

Even if you’re not a publicly traded company with shareholders to report to, creating and reviewing a profit and loss statement is still essential. Rockwell emphasized that every company should review its P&L regularly to support smarter business decision-making.

“While public companies are required to report their financials, private businesses rely on P&Ls for internal decision-making,” Rockwell explained. “Sometimes it is tempting to just watch the bank balance, but that doesn’t tell the full story. A P&L helps business owners understand where the company is spending its money and if a pivot needs to occur in order to stay profitable.”

Here are several crucial reasons all businesses should track their P&L:

Putting together a P&L statement doesn’t have to be complicated, and plenty of business owners handle it themselves. That said, the right accounting software makes the process significantly faster, more accurate and far less prone to human error. The right platform can help you avoid common accounting challenges and costly accounting mistakes.

Good accounting software automatically tracks your revenue and expenses in real time and organizes them consistently, so when it’s time to review your financials, you can generate a polished, accurate P&L statement in just a few clicks — no manual number-crunching required.

Here are a few great options to consider:

A P&L statement provides an overview of how much your business is earning and whether it’s operating profitably. Businesses of all sizes can benefit from creating and reviewing a P&L statement regularly.

If you’re new to P&L statements, starting with a template is a practical first step, or consider investing in feature-rich accounting software. Platforms like QuickBooks Online and Xero make it easy to track expenses and generate a P&L statement in minutes. That way, you can stay on top of your finances, make more informed decisions and be better prepared when tax season rolls around.