Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

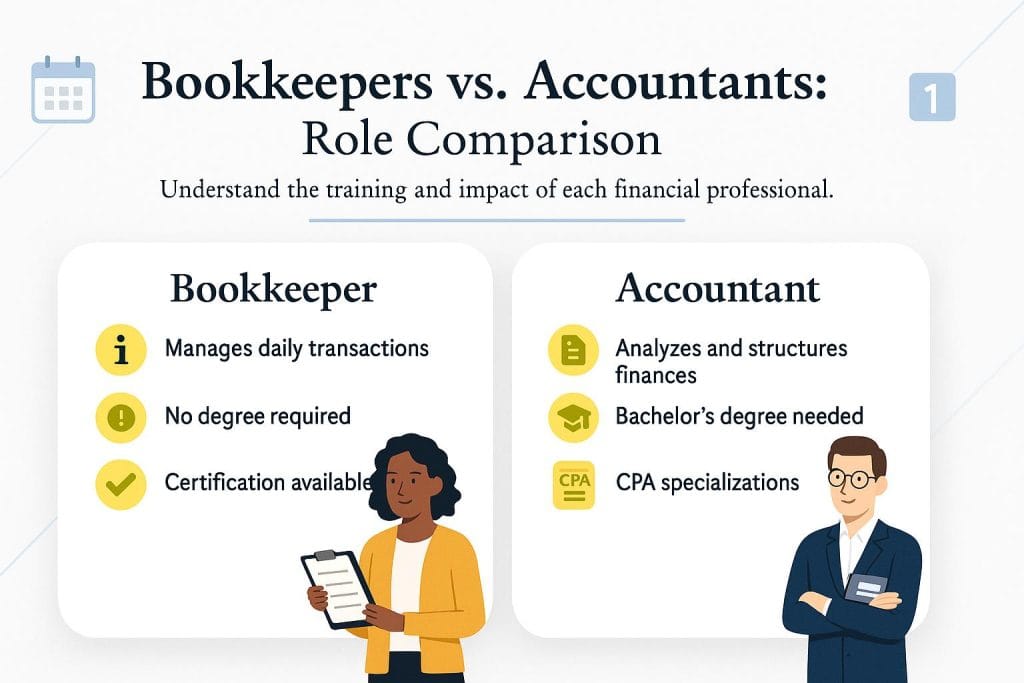

Understand these two roles to match the right financial task with the right professional.

The titles “accountant” and “bookkeeper” are often used interchangeably, but there are important differences between the two roles. For example, accountants typically charge a much higher hourly rate than bookkeepers. As a result, assigning routine bookkeeping tasks to an accountant could leave you overpaying for financial services.

We’ll outline the distinctions between bookkeepers and accountants to help you decide which financial professional best fits your needs — and why many businesses benefit from working with both.

Searching for accounting solutions and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Bookkeeper | Accountant | |

|---|---|---|

Primary duty | Record and organize daily financial transactions | Analyze, interpret and summarize financial data to provide insights |

Objective | Keep financial records accurate and current | Turn financial data into insights that guide business decisions and strategy |

Education required | No formal degree required; training or certifications preferred | Bachelor’s degree in accounting (or related field) required; advanced degrees common for senior roles |

Certifications | Optional credentials available (e.g., CPB, CB) to demonstrate expertise | CPA license required for public accounting; must pass the Uniform CPA Exam |

Typical tasks | Invoicing, payroll, expense tracking, posting debits and credits | Financial reporting, budgeting, tax preparation, audits and compliance |

Software proficiency | Proficient in bookkeeping software (e.g., QuickBooks, Xero) | Use advanced accounting and analytics platforms; may also use bookkeeping tools (e.g., Zoho Books, FreshBooks) |

Regulatory oversight | Handles records but limited compliance responsibility | Ensures compliance with tax and financial regulations |

When to hire | When you need accurate day-to-day recordkeeping and transaction management | When you need financial planning, tax strategy, audits or compliance support |

Bookkeepers and accountants may have overlapping duties, but these roles require different training and skill sets. Here’s an overview of each financial professional.

A bookkeeper is an administrative professional who manages a business’s day-to-day financial records. The role involves following established procedures for recording transactions, reconciling accounts and organizing financial data. While bookkeeping requires specific skills, software knowledge and training, it doesn’t require a formal degree.

However, bookkeepers often complete bookkeeping courses or certification programs to stay competitive. For example, the National Association of Certified Public Bookkeepers (NACPB) offers a certification program for professionals who want to demonstrate or expand their expertise.

David Leichter, a CPA and founder and CEO of Leichter Accounting Services, emphasized the importance of every business having a bookkeeper.

“I tell this to clients all the time, and they insist they can get away with simply recording their income and expenses on a piece of paper or Excel spreadsheet at the end of the year,” Leichter said. “But that’s foolish thinking. A good bookkeeper will record your transactions monthly, pull reports that show your profits and give you direction on how to minimize expenses going forward.”

An accountant is a specialized financial professional who provides higher-level financial analysis, structuring and reporting for a business. Unlike bookkeepers, accountants are typically required to hold a four-year degree in accounting, finance or business administration, along with additional training.

“The accountant’s role usually goes beyond simply preparing tax returns at the end of the year,” Leichter said. “The trusted accountant can be relied upon for proactive tax planning, advice on key business decisions and general guidance as the company grows. Having an accountant who is responsive and knowledgeable can go a long way if you view them as a partner, not simply a necessary evil.”

Gretchen Roberts, CEO of Red Bike Advisors, explained that accountants build on the work of bookkeepers by reviewing records, ensuring transactions are categorized correctly and verifying that the balance sheet balances. “Accountants are responsible for reporting on the business finances and providing an overview of the financial health of the company, as well as ensuring the books are tax-ready,” Roberts added.

You may have also heard of certified public accountants (CPAs). A CPA is an accounting professional who has passed the Uniform CPA Examination, which ensures CPAs meet rigorous standards for knowledge and ethics. The exam consists of three four-hour Core sections and one four-hour Discipline section, and candidates must score at least 75 to pass, according to the American Institute of CPAs.

While some firms employ both certified and noncertified accountants, at least one CPA must ultimately be responsible for managing a company’s financial reporting and compliance.

To help you match the right task with the right professional for your business, we’ll break down the tasks most commonly assigned to bookkeepers and accountants.

With proper standards and procedures in place, a trained bookkeeper can take on the following responsibilities:

Depending on your company’s size and how often these tasks come up, you might handle them in-house, outsource to a third-party bookkeeping service or hire a bookkeeper to work full-time. Some accounting firms also offer bookkeeping services as part of their practice.

CPAs are tasked with higher-level, more specialized responsibilities, which is why they earn more. In some cases, a noncertified accountant can handle these tasks with the careful oversight of a CPA:

Because these critical tasks tend to be relatively infrequent in small business accounting, many companies contract with an outside CPA or accounting firm to meet their accounting needs.

Many small businesses make the mistake of leaving bookkeeping tasks undone or poorly completed, forcing the CPA to finish them before tackling higher-level duties. The problem is so common that many accounting firms employ in-house bookkeepers to handle this work.

Leichter emphasized that bookkeepers are critical for day-to-day tasks like bill paying, collections, reconciliations and reporting — but they can’t replace accountants, especially for tax reporting. “Sometimes, a good bookkeeper can get involved in decision-making, even dabbling in advisory work,” Leichter explained. “But the accountant will always be handy when it comes to income tax planning and filing.”

Because accountants typically charge more, you don’t want them handling basic bookkeeping tasks that a bookkeeper could manage at a lower cost. And even if you prefer to handle your own books, Leichter stressed that hiring an accountant for taxes is worth the expense: “It’s more cost-effective to cough up the extra few bucks and have an accountant prepare those taxes professionally,” he said. “You’ll be glad in the long run that you used them!”

Ultimately, having both roles ensures accurate, up-to-date records and expert guidance on complex tax and financial matters. “They really are separate roles,” Roberts noted. “Compared to more general roles, you might say that an accountant is a manager, responsible for oversight of production, quality and communications. A bookkeeper is like an individual contributor, responsible for doing the actual work and making corrections as requested by the accountant.”

To maximize your financial team’s effectiveness, work with both a bookkeeper and a CPA. Ensure they communicate regularly and follow standardized methods. Clear role separation avoids costly inefficiencies and lets your accountant focus on higher-value tasks.

Dachondra Cason contributed to this article.