Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Debt collection occurs in phases and, although it can seem overwhelming, there are options for relief.

Debt is a common yet troublesome concern for many business owners. Ignoring debt — even just for a few months — can lead to financial burdens that are hard to come back from, including bankruptcy, eviction, wage garnishment, foreclosure, repossession, ruined credit scores and broken partnerships. Fortunately, if you address debt head-on, you can prevent these issues from taking over and causing irreversible damage to your company. Here are expert tips on how to handle your business’s debt during different stages of the debt collection process.

Searching for a collection agency and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Debt collection is the process of an entity obtaining payment on a past-due account. Types of debt among business owners include common business costs like utility bills, Small Business Administration loans and civil judgments. The multistage debt collection process varies depending on the creditor, but it usually includes phone and mail notices, stoppage of services (if applicable), notifications to credit reporting bureaus, assignment to third-party collection agencies and potential court proceedings.

While business owners can have a healthy level of business debt, ignored debt can have catastrophic results and should be mitigated as soon as possible.

“Many debtors ignore requests from [their] debt collector … at their peril,” said David Reischer, a bankruptcy attorney.

>> FREE TOOL: Debt Payoff Calculator

The debt collection process can begin as soon as a scheduled payment is missed, but it typically takes effect around the time the payment is 30 days past due. Here is a breakdown of the four main stages of the process.

In this stage, you’re behind on your payment. Your creditor will likely call, email or send a letter politely reminding you that your payment is past due and should be submitted as soon as possible. They may reach out to credit reporting bureaus to report your account as delinquent and eventually enlist the services of a collections agency.

“As soon as a collection company takes on a debt, the initial notice is sent, with an explanation of debtor rights to dispute the debt,” said Ali Zane, CEO of Imax Credit Repair Firm. “Only after 30 days [can] the account be reported to the credit bureaus.”

What you should do: If you know you’re going to miss a payment, reach out to the vendor or creditor proactively. They may be willing to formulate a payment plan to get you back on track. If you do miss your payment without notifying them, contact the company as soon as possible and collaborate on a repayment plan. Do not ignore calls and letters seeking payment — during this stage, you can still easily rectify the situation.

At this point, your debt is still with your original service provider, but their contact with you will become more aggressive and persistent. The creditor will report your delinquent account to credit reporting bureaus if they have not done so already, and you may accrue penalty fees.

“At the 60-day period, an intent to sue letter can be sent off,” Zane told us. “The debtor may be sued only if the debt is within the statute of limitations. When filing a lawsuit, the collector must take into [consideration] the cost of legal action, the ability of the consumer to pay and the size of the debt.”

What you should do: In this phase, it’s still not too late to reach out to the company to work out a payment or hardship plan. Swift, direct contact is your best course of action.

Now, since the situation wasn’t resolved, the unpaid debt has been turned over to a top collection agency, and your credit report has likely been updated to reflect that you’re in arrears. The agency will purchase the debt amount for a fraction of the balance due, usually 30 to 35 percent, said Todd Christensen, education manager at Money Fit. He advised being proactive and cautious — after the collection agency purchases the debt for a portion of the balance due, it may contact you to collect the full balance.

The collection agency “will never tell the consumer that they only paid a fraction of the balance due,” Christensen said. “They just notify the consumer of the balance owed and try to collect as much as possible.”

What you should do: To avoid a ruined credit score, immediately contact your original creditor, such as the lender, utility company or merchandise supplier, and try to set up a repayment plan directly with them. This way, Christensen said, the account may be returned from collections, and your credit standing may be saved. He recommended following the below steps once a collection agency contacts you:

If the collection agency has been unable to contact you and you didn’t resolve the debt with the original creditor, the agency will file a lawsuit. You will receive a court summons, and you must attend the hearing on the assigned court date. If you don’t, it will mean an automatic win for the collection agency. In court, the judge can deliver a money judgment.

“A creditor that is serious about collecting a debt can then take that money judgment and record a lien against [your] home, levy funds on a bank account or force the sale of an expensive asset,” Reischer said. “A debt collector can execute on the lien and have a marshal or sheriff seize the property and arrange for a public sale from which the creditor is paid out of the proceeds.”

What you should do: First, show up to your court date so you can dispute the debt. Then, ask the judge if they are willing to oversee the creation of a repayment plan instead of imposing a lien, wage garnishment or sale of an asset.

>> Read Next: Business Debt: How Much Is Too Much to Carry?

The experts business.com spoke with offered additional tips for handling debt and reducing the harm to your business.

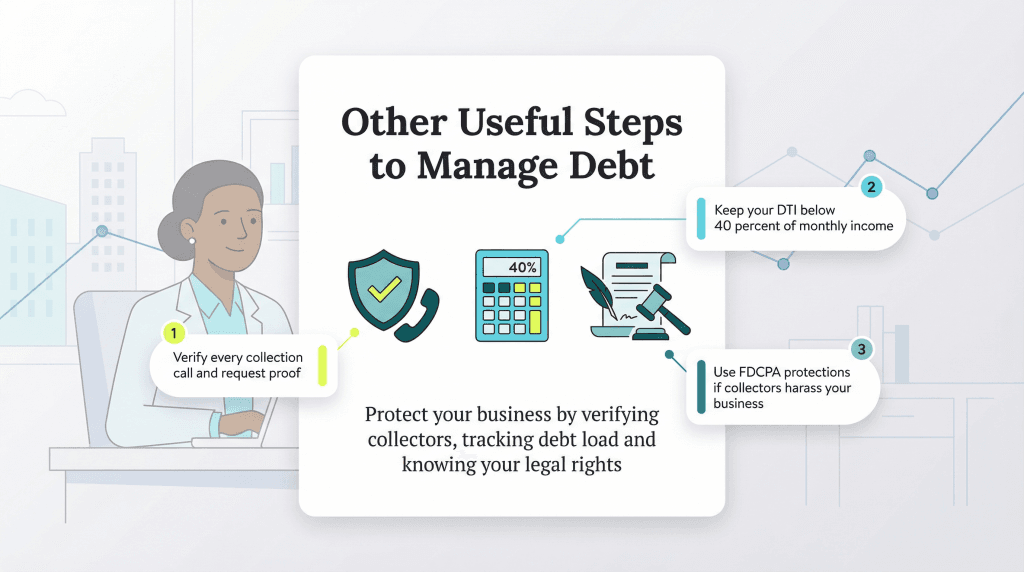

Know whom you’re speaking to when someone calls you or your business demanding payment for an alleged debt. While the message may be alarming and make you think you need to resolve the issue on the phone right then and there, you should first take the time to make sure the call is legitimate.

“Never cave to the pressures of a collection call,” Christensen said. “If you do not recognize the debt, always ask for verification and never give your bank information out.”

To stay out of debt, Reischer recommended calculating your monthly DTI ratio and never taking on debt with monthly payments that exceed 40 percent of your monthly income.

“A prudent lender will not lend to a borrower when the DTI ratio becomes very high,” Reischer said. “But it is the borrower’s ultimate responsibility to calculate their own DTI ratio to determine whether they are able to repay a loan.”

>> Related Article: Hidden Gotchas in Your Business Loan Repayment Terms

That said, Zane warned against solely focusing on your DTI. “The actual income is also important, as someone can have a low DTI and a low income as well, which would make it difficult for the debtor to pay a high collection amount,” he said.

The FDCPA protects consumers from excessive contact by collection agencies by outlining when and how often they can contact you.

“The FDCPA regulates all collection activity across the U.S.,” Zane said. “It is a strict liability statute, meaning it holds the debtor liable for any negative consequences of their actions regardless of intent or fault. It requires debtors not to stress or harass debtors. A collector must stop contacting the debtor if the debtor asked not to be contacted. And there are many more requirements of the FDCPA, each carrying a minimum fine of $1,000 per violation … or actual damages.”

Christensen recalled a client who was receiving harassing phone calls from a collection agency they didn’t know. The agency threatened the person with legal action and personal contact but its claims were unsupported and violated the FDCPA. That enabled the client, together with an attorney, to send a certified letter to the agency demanding it cease all contact.

Amanda Hoffman and Sean Peek contributed to this article. Some source interviews were conducted for a previous version of this article.