Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Although these terms have much in common, business owners must understand the distinction.

While often used interchangeably in casual conversation, revenue and income represent two distinct financial realities for a company.Although they have much in common, there are crucial differences between these two financial terms. Business owners must understand the distinction between net income and revenue (and accurately measure both) to better understand their expenses, including inventory expenses, overhead costs and other outlays.

Understanding revenue and income is also essential because businesses are valued differently using one number vs. the other — and only net income is taxable. In a high-inflation environment where costs rise distinct from sales prices, knowing the difference is vital for survival. We’ll explain the differences between revenue and income to help business owners use each term correctly to avoid confusion and communicate clearly with accountants, financial advisors, investors and lenders.

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

Revenue is the total amount of money a business earns over a specified period. The number is often noted as “total sales” or another figure that indicates the entire amount the company brought in. Businesses can generate this money from many different avenues, but the figure does not include business loans taken out during the covered period.

“A company with strong revenue is often seen as having high market demand and effective sales strategies,” explained Rose Jimenez, chief financial officer of Culture.org. “However, high revenue alone doesn’t mean a business is profitable.”

Net income appears at the bottom of an income statement and is often used as the starting point for a cash flow statement. It represents the amount left over after a business accounts for revenue and expenses over the same period, such as all the money flowing into and out of the company. “[Net income] reflects how efficiently a company converts revenue into actual profit,” Jimenez explained. “A business with high revenue but low income may struggle with excessive costs, inefficient pricing or poor financial management.”

Income could be negative if a company’s expenses exceeded its revenue during the period in question. In that case, the company operated at a loss. This distinction is critical; according to the Federal Reserve’s 2024 Report on Employer Firms, 54% of small businesses reported experiencing financial hardship in the prior 12 months, often driven by the widening gap between rising operating costs and revenue.

“I’ve seen businesses celebrate skyrocketing sales while quietly struggling with shrinking net income due to rising expenses,” Hemming shared. “This is why understanding both revenue and income is crucial — revenue shows how much money is coming in, while income reveals what’s left after all expenses.”

Measuring a business’s net income starts with looking at its revenue — how much money it brought in over a set period. Then, the company makes adjustments for all expenses incurred over the same period. Those fixed and variable expenses could include the following:

While these are ordinary small business expenses, not all of them apply to all companies. The expenses applicable to your business depend on its size, type, industry and specific accounting practices.

Different businesses use various measurements for revenue and net income. Each figure includes several factors and is relevant to a particular company based on its industry and operations.

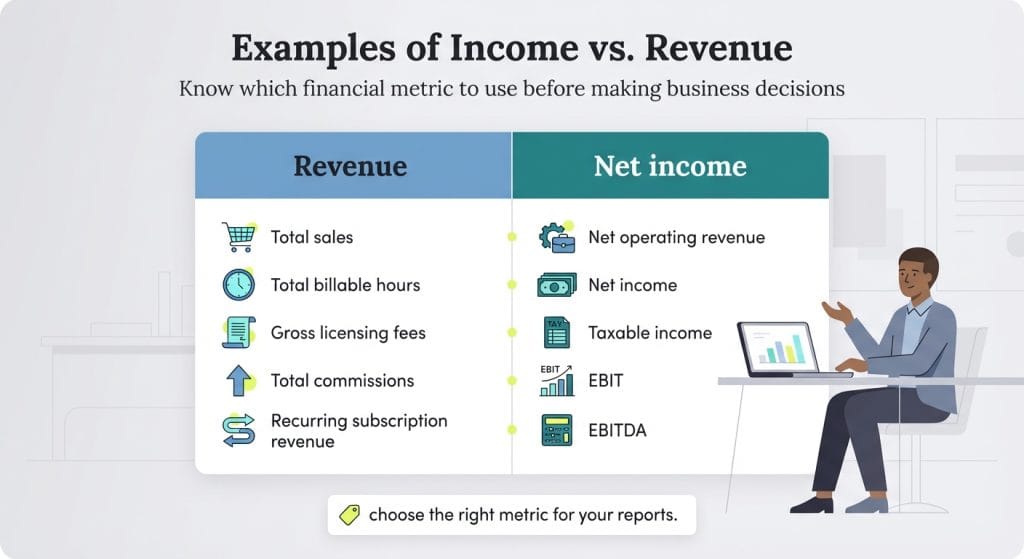

Gross revenue is much more straightforward than net income. It’s the total amount of money a business takes in over a specific period. Here are some examples of gross revenue:

Net income — the amount of money a company makes or loses over a period after offsetting expenses against revenue — is provided separately on accounting statements. It may appear on financial statements as any of the following:

Like revenue, a company’s net income is easy to calculate using small business accounting software, but it’s more involved. A manager must generate a report that includes revenue and expenses, particularly those relevant to the company’s specific operations. (Generating reports is a typical accounting software feature.)

Once a manager produces a report reflecting some measure of net income (usually a profit and loss statement), they still need to know which metric to use and how to use it. That’s one of the challenges of business accounting: Software can provide a lot of information, but it doesn’t tell business owners how to use these insights.

While a business’s net income includes more information about the overall state of its finances, both revenue and income are essential for small business owners to know, measure and track. Investors, for example, may look at revenue to judge a company’s potential market share, but lenders will scrutinize net income to determine if the business has enough cash flow to repay a debt. These metrics are used for different purposes, but here are some typical uses for both revenue and income:

Revenue and income are regularly provided in company financial reports to shareholders. Depending on a business’s type and size, these figures also may be included in reports filed with regulators, such as the United States Securities and Exchange Commission.

Revenue and income are also prominent fixtures in tax forms filed with the IRS, as well as in company strategies for minimizing tax liability incurred from year to year. Accurate income reporting helps prevent overpayment of taxes while ensuring compliance with federal tax obligations.

As Hemming put it, “True success isn’t just about making more sales — it’s about managing costs and ensuring profitability.”

Jennifer Dublino contributed to this article.