Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What’s the Difference Between Net Income and Profit?

Understanding how these two terms differ will help you measure how well your business is doing and communicate those results more accurately.

Written by:

Sally Herigstad, Senior Writer

Editor verified:

Shari Weiss,Senior Editor

Last Updated Feb 02, 2026

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Financial success is the goal of every business owner, but tracking it isn’t always straightforward. Many business owners look at their profit and assume they know how well their company is doing, but that number doesn’t always tell the whole story. In particular, terms like “net income” and “profit” are often used interchangeably when they actually mean different things.

Understanding the difference between the two helps you communicate your business’s financial results accurately and make smarter decisions. We’ll break down what profit and net income really mean, how they compare, and why knowing the difference matters for your bottom line.

Why understanding net income vs. profit matters

It’s easy to confuse profit and net income, especially when you’re focused on sales. Sales show what’s coming in, and increasing sales is a natural goal for business owners. But sales alone don’t reveal how much of that money actually stays in the business. Profit offers part of the picture, while net income shows what truly remains once every expense is covered.

That distinction matters even more as costs rise. According to the Federal Reserve’s 2025 Report on EmployerFirms, rising costs were the most common financial challenge for small businesses in the prior year, cited by 75 percent of employer firms. When expenses increase, understanding your net income — not just your top-line profit — gives you a clearer view of your business’s financial health.

Knowing the difference between net income and profit helps you:

Explain your company’s results clearly to lenders, business investors and employees.

Make realistic decisions about how much money to reinvest or take home.

Spot operational inefficiencies or pricing issues before they become bigger problems.

Cassandra Gucwa, founder and CEO of Minerva Digital, learned this firsthand: “When I started my business, I thought it was doing well when I saw the gross income.” But once she looked at net income after all expenses, she came back down to earth.

Her experience shows how strong sales or gross profit can be misleading if you don’t look at what’s left at the end of the day.

What is net income?

Net income, also called net earnings or net profit, is the amount your business keeps after subtracting all expenses, including operating costs, loan interest, business taxes and one-time charges. It’s often called the “bottom line” because it sits at the end of the income statement.

Here’s the basic formula:

Total revenue – total expenses = Net income

Unlike sales or partial profit measures, net income reflects the full financial picture of your business. It accounts for:

One-time charges or gains (such as selling equipment)

Because it’s calculated after everything is deducted, net income is one of the best indicators of your company’s true financial standing. Tracking it consistently lets you compare results period over period and see whether your business is growing, holding steady or falling behind.

Tip

Make sure you understand fixed vs. variable expenses. A fixed expense, such as rent, doesn't change due to sales or production volume. Variable expenses, such as labor and materials, change based on your levels of sales and production.

What is profit?

Analyzing profit at different stages—gross, operating, and net—gives you a clearer picture of your business health.

Profit is the money your business makes after subtracting certain expenses. Unlike net income, which always reflects all expenses, “profit” can describe earnings at different stages. That’s why the term can be confusing — it’s a broader category, not just one number.

On an income statement, you’ll usually see three main types of profit:

Gross profit: Revenue minus the cost of goods sold (COGS). This shows how efficiently you produce or source what you sell, but it doesn’t include operating expenses.

Operating profit: Gross profit minus operating expenses like payroll liabilities, rent, utilities and other overhead costs. This measures how well your core operations are performing.

Net profit (net income): Operating profit minus taxes, interest and all other expenses. This is the bottom line — the amount your business actually keeps.

Each type of profit offers a different view of performance. For example, strong gross profit but weak net income may signal that non-production costs are cutting into results. Looking at all three together gives you a layered, realistic picture of your company’s financial health.

Bottom Line

In financial accounting, profit can mean different things depending on which expenses you subtract, but net income is always the all-inclusive final measure. Knowing the difference helps you see your company's financial health more clearly.

Analyzing profitability in your business

Understanding the difference between gross, operating and net profit is only the first step. To see how your business is really performing, you also need to measure those numbers relative to sales, and that’s where profit margins come in.

For example, the gross profit margin shows how efficiently you produce or source what you sell. The formula is simple:

Gross profit ÷ Net sales = Gross profit margin

If you sell a product for $8 that costs $6 to make, your gross profit is $2, and your gross profit margin is 25 percent. In other words, for every dollar in sales, 25 cents is left after covering production costs.

However, Chris Sorensen, CEO of PhoneBurner, cautions against looking only at gross profit. “You might see sales increasing, but if operational costs are also rising, profitability as a whole will likely remain stagnant,” Sorensen explained. Many business owners invest heavily in marketing or infrastructure based on gross revenue, only to find themselves squeezed when overhead or fulfillment costs climb.

That’s why it’s critical to also track operating profit, which shows how well you’re managing expenses like rent, salaries and marketing, and net income, which reveals the bottom line after every cost, including taxes and interest.

By monitoring each type of profit over time, you can spot where money is being lost, adjust pricing and expenses, and benchmark your performance against others in your industry.

FYI

Comparing your profit margins to industry trends and averages can reveal whether you're underperforming or ahead of the competition.

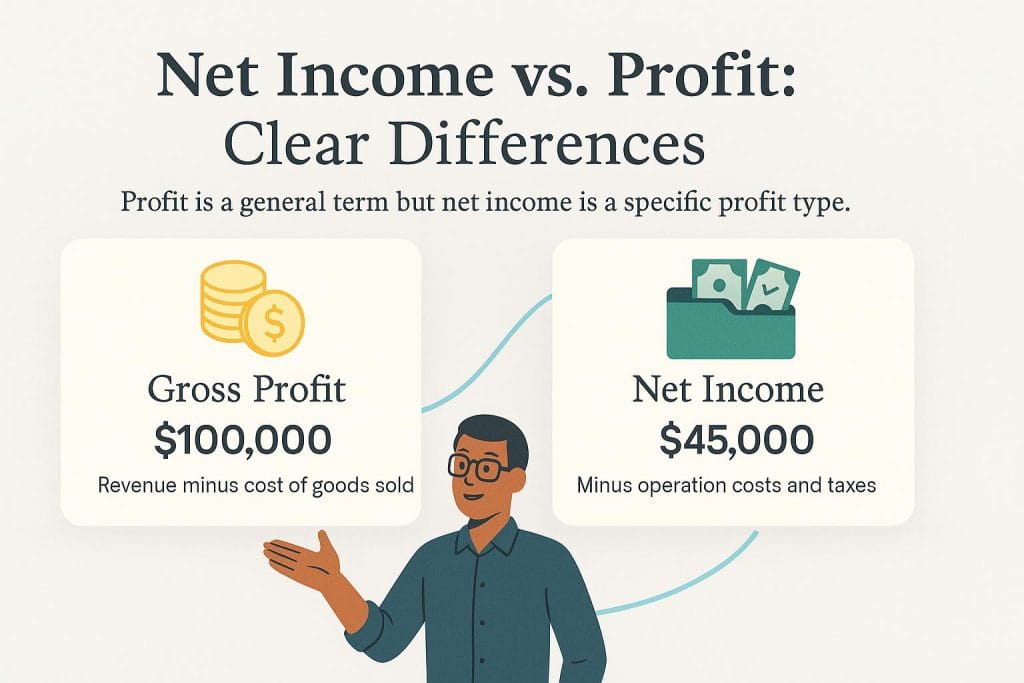

Example of net income vs. profit

Net income is your bottom line after all expenses—including taxes and interest—are paid, whereas gross profit only accounts for the cost of goods sold.

It’s one thing to define profit and net income, but seeing the numbers side by side makes the difference clearer.

Suppose Company Z reports a gross profit of $100,000 — revenue minus the cost of goods sold. After subtracting operating expenses, taxes and interest, however, the company’s net income is $45,000. That’s the true bottom line: the money the business actually keeps once every expense is covered.

Did You Know?

Net income will always be lower than gross profit because it includes operating costs, taxes, interest and other expenses beyond production.

What to do if your profits fall short

Even with strong sales, many small businesses are surprised to see profits fall short of expectations. Hidden expenses, rising overhead and underpriced products can quietly eat away at the bottom line.

Gucwa learned this firsthand after an unsuccessful email marketing campaign yielded a disappointing digital marketing ROI. “We invested about $25,000 in email marketing, and our return on investment was much lower than that of other marketing channels,” Gucwa recalled. However, by shifting strategies and trimming costs elsewhere, her company boosted its net profit.

Pricing can also be a silent culprit. Gucwa recalled a friend selling on Etsy who saw steady sales but almost no profit because prices didn’t reflect the true costs of running the business — including platform fees and the value of the owner’s time. It’s a common pitfall for new entrepreneurs eager to attract customers.

Michael Bush, co-founder of GrowthWays Partners, says business owners should focus on three areas when profits lag:

Gross margin: Look for ways to improve efficiency, negotiate better supplier terms or adjust pricing.

Expenses: Scrutinize your spending to cut business costs without stalling growth. Marketing campaigns and travel are common places to find savings.

Cash flow: Keeping a close eye on your cash position is a common accounting challenge. “Cash tells the real story,” Bush noted. “If you’re consistently running low, something needs to change.”

The good news? Profitability issues don’t mean your business is doomed. By reviewing margins, tightening expenses and monitoring cash flow, you can make course corrections before small leaks sink the ship.

Bottom Line

Falling short on profits is usually fixable. By checking margins, trimming expenses and watching cash flow, you can spot problems early and steer your business back on track.

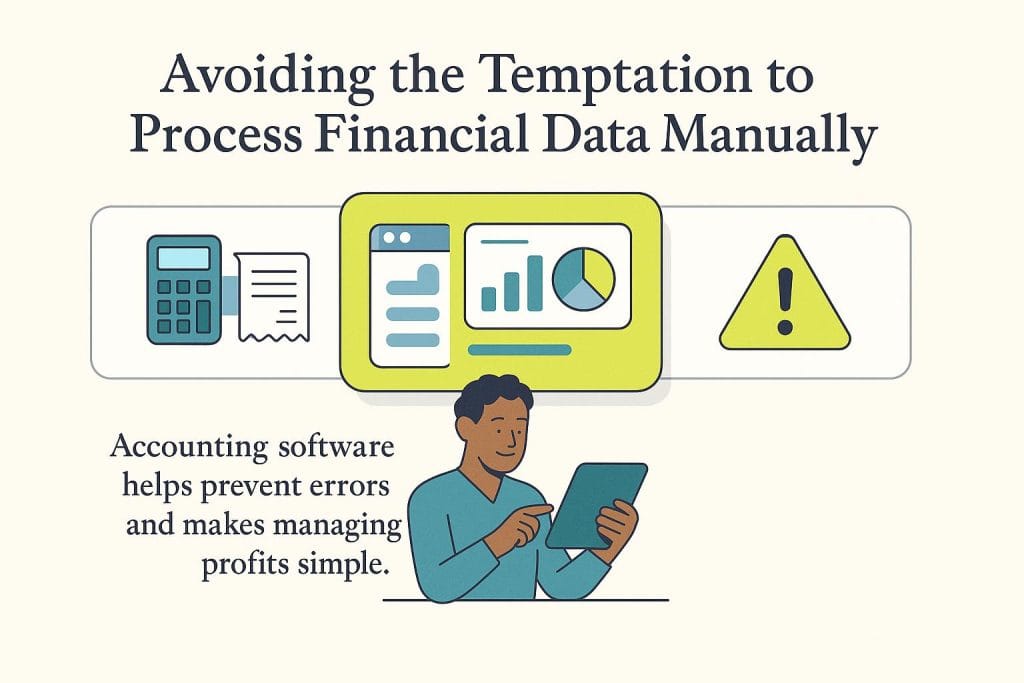

Don’t rely on spreadsheets alone

Manual tracking leads to errors. Modern accounting software automates calculations, ensuring accurate net income reporting.

Many small business owners start out tracking finances in a spreadsheet. It feels quick and affordable, but the risks add up fast. Missed entries, inconsistent records and late reconciliations can leave you guessing about your company’s true performance.

Gucwa discovered this the hard way: “I had no idea what my net income was. I only found out how profitable my business was when I compiled information for my taxes.” After switching to QuickBooks and hiring an accountant, she finally gained a real-time view of her company’s financial health.

Automation makes that difference even clearer. “Automated reports that show real-time net income, versus only projections, have really helped us make more informed decisions on various aspects of the business — hiring, pricing, reinvesting,” Sorensen explained.

The best accounting software does more than crunch numbers. Today’s platforms surface real-time insights, highlight trends on dashboards and flag potential cash flow issues early. That visibility can mean the difference between making smart, timely decisions and realizing too late that profits aren’t where they should be.

Dachondra Cason contributed to this article. Source interviews were conducted for a previous version of this article.

Did you find this content helpful?

Thank you for your feedback!

Share Article:

Written by: Sally Herigstad, Senior Writer

Sally Herigstad is a retired CPA who spent nearly a decade advising on tax and money issues for Microsoft properties, in addition to hemming a financial advice column for CreditCards.com. She is skilled at breaking down complicated tax guidance for both personal finance and business finance audiences and has even helped develop tax software.

At business.com, Herigstad covers accounting topics, particularly those related to taxation.

Herigstad is the author of the book Help! I Can't Pay My Bills: Surviving a Financial Crisis. Her expertise has been featured in U.S. News & World Report, Bankrate, Realtor.com, The Motley Fool and TaxAct, among others.