Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

How to Create Payroll Journal Entries

Stay on top of your accounting with this process, which tracks the money you spend on wages and other expenses.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Tracking your company’s spending is essential for maintaining accurate financial records. One financial accounting method businesses use is the payroll journal entry.

Payroll journal entries record your workers’ pay alongside overall business expenses. While the process may look different for every company, payroll ledgers typically include employee compensation, benefits, taxes and deductions. Let’s look at the types of payroll journal entries and how to record them.

Searching for payroll software or services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Tip

The best online payroll services can connect to your accounting software and generate payroll journal entries automatically, helping you stay organized and reduce errors.

What is payroll accounting?

Payroll accounting is the process of tracking all the money a business spends on wages and payroll taxes. It’s integral to ensuring your employees are paid in full and on time — and it keeps you out of hot water with the IRS. Proper payroll accounting also balances your general ledger (GL) so you can be more confident in the accuracy of your financial statements.

Payroll journal entries are the foundation of payroll accounting. They record each payroll-related transaction in your books, allowing you to keep track of gross pay, deductions and employer expenses in real time.

Karen Mann, owner of Rosemary Bookkeeping North Dorset and Salisbury, explained why accurate payroll journals matter for businesses beyond just compliance. “They ensure complete management information, allowing businesses to track staff costs, monitor cash flow and verify amounts due to HMRC [His Majesty’s Revenue and Customs] and pension providers,” Mann said. “This helps with financial planning and ensures compliance with legal obligations, ultimately supporting smooth business operations.”

What are payroll journal entries?

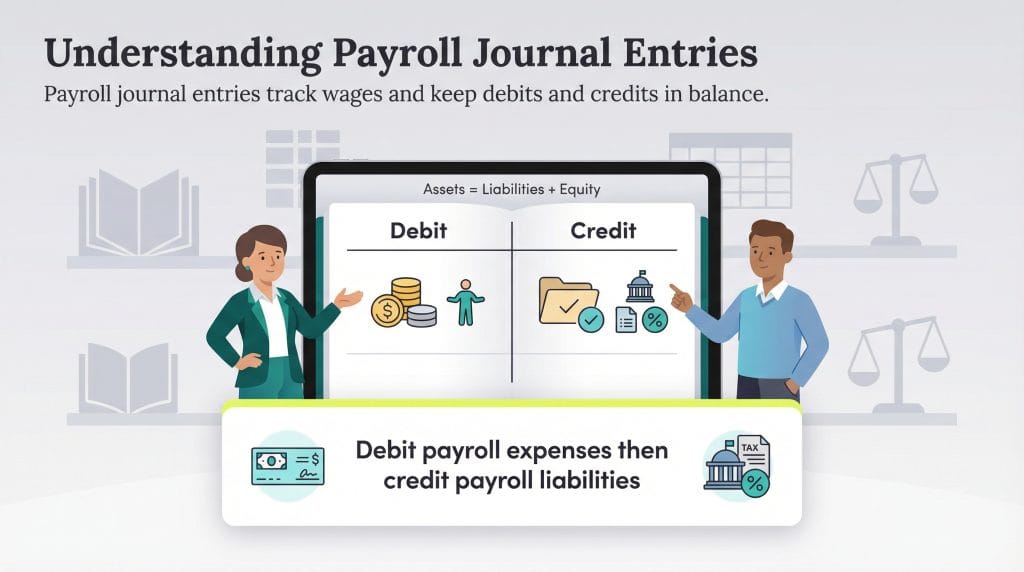

Payroll journal entries are the records you enter in your small business’s GL to track employee wages and payroll-related costs. Each payroll journal entry follows the double-entry accounting method, meaning it’s paired with another entry of an equal and opposite amount. In this method, when your company increases money in one account (a credit), it decreases money in another (a debit) — and vice versa.

For example, when you pay employees, you debit your expense accounts to reflect the cost of wages. At the same time, you credit your liability accounts — such as payroll payable — to show what your business owes. This keeps your books balanced and ensures payroll transactions are properly recorded.

Did You Know?

When recording payroll, you should debit your expense accounts and credit your payroll liabilities — accounts that reflect what you owe to employees, tax agencies and benefit providers.

Types of payroll journal entries

These are the three main types of payroll journal entries.

1. Initial recording payroll entry

Initial recordings are the most detailed type of payroll entry. They include debits for wages, direct labor expenses and payroll taxes, along with equal and opposite credits to liability accounts for each category.

In many cases, wages and direct labor are interchangeable, but they may differ depending on your industry. For example, in construction, direct labor often refers to wages paid for open jobs, while general wages may apply to overhead employees.

For your payroll taxes debit, you’ll record credits for each type of tax withheld. These may include federal and state income taxes, federal unemployment tax (FUTA), state unemployment tax (SUTA) and FICA (Social Security and Medicare).

If you also withhold other payroll deductions, such as benefit plan premiums, retirement contributions or wage garnishments, you’ll need to record those in your initial payroll entry as well. Each benefit or deduction should appear in its own row as a separate credit.

Your initial recording payroll entry should look like this table:

Date

Account

Debit

Credit

9/10/2025

Wages

$200,000

N/A

9/10/2025

Payroll taxes expense

$70,000

N/A

9/10/2025

Wages payable

N/A

$200,000

9/10/2025

Employee FICA tax payable

N/A

$15,000

9/10/2025

Federal income tax payable

N/A

$24,000

9/10/2025

State income tax payable

N/A

$8,000

9/10/2025

Wage garnishments payable

N/A

$1,000

9/10/2025

Employer FICA tax payable

N/A

$15,000

9/10/2025

FUTA tax payable

N/A

$1,000

9/10/2025

SUTA tax payable

N/A

$6,000

Payroll taxes are unique in payroll journal entries because you typically withhold them before you pay them. When you submit each tax payment, you must debit the related liability account and credit your payroll account to reflect the cash outflow.

After payment, the relevant section of your payroll journal will look like this:

Date

Account

Debit

Credit

9/10/2025

Employee FICA tax payable

$15,000

N/A

9/10/2025

Federal income tax payable

$24,000

N/A

9/10/2025

State income tax payable

$8,000

N/A

9/10/2025

Wage garnishments payable

$1,000

N/A

9/10/2025

Employer FICA tax payable

$15,000

N/A

9/10/2025

FUTA tax payable

$1,000

N/A

9/10/2025

SUTA tax payable

$6,000

N/A

9/10/2025

Payroll account

N/A

$70,000

FYI

In payroll journaling, you withhold payroll taxes before you file and pay employee payroll taxes. You'll first record the withholdings as liabilities, then make a second journal entry when you submit payment to tax agencies.

2. Accrued payroll entry

Despite how comprehensive your initial payroll entry may seem, it might not cover all outstanding wages. That’s because, in some cases, employees have earned wages that haven’t yet been paid when an accounting period closes. In these situations, you’ll need to create an accrued payroll entry to account for the remaining balance.

When creating accrued payroll journal entries, group unpaid wages in one row and the related payroll taxes in another. This type of payroll journaling is simpler than initial recording, but you must reverse the accrued entry at the beginning of the next accounting period to avoid duplicating expenses.

An accrued payroll entry may look like this:

Date

Account

Debit

Credit

9/10/2025

Wages

$200,000

N/A

9/10/2025

Accrued wages

N/A

$150,000

9/10/2025

Accrued payroll taxes

N/A

$50,000

3. Manual payroll entry

If you pay wages by check outside your company’s typical payroll cycle, you’ll need to create a manual payroll journal entry to account for them. These off-cycle payments often don’t come from your standard payroll account — they may be paid through accounts payable instead.

Even if the payment method is different, you’ll still use the same payroll line items, such as wages, payroll taxes and deductions, to record the transaction correctly in your ledger.

How to record payroll entries

While online payroll software or services can handle payroll entries for you, it’s still important to understand how to record them manually. Knowing the payroll journaling process can help you spot discrepancies — such as incorrect numbers or missed deductions — that may arise from data entry errors. It also gives you more control and confidence in your employee payment process.

Follow these steps to create payroll entries.

How to Create Payroll Journal Entries

Log wage payments in appropriate accounts

Record employee payroll deductions

Record employer-paid payroll taxes and benefits

Transfer cash to the payroll account

Pay employees and record the payment of wages

Pay employer payroll deductions

1. Log your wage payments in the appropriate accounts.

Let’s say you pay $200,000 in total wages for the pay period. You’ll record this amount as a debit to your wages expense account and a credit to your wages payable account.

The distinction between these two similarly named accounts is that wages expense is a cost of doing business while wages payable is a liability. Because expense and liability accounts appear on opposite sides of the accounting equation, it’s correct to debit one and credit the other in equal amounts.

Your payroll journal entry will look similar to this chart:

Date

Account

Debit

Credit

9/10/2025

Wages

$200,000

N/A

9/10/2025

Wages payable

N/A

$200,000

If your company distinguishes between wages and direct labor, you’ll need to split your $200,000 wage expense into separate rows in your journal entry:

Date

Account

Debit

Credit

9/10/2025

Wages

$150,000

N/A

9/10/2025

Direct labor

$50,000

N/A

9/10/2025

Wages payable

N/A

$200,000

2. Write down your employee payroll deductions.

In addition to wages, you must also record payroll deductions, such as FICA taxes, income taxes, employee benefit premiums and wage garnishments. These are amounts withheld from your employees’ paychecks and recorded as liabilities in your GL.

To create payroll journal entries for these deductions, make a row for each type of tax titled “[tax name] payable.” Record each tax amount as a credit. Then, record the sum of these credits as a payroll tax debit.

Your payroll journal entry for these deductions should appear similar to this table:

Date

Account

Debit

Credit

9/10/2025

Payroll taxes

$200,000

N/A

9/10/2025

Employee FICA tax payable

N/A

$60,000

9/10/2025

Federal income tax payable

N/A

$96,000

9/10/2025

State income tax payable

N/A

$32,000

9/10/2025

Wage garnishments payable

N/A

$4,000

9/10/2025

Employee health insurance premiums payable

N/A

$8,000

3. Record your employer payroll deductions.

Employee payroll deductions are only part of the story — as an employer, you must also pay payroll taxes and benefits on behalf of your employees. These include FUTA, SUTA and the employer’s share of FICA taxes. One way to double-check your calculations is to confirm that the employer and employee FICA amounts are equal.

Mann cautioned that misclassifying payroll entries can lead to serious issues. “Misallocating payroll costs or not entering the information means financial reports are incorrect and can’t be used to help make business decisions and will affect tax calculations,” Mann explained.

To record these amounts, create credits for each employer tax and benefit payable, along with the debit to the payroll expenses account. This includes employer-paid premiums for benefit plans (such as health insurance and workers’ compensation) and the dollar value of any paid leave employees have taken.

Your payroll journal entry will look like this:

Date

Account

Debit

Credit

9/10/2025

Payroll expenses

$124,000

N/A

9/10/2025

Employer FICA tax payable

N/A

$60,000

9/10/2025

FUTA tax payable

N/A

$4,000

9/10/2025

SUTA tax payable

N/A

$24,000

9/10/2025

Employer health insurance premiums payable

N/A

$20,000

9/10/2025

Employer workers’ comp insurance premiums payable

N/A

$12,000

9/10/2025

Employer pay for employee leave payable

N/A

$4,000

Tip

To avoid common accounting mistakes, check that your employer and employee FICA tax totals match — they should always be equal.

4. Add cash to your payroll account.

You’ll need to transfer cash into your payroll account to cover all payroll-related costs. When moving funds from your operating cash account to your payroll account, record a debit to the payroll account and a credit to the operating cash account.

To determine how much to transfer, add the wages expense from step one, the payroll tax debit from step two and the payroll expenses from step three. Then, subtract any non-cash items, like the employee leave credit from step three. The result is the amount of cash you need to fund payroll.

Once you’ve funded your payroll account, it’s time to pay your employees — and create one more payroll journal entry.

Since you previously debited your payroll account to set aside the cash, you’ll now credit it to reflect the outflow of funds. To balance the entry, debit your wages payable account, reducing the liability you’ve been tracking.

Your payroll journal entry will look like this:

Date

Account

Debit

Credit

9/10/2025

Wages payable

$520,000

N/A

9/10/2025

Payroll account

N/A

$520,000

6. Pay all your deductions and record the payments.

The final step is to pay all your recorded deductions — excluding employee leave, which has already been accounted for as a noncash item.

For each payable account, debit the amount you previously recorded as a credit. Then, credit your payroll account for the total amount paid. This clears your liabilities and reflects the cash leaving your payroll account.

Your payroll journal entry will look like this:

Date

Account

Debit

Credit

9/10/2025

Employee FICA tax payable

$60,000

N/A

9/10/2025

Federal income tax payable

$96,000

N/A

9/10/2025

State income tax payable

$32,000

N/A

9/10/2025

Wage garnishments payable

$4,000

N/A

9/10/2025

Employee health insurance premiums payable

$8,000

N/A

9/10/2025

Employer FICA tax payable

$60,000

N/A

9/10/2025

FUTA tax payable

$4,000

N/A

9/10/2025

SUTA tax payable

$24,000

N/A

9/10/2025

Employer health insurance premiums payable

$20,000

N/A

9/10/2025

Employer workers’ comp insurance premiums payable

$12,000

N/A

9/10/2025

Payroll account

N/A

$320,000

Creating payroll journal entries manually is tedious and time-consuming — and it’s easy to make mistakes. Many payroll software platforms can automate this process and generate a complete, accurate payroll ledger in a few clicks.

For almost a decade, Max Freedman has been a trusted advisor for entrepreneurs and business owners, providing practical insights to kickstart and elevate their ventures. With hands-on experience in small business management, he offers authentic perspectives on crucial business areas that run the gamut from marketing strategies to employee health insurance.

At business.com, Freedman primarily covers financial topics, including debt financing, equity compensation, stock purchase agreements, SIMPLE IRAs, differential pay, workers' compensation payments and business loans.

Freedman's guidance is grounded in the real world and based on his years working in and leading operations for small business workplaces. Whether advising on financial statements, retirement plans or e-commerce tactics, his expertise and genuine passion for empowering business owners make him an invaluable resource in the entrepreneurial landscape.