Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Filing employee payroll taxes is important for any small business with employees. Here's how to do it.

Paying employees involves more than making sure they’re compensated accurately and on time. Employers are also responsible for calculating, deducting, setting aside and paying various payroll taxes. Whether you handle it yourself with payroll software, hire an accountant or bookkeeper or work with an outsourced payroll provider, getting payroll taxes right is critical.

In this guide, we’ll explain how employee payroll taxes work, what forms you’ll need to file and how to stay compliant throughout the year.

Employee payroll taxes are federal employment taxes employers must withhold, pay and report based on employee wages. These taxes typically include federal income tax withholding, Social Security tax, Medicare tax and federal unemployment tax.

Each tax has its own deposit schedule, reporting requirements and forms that must be submitted to the Internal Revenue Service. In addition to withholding payroll taxes from employee paychecks, employers are also responsible for contributing their share of certain taxes, depositing funds on time and filing accurate payroll tax reports.

“Payroll taxes include federal income tax, Social Security, Medicare and sometimes additional taxes such as unemployment (FUTA),” said Kraig Kleeman, founder and CEO of The New Workforce. “As an employer, you are responsible for withholding taxes from your employees’ wages and submitting them to the IRS. It sounds simple, but the process can be complicated if you don’t have a plan in place.”

Managing employee payroll taxes is a critical responsibility for employers. Staying compliant with federal regulations means completing the right forms, making timely payments and following a strict reporting schedule.

“I’ve worked with enough small business owners to know: Payroll taxes can be like a giant puzzle,” said Kleeman. “But the good news? After you have understood the different steps, it is not as complicated as it seems.”

Below is a step-by-step guide to help you navigate the process.

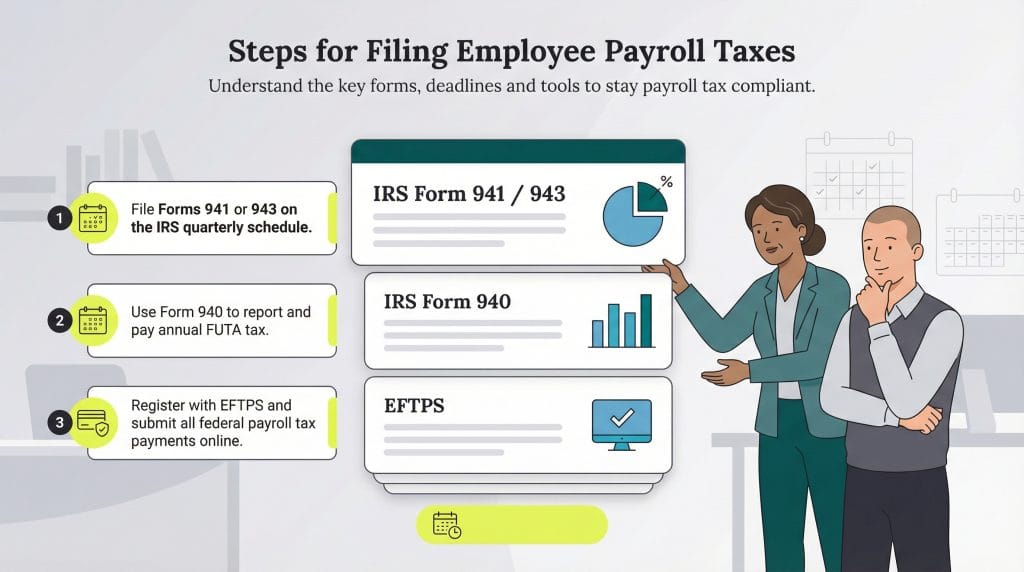

Before you can file employee payroll taxes, you need to know which IRS form applies to your business. Most employers will file one of the following payroll forms:

Some very small employers may be instructed by the IRS to file Form 944 (Employer’s Annual Federal Tax Return) instead of quarterly Form 941. If Form 944 applies to your business, the IRS will notify you directly.

“This is where the paperwork comes in,” Kleeman told business.com. “For most businesses, you’ll need to file IRS Form 941 quarterly. This form reports the wages, withholding taxes, and Social Security and Medicare contributions that you and your employees share.”

Federal unemployment tax, or FUTA, is separate from the payroll tax forms you file for employee wages and tax withholdings. Employers generally must pay FUTA if they paid $1,500 or more in employee wages during any calendar quarter in the current or previous year, or if they had at least one employee working for part of a day during 20 or more different weeks during the year.

If your business meets either threshold, use IRS Form 940 to report your annual federal unemployment tax liability. Form 940 is generally due by Jan. 31.

Although Form 940 is filed annually, employers must calculate their FUTA liability each quarter. Once your cumulative FUTA tax reaches $500, you must deposit the amount owed. If your balance is less than $500, you can carry it forward to the next quarter until you reach the deposit threshold.

Most employers make federal payroll tax deposits electronically, and the Electronic Federal Tax Payment System (EFTPS) is one of the most common ways to schedule and track payments with the IRS. EFTPS is a free service from the U.S. Department of the Treasury that allows businesses to submit payroll tax payments online or by phone.

To enroll, visit EFTPS.gov, select Enroll, then choose Business. You’ll need your employer identification number (EIN), business bank account information and routing number to complete registration.

If you’re a new employer that indicated a federal tax obligation when applying for an EIN, the IRS may automatically pre-enroll your business in EFTPS. If not, you can register directly through the EFTPS website. New enrollments typically take up to five business days to process, and your PIN is mailed to your business address on file.

“Any employer who is required to submit federal payroll taxes — including income taxes, Social Security and Medicare taxes — must register for the Electronic Federal Tax Payment System (EFTPS),” said Max Shak, CEO and founder at Zapiy. “This system allows businesses to make electronic payments to the IRS and ensures compliance with deadlines.”

Employers must submit the appropriate payroll tax forms — typically Form 941, Form 943 or Form 940 — by their quarterly or annual deadlines.

Note: Keep in mind that filing and paying payroll taxes don’t always happen at the same time. Payroll tax deposits are typically made throughout the quarter on a monthly or semiweekly schedule, while forms are generally filed quarterly or annually.

Most businesses file electronically through payroll software, an accountant or bookkeeper, or an IRS-authorized e-file provider. However, employers can also download fillable PDF versions of these forms from the IRS website, print them and mail them using the filing instructions provided with each form.

Paper filing may take longer to process, but it can be a practical option for smaller businesses that prefer to handle payroll tax reporting manually. Whether you file electronically or by mail, keep copies of submitted forms, payment confirmations and payroll records for your files.

“Filing on time is just as important as paying on time,” said Kleeman. “Good recordkeeping and consistent processes can help employers avoid unnecessary penalties and headaches.”

When it’s time to deposit your payroll taxes, use EFTPS to deposit the federal income tax withholdings, Social Security taxes, Medicare taxes and unemployment taxes you reported on Forms 940, 941 or 943.

Note: Submitting a payment through EFTPS does not replace your filing responsibilities. Employers must still file the appropriate payroll tax returns by their required deadlines.

To make a payment through EFTPS:

The payment is debited directly from your business bank account and submitted to the IRS. After completing your payment, you’ll receive a tracking number for your records.

To receive credit for paying on time, schedule your EFTPS payment no later than 8 p.m. ET on the day before the tax due date.

“It’s essential to meet these deadlines, as late payments can result in penalties and interest. My advice? Schedule reminders or automate payments if you can,” said Kleeman.

Employers must deposit payroll taxes with the IRS on either a monthly or semiweekly schedule, depending on how much payroll tax they reported during the IRS lookback period. Businesses with smaller payroll tax liabilities typically deposit monthly, while employers with larger liabilities usually follow a semiweekly schedule.

Most employers will follow one of these schedules:

“It can be a hassle to make regular deposits, but they are not negotiable,” Kleeman stressed. “Think of them as a way to stay ahead of the curve. Waiting too long or skipping payments can lead to more serious problems later. A small business owner I worked with missed a payroll tax deposit by a few days and it turned into a nightmare of penalties and additional paperwork. This is a mistake you should definitely avoid.”

In addition to Forms 940, 941 and 943, some employers may need to complete additional payroll reporting forms, year-end wage statements or information returns, depending on their business structure, employee compensation and reporting requirements.

Common payroll reporting deadlines include the following.

Due Jan. 31:

Due Feb. 28 (paper filing):

Due March 31 (electronic filing):

Missing filing or deposit deadlines can trigger IRS penalties, so it’s important to track both payment schedules and reporting due dates throughout the year.

Filing and paying employee payroll taxes is a critical part of running a business and staying compliant with federal regulations. By understanding the forms, deadlines and payment requirements involved, employers can avoid costly penalties and keep operations running smoothly.

“It may not be fun, but it is manageable,” said Kleeman. “By staying organized, meeting deadlines and using tools like EFTPS, you can take the stress out of the process.”

Reviewing your payroll obligations regularly, keeping accurate records and following IRS deadlines can make payroll tax compliance much easier to manage. With the right tools and a consistent process in place, payroll taxes can become a predictable and far less stressful part of running your business.

Amanda Clark and Jennifer Dublino contributed to this article. Source interviews were conducted for a previous version of this article.