Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is SUTA Tax? How Do You Calculate It?

Understand your state’s unemployment tax and how it is calculated.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Managing employees comes with significant responsibilities, including running payroll. A crucial part of managing your team’s compensation is ensuring you withhold the correct federal and state taxes — particularly state unemployment tax, more commonly known as SUTA tax. Whether you handle payroll in-house or rely on an outsourced provider, understanding how SUTA tax works and how it’s calculated is essential for staying compliant and avoiding costly penalties.

Searching for payroll software or services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

What is SUTA tax?

Employers pay the SUTA tax based on a state-set annual wage base.

State Unemployment Tax Act (SUTA) tax — also known as state unemployment insurance (SUI) or reemployment tax — is a component of a business’s payroll taxes. SUTA tax funds each state’s unemployment insurance program, which covers benefits paid to displaced and unemployed workers.

Each state determines which employers are required to pay this tax. “This tax provides unemployment benefits to workers who lose their jobs through no fault of their own,” explained Armine Alajian, founder and CPA at Alajian Group, Inc.

Did You Know?

Although you can manually calculate your SUTA tax, using a payroll software solution is much easier. The best online payroll services have built-in tax rate and wage base updates.

Who pays SUTA tax?

In most states, SUTA applies only to employers, not employees. Unlike Social Security, for example, which is withheld from all employees’ paychecks, employers usually pay all SUTA taxes.

The only states that require employees to pay state unemployment taxes are Alaska, New Jersey and Pennsylvania. Businesses with employees in these three states must withhold SUTA tax from their employees’ wages and pay those collected taxes to the state.

Most employers, including those with at least one employee, are subject to SUTA taxes. However, some exemptions — which vary from state to state — exist based on the number of employees and the duration of their employment.

FYI

In certain states, some organizations are exempt from paying SUTA. For example, certain nonprofits, government entities, religious institutions and educational organizations do not have to pay SUTA taxes nor other payroll liabilities.

What is the difference between SUTA and FUTA tax?

The Federal Unemployment Tax Act (FUTA) is a federal payroll tax employers pay on employee wages. Employees are exempt from FUTA, so they do not pay this tax. The FUTA tax rate is 6 percent on the first $7,000 of an employee’s earnings; the tax does not apply to earnings over $7,000. The maximum FUTA tax an employer is required to pay is $420 per year per employee before accounting for any credits.

FUTA taxes are generally paid quarterly (four times per year). Insurance premiums and certain fringe benefits are exempt from FUTA.

The SUTA tax is a state tax and is separate from the FUTA tax. However, businesses that pay their SUTA tax on time are eligible to receive a FUTA tax credit of up to 5.4 percent. This can reduce the employer’s total FUTA liability to 0.6 percent of the first $7,000 in wages per

Tip

Tip

Be sure you understand the system in order to not waste any money. These books can offer insight:

“Controlling Unemployment Insurance Costs”: Learn how to control and to dramatically reduce unemployment insurance compensation taxes. Get on Amazon

“The Economics of Unemployment Insurance”: Understand the role unemployment insurance plays in a high-employment economy. Buy on Amazon

“Unemployment Insurance Reform: Fixing a Broken System”: Insights into how our current unemployment insurance legislation can be improved. Order on Amazon

What is the SUTA wage base?

Each state determines its SUTA tax wage base each year. The wage base is the maximum amount (or threshold) of an employee’s income that the state can tax within a calendar year. Employers pay taxes on an employee’s wages until they meet this wage base.

All employers in the same state have the same SUTA wage base. Wage bases vary from state to state and are adjusted periodically, so it’s important to verify your state’s current figure each year. For example, in 2026, employers in Washington have a SUTA wage base of $78,200, while states like Florida set their wage base at $7,000 — the same floor as FUTA. All nonexempt employers must pay SUTA tax on each employee’s wages until that employee reaches their state’s wage base threshold for the calendar year.

SUTA wage base by state

Below is each state’s wage base for 2026:

Alabama: $8,000

Alaska: $54,200

Arizona: $8,000

Arkansas: $7,000

California: $7,000

Colorado: $30,600

Connecticut: $27,000

Delaware: $14,500

District of Columbia: $9,000

Florida: $7,000

Georgia: $9,500

Hawaii: $64,500

Idaho: $58,300

Illinois: $14,250

Indiana: $9,500

Iowa: $20,400

Kansas: $15,100

Kentucky: $12,000

Louisiana: $7,000

Maine: $12,000

Maryland: $8,500

Massachusetts: $15,000

Michigan: $9,500

Minnesota: $44,000

Mississippi: $14,000

Missouri: $9,500

Montana: $47,300

Nebraska: $9,000 ($24,000 for experienced employers)

Nevada: $43,700

New Hampshire: $14,000

New Jersey: $44,800

New Mexico: $34,800

New York: $13,000

North Carolina: $34,200

North Dakota: $46,600

Ohio: $9,000

Oklahoma: $25,000

Oregon: $56,700

Pennsylvania: $10,000

Puerto Rico: $7,000

Rhode Island: $30,800 ($31,800 for employers in the highest UI tax rate group)

South Carolina: $14,000

South Dakota: $15,000

Tennessee: $7,000

Texas: $9,000

Utah: $50,700

Vermont: $15,400

Virgin Islands: $32,100

Virginia: $8,000

Washington: $78,200

West Virginia: $9,500

Wisconsin: $14,000

Wyoming: $33,800

States may update their SUTA wage bases, so check your state’s Department of Labor website for the most accurate information.

FYI

Like Form 941 for quarterly payroll taxes, SUTA tax payments are due quarterly, usually within a month of each quarter's end.

What are SUTA tax rates?

The other key component in calculating your SUTA tax is the tax rate. Like the wage base, the tax rate varies by state. Additionally, when starting a new business, employers are subject to the new employer SUTA tax rate. Once a business becomes more established, the state assigns it a new tax rate within its employer tax rate range.

Some states also base SUTA tax rates on the industry. Construction businesses tend to pay higher SUTA tax rates than companies in nonconstruction industries. For example, in Ohio, new construction employers pay a SUTA tax rate of 5.85 percent (as of 2026), while the new employer SUTA tax rate is 2.85 percent.

Here are the new employer tax rate and the standard employer tax rate ranges for each state.

State

SUTA new employer tax rate

Tax rate range for positive to negative balance employers

Alabama

2.7%

0.14%–5.34%

Alaska

1.5% standard rate (0.50% employee share)

1.50%–5.90%

Arizona

2.00%

0.03%–8.36%

Arkansas

2.0%

0.2%–10.1%

California

3.4%

1.5%–6.2%

Colorado

3.05%

0.56%–7.34%

Connecticut

1.9%

1.10%–9.90%

Delaware

1.0%

0.3%–5.4%

District of Columbia

2.7% or average rate of employer contributions in the preceding year, whichever is greater

To calculate your SUTA tax as a new employer, multiply your state’s new employer tax rate by the wage base.

For example, if you own a nonconstruction business in California (as of 2026), the SUTA new employer tax rate is 3.4 percent, and the taxable wage base per worker is $7,000. That means you would owe $238 (0.034 x $7,000) per employee.

The same calculations are done for businesses assigned an established business tax rate: Multiply the tax rate by the taxable wage base.

Tip

Choose a payroll provider that can help you reduce tax calculation errors and stay on top of frequently changing wage bases and tax rates.

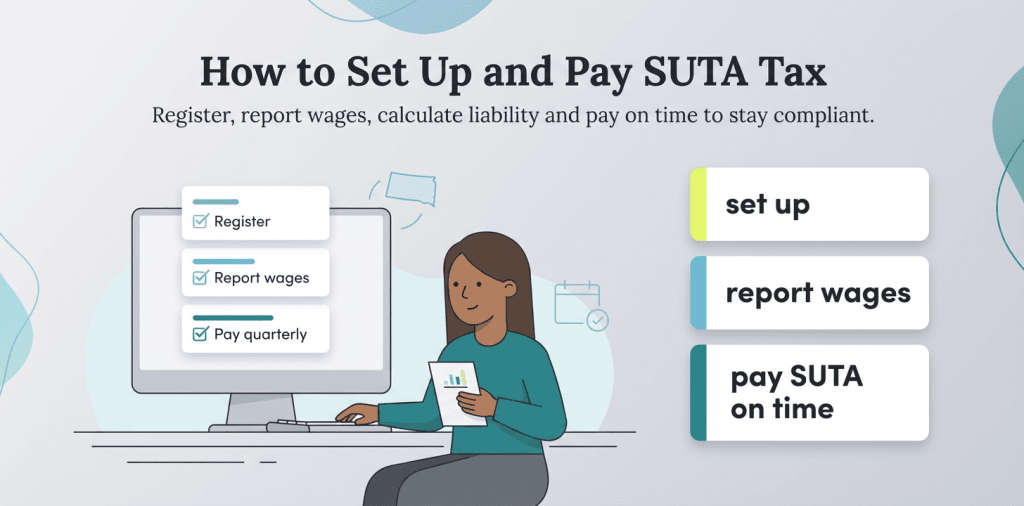

How do you set up and pay SUTA tax?

Paying SUTA taxes requires a company to do several things, including reporting wages and paying taxes on time.

While each state has its own process for registering as a new employer and setting up a state unemployment tax account, nearly all states require certain key items, including the following:

Employer identification number (EIN): An EIN enables the IRS to identify your business on tax returns. It’s often required to register with your state’s unemployment department.

Enrollment in the Electronic Federal Tax Payment System (EFTPS): The EFTPS allows employers to pay employment taxes online or over the phone.

New-hire reporting account: This account allows employers to report newly hired employees. This practice helps the government collect child support, prevent unemployment insurance fraud and identify unlawful welfare assistance.

Proof of workers’ compensation insurance: A workers’ compensation insurance policy provides wage protection and medical benefits to employees who have been injured on the job.

Each employer is responsible for reporting their SUTA tax liability to their respective state and making timely tax payments. “SUTA is usually paid quarterly with first-quarter taxes (January-March) paid in April,” Alajian explained. “Some states require monthly payments and might have other specific rules. Not paying or paying late may result in a penalty, interest, loss of benefits, legal consequences and could impact business operations.”

Once you’ve gathered the above requirements, follow these steps to set up and pay your SUTA tax:

Register with your state’s unemployment insurance department: Each state’s department has a different name. Conduct an internet search on “unemployment insurance department [state]” to find the one in your state. Some states have a paper form you must complete and return, while others have an online portal.

Report wages monthly: Report all wages for both full-time and part-time employees. To avoid duplicating wages, each reference period must include the 12th of the month. This interval will depend on how frequently you run payroll. Every state has different payroll reporting procedures that may include reporting by mail or online.

Calculate your quarterly SUTA tax due: Use your state’s wage base and tax rate to calculate the SUTA tax due for each employee for the quarter. Some states’ online tax portals may calculate this amount based on your reported wages.

Pay SUTA tax quarterly: Submit your payment to your state’s unemployment insurance department by the deadline each quarter. This may be by mail or online, depending on your state. Check with your state to learn about specific payment instructions.

Antwyne DeLonde, founder and CEO of VisionX, emphasized the importance of seeking current information. “It’s best to reach out to your state labor department for updated rates and thresholds, understanding that most payments are due quarterly,” DeLonde advised.

Jennifer Dublino contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.

David Gargaro has over 25 years of hands-on experience in the business arena. In 2018, he penned "How to Run Your Company… into the Ground," drawing insights from his direct involvement in small business operations. His practical guide covers a spectrum of topics, including strategic partnerships, product development, hiring and expansion strategies.

At business.com, Gargaro provides guidance on business insurance (errors and omissions, product liability, workers' compensation, etc.) and sales (sales funnels, lead generation, building a sales process, etc.).

Gargaro has also developed toolkits for startup founders, assisting them in navigating the complexities of entrepreneurship. He is a professional speaker as well, addressing audiences on topics such as the customer experience. Additionally, Gargaro's expertise in sales, marketing and financial planning has been featured in publications like Advisors Magazine, Moody's Analytics and VentureBeat.