Of your many responsibilities as a small business owner, ensuring that your employees’ pay is calculated accurately ranks near the top of the list. That includes withholding the correct amounts for federal income tax, state income tax, Social Security and Medicare. You also need to factor in other deductions, such as those for employee health insurance premiums and contributions to retirement accounts. These deductions are the difference between gross pay and net pay.

Failure to make the proper deductions from an employee’s wages or salary could get you in trouble with your staff and the IRS. However, preventing the headaches that stem from payroll mistakes isn’t difficult if you know how to properly calculate gross pay and net pay.

- Calculate gross pay per pay period

- Add bonuses and commissions if applicable

- Factor in overtime

What is gross pay?

Gross pay is the amount of an employee’s salary or wages before any deductions. For example, if an employee has a salary of $35,000 per year, that employee’s gross pay is $35,000. The gross pay of an hourly employee who works 30 hours and makes $15 per hour is $450 for that pay period.

For an hourly employee, wages can include breaks, on-call time, overtime, travel time and training. Gross pay is the starting point for all calculations related to employee compensation and taxes.

What is net pay?

Net pay, commonly called “take-home pay,” is the amount paid to employees after federal, state and local income taxes, as well as other deductions for health insurance premiums and contributions to retirement accounts, have been withheld from their gross wages or compensation.

Gross pay is the total amount of an employee's salary before deductions, while net pay is the amount paid to employees after taxes and other deductions have been made to their gross compensation.

How do you calculate gross pay?

Because you don’t pay employees for an entire year of work in a single paycheck, you need to know how to calculate gross and net pay for each pay period, which could be weekly, biweekly, semimonthly or monthly.

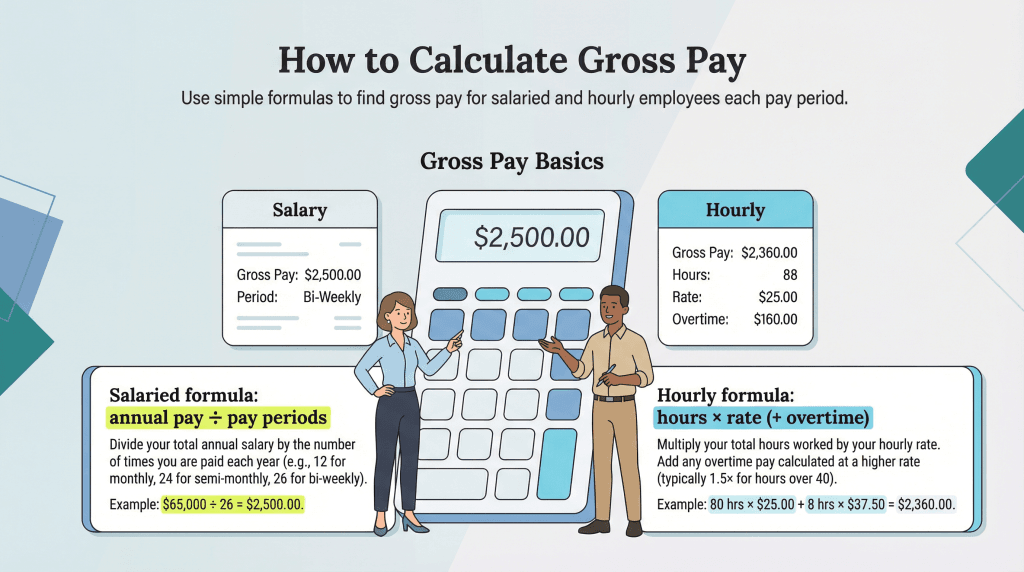

Gross pay for salaried employees

Follow these steps to calculate gross pay per pay period for a salaried employee:

- Divide the annual gross pay by the number of pay periods in the year.

For example, if an employee has an annual salary of $35,000 and you pay them biweekly, this would be the calculation:

$35,000/26 = $1,346.15

- Add bonuses and commissions, if applicable.

The next step is to include any additional compensation the employee may have earned during the pay period. For example, if your business offers an annual holiday bonus of $100 per employee, payable in the last paycheck of the year, you would add $100 to the employee’s gross pay for the pay period. Using the example above, this would be the calculation:

$1,346.15 + $100 = $1,446.15

Gross pay for hourly employees

Follow these steps to calculate gross pay for an hourly employee:

- Multiply the hourly wage by the number of hours worked during the pay period for which you’re writing paychecks.

For example, if an employee is paid $15 per hour and worked 20 hours over a two-week pay period, this would be the calculation to determine their gross pay for the pay period:

$15 x 20 = $300

- Factor in overtime.

The next step is to add any overtime the employee worked. If you pay time and a half for overtime hours, the employee would receive the regular hourly wage of $15, plus 1.5 times the hourly rate, or $22.50, for each extra hour on the job. So, if the employee above worked five hours of overtime, this would be the calculation to find their gross pay:

$300 + ($22.50 x 5) = $412.50

How do you calculate net pay?

- Subtract pretax deductions

- Calculate federal tax withholding

- Calculate state tax withholding

- Calculate FICA tax

- Deduct any wage garnishments

Using one of the best online payroll services makes deductions easy, but it’s still important to understand what goes into each section. Calculating an employee’s net pay for any pay period involves subtracting tax withholding and other payroll deductions from the gross pay for that pay period. Start with the gross pay for the pay period. Then, follow these steps:

1. Make voluntary pretax deductions.

Items in this category are deductions that aren’t required by law. Rather, employees opt to have them withheld from their paycheck to lower their taxable income and payroll taxes. For example, voluntary pretax deductions might include contributions to a retirement account, such a 401(k); some health benefits, such as a flexible spending account (FSA); and commuter benefits.

Pretax deductions are taken before mandatory payroll taxes are applied. This lowers the employee’s taxable income base. For example, if an employee contributes $75 per paycheck to a 401(k) plan and $50 per month to their health insurance premium, you would subtract those two amounts from their gross pay to figure out their net pay.

Voluntary tax responsibilities you can opt for include 401(k) plans or other retirement plans, FSAs and commuter benefits. Visit our

guide to employer taxes to read more about voluntary and mandatory tax responsibilities.

2. Subtract federal tax (mandatory payroll tax).

Here, you’ll need information about the employee’s filing status (single, married filing jointly, married filing separately, head of household, and widow or widower with dependent child) and withholding allowance. The withholding allowance refers to exemptions a taxpayer can lawfully take from their income to reduce the amount of income that would otherwise be taxed. Each exemption drives down the amount of tax you can deduct from an employee’s paycheck.

You can find filing status and withholding allowance details on IRS Form W-4, Employee’s Withholding Certificate, which an employee must complete and submit to you upon starting work at your company. It’s illegal for an employer to assist an employee in filling out Form W-4, but you’re allowed to refer them to the IRS’ withholding estimator tool.

You also need the IRS’ tax withholding tables, which can be found in the agency’s Publication 15-T. IRS Publication 15-T (2026)-Federal Income Tax Withholding Methods contains the most current tables. The tables provide the correct percentage of federal income tax withholding from gross wages, based on an employee’s filing status, withholding allowance and the employee’s salary range.

3. Deduct state and local tax (mandatory payroll tax), if applicable.

Unlike federal tax withholding, state tax withholding rates vary from state to state. There’s no withholding to consider in Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington or Wyoming, as these states don’t tax income. Likewise, state withholding doesn’t come into play in New Hampshire because it taxes interest and dividend income only, not salary and wages. Note, too, that while Washington does not have a general personal income tax, a capital gains tax may apply to high earners, and the WA Cares Fund payroll tax applies to employee wages.

You may need to deduct state income tax from more than one state if an employee works in one state and lives in another. However, some states maintain reciprocity agreements and don’t tax out-of-state income. Illinois and Iowa fall into this category. This means that if you have an employee who lives in Illinois but works in Iowa, you wouldn’t deduct state withholding for that employee.

4. Deduct the FICA payroll tax.

Federal Insurance Contributions Act (FICA) payroll tax is made up of Social Security and Medicare tax. To calculate it, multiply the employee’s gross pay for the pay period by 7.65 percent. Of this 7.65 percent, 6.2 percent is for Social Security and 1.45 percent is for Medicare.

Here is the calculation for the FICA tax deduction for the salaried employee who earned the $100 bonus above:

$1,446.15 x 0.0765 = $110.63

Here is the calculation for the hourly employee who worked five hours of overtime:

$412.50 x 0.0765 = $31.56

There are a few caveats to keep in mind with FICA. For example, each year, the Social Security Administration sets a maximum withholding based on cost-of-living expenses. Once an employee’s annual gross pay reaches this threshold — which is $184,500 for 2026 — you withhold Social Security tax only up to that amount, and not for any pay exceeding that threshold.

Additionally, in 2013, the IRS implemented the Additional Medicare Tax. Employers are now responsible for withholding an additional 0.9 percent from an employee’s gross wages or salary if they reach a certain threshold. The applicable threshold depends on the employee’s tax filing status. Currently, it’s $250,000 for married filing jointly, $125,000 for married filing separately, $200,000 for a single filer, $200,000 for a head of household with a qualifying individual, and $200,000 for a qualifying widow or widower with a dependent child.

Calculating an employee’s net pay involves withholding taxes and other payroll deductions, including voluntary pretax deductions, mandatory payroll taxes and the FICA payroll tax.

5. Make other mandatory payroll deductions.

An employee may be subject to wage garnishments for back child-support payments, delinquent student loans, unpaid taxes and/or credit card debt. In these instances, you’ll receive a notice from the federal or state government alerting you to the required wage garnishments. The notice will indicate the exact amount to withhold from each paycheck. [Read more about how to do payroll for your business.]

You can easily calculate net pay by using our free payroll deductions calculator tool. Additionally, the IRS’ Employer’s Tax Guide (publication 15) incorporates withholding information and instructions for withholdings.

Kimberlee Leonard and Sean Peek contributed to the reporting and writing in this article.