Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Ask yourself these questions to determine whether buying or leasing is the right decision for your business.

You need a new company car. Should you buy or lease? The fundamental difference between the two options lies in ownership and financial commitment. When you lease, you’re essentially renting the vehicle for a predetermined period with lower monthly payments but no equity building. Purchasing means you own an asset that can provide long-term value but requires higher upfront costs and monthly payments

The decision between leasing and buying involves multiple financial and operational factors that vary by business type and usage patterns. This comprehensive guide examines cost comparisons, tax implications, cash flow considerations and industry-specific recommendations to help you determine which option aligns best with your business goals.

Understanding the financial implications over time helps business owners make informed vehicle decisions. Monthly lease payments are typically lower than loan payments for the same vehicle, but purchasing builds equity that can offset higher costs.

Leasing or buying a car for your business depends on your unique circumstances. Consider the following questions. Their answers will lead you in the right direction.

You must understand how far you’ll drive the car and how many miles it will rack up. Leases typically come with an allowance of up to 12,000 miles per year. This means that when you return the car, it must be at that mileage or under. If you lease the car for three years, at the end of the lease, that means 36,000 miles. Some leases allow for a little more, such as 15,000, or a little less like 10,000. If you go over the mileage allowance, you’ll be charged a certain rate per mile — and it can get expensive quickly. For example, exceeding lease limits by just 3,000 miles during a three-year lease with a $0.25 per-mile penalty results in a $1,500 charge upon return.

“If you plan to drive long distances regularly — such as for work commutes, road trips or business travel — buying a car is the better option since there are no mileage restrictions,” Wes Lewins, chief financial officer at Networth.com, told us. “On the other hand, if you drive less and stay within mileage limits, leasing may be a more cost-effective choice with lower monthly payments.”

Another essential consideration is knowing how much you can put toward a down payment. When you lease a car, you may need less money up front, and some leases don’t require a down payment at all.

Generally, the less you put down, the higher your monthly payment. However, even with a slightly higher payment, lease payments are still lower than financing payments. Let’s look at an example for a $40,000 vehicle with a negotiated price of $38,000. If you lease it, you might put $2,500 down and pay $420 per month for 36 months, since the down payment mostly covers fees and part of the car’s depreciation. If you purchase the same vehicle with a loan, you might put $5,000 down and still face payments of about $700 per month for 60 months, because your down payment reduces the overall loan balance instead of just the lease cost.

Many advisors say you should put the lowest amount possible for a down payment when leasing a car. In contrast, when financing a car, you’ll want to put more money into a down payment to help decrease your monthly payment.

“Buying a car may have higher up-front costs but provides long-term savings since there are no ongoing lease payments after the loan is paid off,” said Rose Jimenez, chief finance officer at Culture.org. “Leasing, however, offers lower monthly payments and may require little or no down payment, making it easier for those with limited cash flow to drive a newer car. To decide, buyers should calculate the total cost of ownership over five to 10 years, considering maintenance, insurance and depreciation.”

Business vehicle tax benefits vary significantly between leasing and purchasing, with each option offering distinct advantages depending on your specific tax situation.

When leasing a vehicle for business purposes, monthly lease payments are typically fully tax-deductible as business expenses, proportional to business use. If you use your leased vehicle 70 percent for business, you can deduct 70 percent of the payments.

For luxury vehicles valued above $62,000, the IRS requires an “income inclusion amount” that reduces your deduction for leases starting in 2024. You can also claim the standard mileage rate (67 cents per mile in 2024) instead of actual expenses, but you must maintain that method throughout the entire lease period.

Purchased business vehicles unlock significant tax advantages through depreciation deductions. For vehicles bought and placed in service in 2024, you can potentially claim a first-year depreciation deduction of up to $20,400 (including bonus depreciation).

Section 179 allows businesses to immediately expense qualifying vehicle purchases rather than depreciating them over time. For 2025, the maximum Section 179 deduction has been significantly increased to $2.5 million with a phase-out threshold beginning at $4 million. For vehicles weighing over 6,000 pounds but not exceeding 14,000 pounds, the maximum deduction is $31,300.

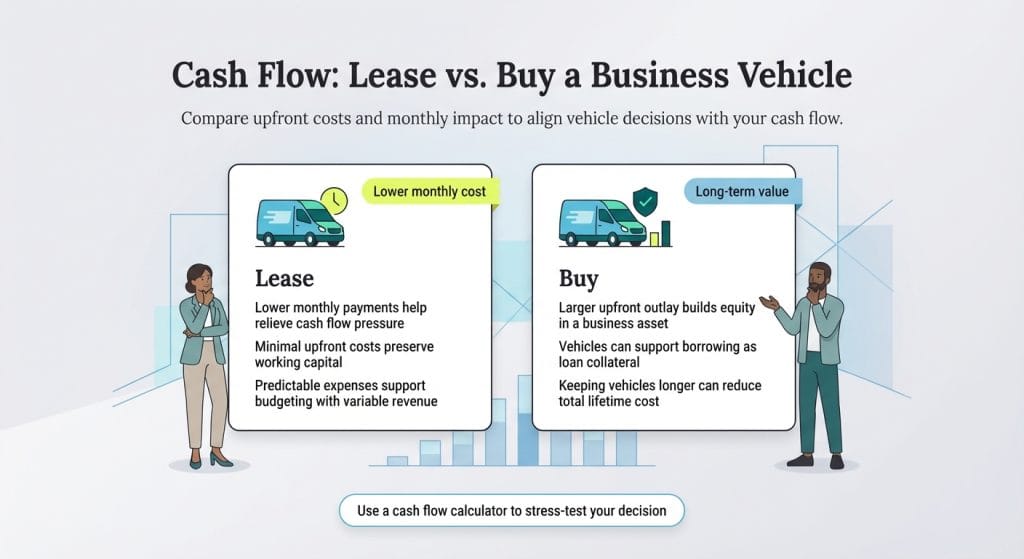

Cash flow implications differ dramatically between leasing and purchasing, affecting your business’s available capital for other investments and day-to-day operations.

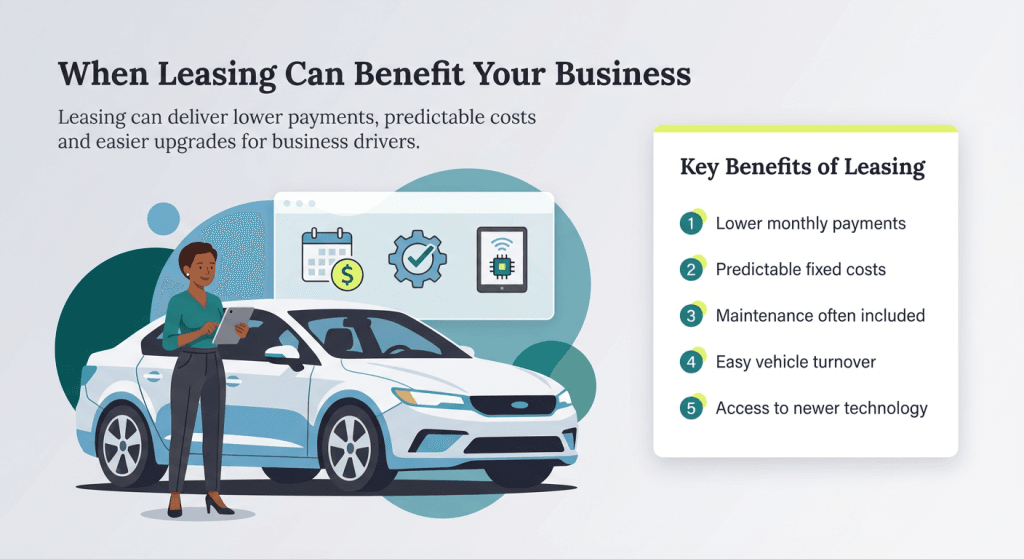

Lease payments are consistently lower than loan payments for the same vehicle, providing immediate cash flow relief for businesses managing tight budgets. The monthly savings with leasing can free up cash for other business investments such as inventory, marketing or equipment upgrades. Businesses with variable revenue streams particularly benefit from the predictable, lower monthly expenses that leasing provides.

The upfront financial commitment varies significantly between the two options, directly impacting your business’s working capital.

Purchasing typically requires a substantial down payment – approximately 20 percent of the vehicle’s cost – plus all sales taxes upfront. This immediate outlay can strain cash reserves and limit funds available for other business opportunities.

Leasing requires much less money upfront, with many agreements needing minimal initial payments and some requiring no down payment at all. You might only need to cover the first month’s payment and a security deposit. With leasing, sales tax spreads across your monthly payments in most states rather than requiring immediate payment on the entire vehicle value.

Leasing preserves working capital that can be deployed for revenue-generating activities, making it particularly attractive for growing businesses and startups. The lower monthly commitment allows businesses to maintain financial flexibility for unexpected opportunities or seasonal fluctuations.

Purchasing builds equity in a business asset but ties up more capital initially. While this creates long-term value, it may limit short-term financial agility. However, owned vehicles can serve as collateral for business loans and contribute to your company’s balance sheet strength.

For businesses with consistent cash flow and long-term vehicle needs, the higher upfront costs of purchasing often result in lower total costs over time, especially when vehicles are kept beyond the typical lease term.

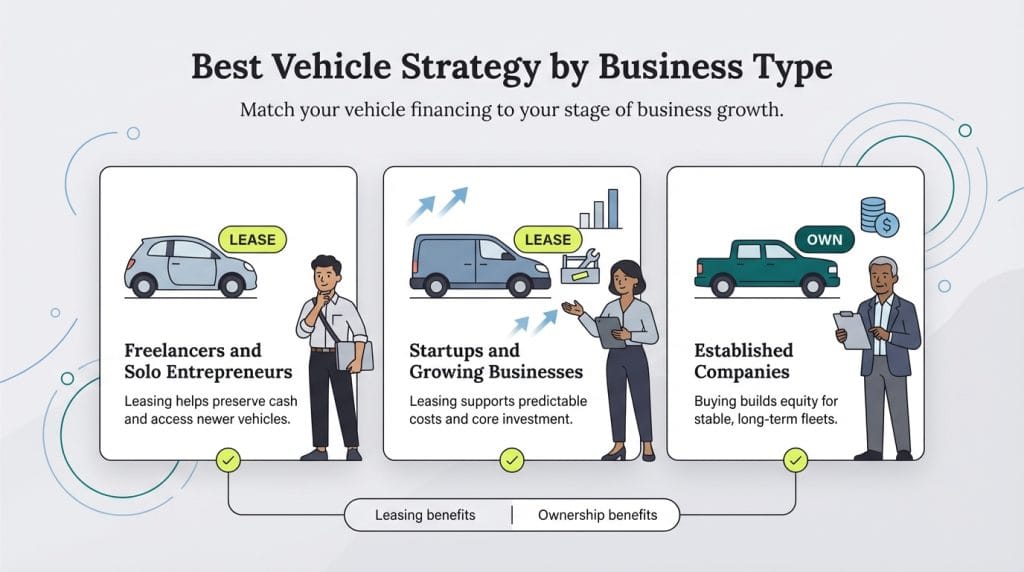

Different business types benefit from different vehicle acquisition strategies based on their unique operational needs, cash flow situations and growth plans.

Leasing a car can be a great option for business owners who prefer lower monthly payments and the ability to upgrade to a new vehicle every few years.

Buying a car offers several benefits like full ownership, customization freedom and long-term cost savings.

Factor | Leasing | Buying |

|---|---|---|

Monthly Payments | Lower | Higher |

Upfront Costs | Minimal to none | 20 percent down payment typical |

Ownership | No equity building | Build asset value |

Mileage | Limited (10,000 to 15,000/year) | Unlimited |

Customization | Restricted | Complete freedom |

Tax Benefits | Deduct monthly payments | Depreciation + Section 179 |

Maintenance | Often included | Owner responsibility |

Early Exit | Penalty fees | Sell anytime |

You should buy a company car if:

You should lease a company car if:

Amanda Hoffman contributed to this article. Source interviews were conducted for a previous version of this article.