Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

How Do Commercial Car Insurance Deductibles Work?

Commercial car insurance deductibles work just like personal auto insurance deductibles. Learn about collision and comprehensive claims deductibles.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

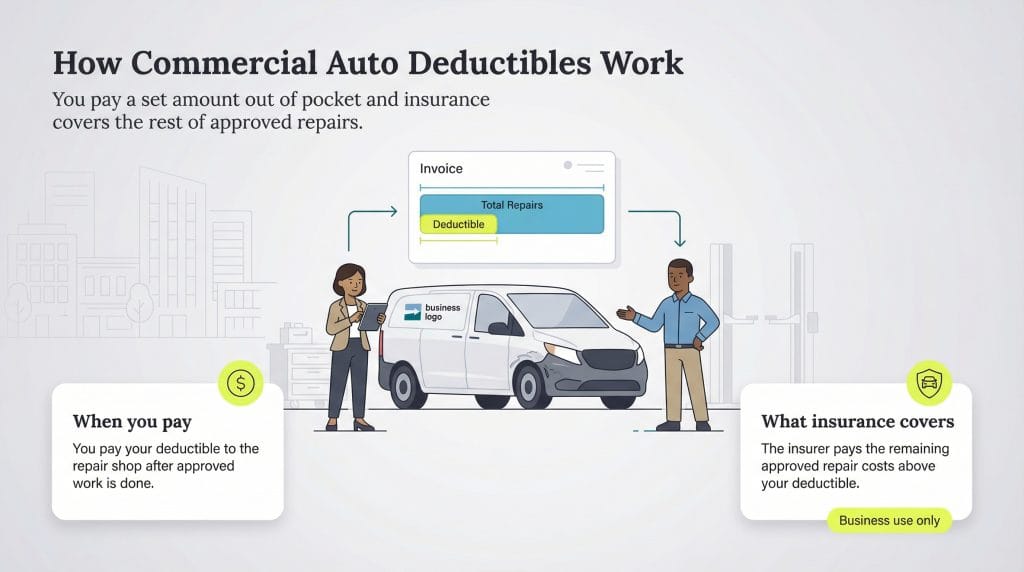

The deductible on a commercial car business insurance policy works the same as it does for personal auto insurance. The deductible is the amount you’ll pay when there’s a claim on your policy. Consider the deductible the “self-insured” part of the policy where you are responsible for paying for a portion of the repairs.

Here’s a look at what a business owner needs to know about commercial auto coverage and deductibles.

What are auto insurance deductibles?

Your insurance deductible is the amount you’ll pay out of pocket after you file an insurance claim because of an incident with your covered business vehicle.

Deductible amounts vary; you and your insurer will determine your deductible amount when you agree on the policy. “So, if you have a $1,000 deductible and you file a $5,000 claim, you’d pay the first $1,000 and the insurer would cover the rest,” according to Chris Peterie, CEO and co-founder of Tower Street Insurance. However, policyholders can change the deductible amount in the middle of a policy by contacting their insurance carrier.

The deductible shows up on collision and comprehensive claims but doesn’t apply if another car hits you and you need to get your vehicle repaired.

How do deductibles work for commercial auto insurance?

You pay the deductible when you get your car repaired. You’ll usually pay the deductible directly to the auto body shop before it releases your vehicle back to you. “In commercial auto insurance, deductibles are often customized to reflect things like fleet size and intensity of use,” according to Dennis Shirshikov, adjunct professor of economics at City University of New York.

For example, let’s say you were in an at-fault accident that damaged your vehicle and your deductible is $500. Your first step is to file a claim with your insurance carrier to explain the accident’s circumstances. Next, the insurance carrier sends an adjuster to assess the damage and estimate what repairs would cost. In this case, let’s say the adjuster notes $5,000 in damages.

Next, you’ll bring your car to a repair shop and provide the claim information. When your car is fixed, the shop will bill your insurance carrier for the total amount minus the deductible. When you pick up your car, you’ll pay your $500 deductible to the shop and leave with your newly repaired car.

Did You Know?

When considering insurance expenses and tax deductions, you can deduct your commercial auto insurance premiums and expenses if you use a vehicle exclusively for business purposes.

Types of commercial auto insurance deductibles

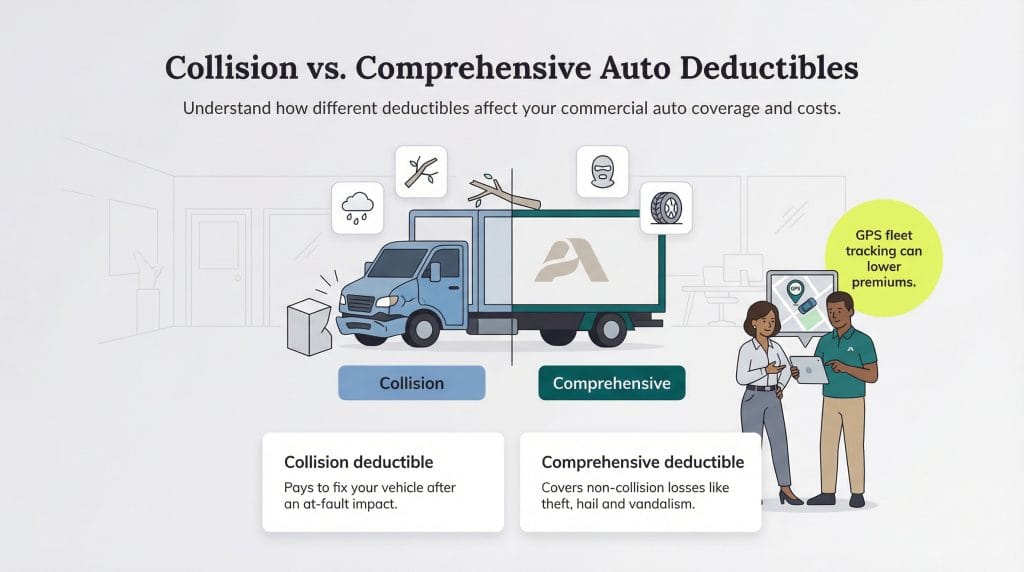

Commercial auto insurance deductibles apply only to your insurance policy’s comprehensive and collision coverages. You can choose a separate deductible for each coverage to customize your policy.

Collision coverage deductible

Collision coverage pays for repairing or replacing your vehicle if you hit something – a car, building, object or animal – and are at fault in the accident. Collision coverage doesn’t cover damage to what you hit; your general liability insurance covers those damages.

When you claim from your policy for collision coverage, you’ll need to pay the collision deductible. Deductibles vary from carrier to carrier, but most carriers offer policies that range from no deductible to a $2,000 deductible. Basically, the higher your deductible, the lower your premium will be.

Did You Know?

Many of the best GPS fleet tracking systems monitor driver behavior, record collision data and some even take video of road traffic accidents. While its impact on deductible costs is minimal, some insurers reduce premium costs for companies that have these systems installed on their fleet. In addition to insurance savings, GPS fleet tracking platforms can reduce fuel use and vehicle maintenance expenses.

Comprehensive coverage deductible

Comprehensive coverage kicks in for any type of loss other than a collision. For example, a comprehensive claim would cover someone stealing your car, a vandal slashing your tires or a tree branch falling on your car. Hail is another common source of comprehensive coverage claims. In most cases, having a comprehensive deductible is worth it, “especially if you have a fleet or expensive vehicles,” according to Peterie. “It’s typically affordable, and the peace of mind it provides is well worth it for most businesses.”

Comprehensive coverage also has its own deductible that you’ll set when you choose your business insurance policies. Like the collision deductible, it can range from nothing to $2,000, depending on the carrier. Also, as with the collision deductible, you’ll pay the deductible directly to the repair shop when you get your car fixed.

What is the average auto insurance deductible paid on commercial vehicles?

Policyholders can select a $250, $500, $1,000 or $2,000 deductible for both comprehensive and collision coverage. The higher the deductible, the lower the cost of your commercial auto insurance. Most drivers tend to take a middle ground, finding the sweet spot between cost and coverage with a $500 deductible.

Those who want additional savings might jump to a $1,000 deductible, while many find that a $2,000 deductible doesn’t provide enough savings to take on so much risk. [Learn about the best business insurance for your needs]

FYI

One way to save money on business insurance is to bundle your commercial auto policy with other insurance policies you purchase.

What to consider when choosing a commercial auto policy with deductibles

When it comes to your deductible amount, your decision boils down to cost versus risk. As an insurance policyholder, you want to save as much money as possible, so you may be tempted to go with a higher deductible and lower premium.

But when you look at what you’d have to pay out of pocket in a claim, consider whether or not the lower premium is worth it. For many people, coming up with an extra $1,000 for a claim would be difficult. Even $500 can be burdensome.

If the cost savings associated with a higher deductible aren’t substantial, you may be better off with a lower deductible while paying a few extra dollars a month for coverage. “Your starting point for the right deductible hinges on your company’s risk appetite, available cash reserves and strategizing the correct intersection between premium costs and the possible claim expense,” according to Shirshikov.

A commercial car insurance deductible doesn’t work like a health insurance deductible. In health insurance, the deductible goes toward the out-of-pocket maximum for the year. With auto insurance, there’s no ceiling; you’ll pay the deductible every time you file a collision or comprehensive insurance claim. So, if you have a $500 deductible and make three claims during your policy, you’ll pay a total of $1,500 to get your car repaired.

Choosing between a $500 and $1,000 deductible is a personal choice. Since this is the amount you’ll pay if you file a claim, you need to be comfortable with your out-of-pocket responsibility. A higher deductible can save you money on your insurance premium. You might be able to save as much as 40 percent on your premium when you jump from a $500 to a $1,000 deductible. If you aren’t likely to file many claims, the higher deductible may be a good option that’s worth it for the premium savings. If you have more frequent claims, consider a lower deductible to get the most out of your insurance.

As your car gets older, the cost of repairing it after an accident can exceed its fair market value. This means your car is likely to be totaled. If so, you’ll receive a check for its fair market value if you have comprehensive or collision coverage. For many, this is why paying for these coverages on an older car is often not worth it. When deciding if you should have a deductible on an older car, evaluate the amount you’d receive in a claim compared to what you’re paying for insurance. Some people decide to keep coverage in place because they feel getting something in a claim is better than nothing.

Splitting the deductible is when you choose different deductible options for collision and comprehensive coverage. For example, you might have a $500 collision deductible and a $250 comprehensive deductible. Traditionally, the comprehensive deductible affects premium pricing less, and many policyholders prefer carrying less responsibility for events where they’re not at fault. Other policyholders keep things simple and choose the same deductible for both comprehensive and collision coverage. This eliminates confusion in claims, and the policyholder doesn’t have to guess which deductible will apply.

A buydown or buyback deductible allows you, as an insurance policyholder, to pay an extra premium to reduce or “buy down” the deductible amount. It’s like paying a portion of your deductible upfront, meaning you pay a higher premium for your policy. Let’s say your auto insurance policy has a deductible of $1,000. You purchase a buydown from your auto insurer to reduce the deductible to $500. This makes sense if you’d struggle to meet a high deductible if an accident does happen, but you could afford to pay slightly more each month.

Mark Fairlie contributed to the reporting and writing in this article.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.