Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Business interruption insurance for unforeseen adverse events can help you cover lost income and other expenses.

An unforeseen adverse event, such as a fire, can devastate your small business’s operations. Although standard property insurance may cover specific types of property damage, business interruption insurance (also known as business income insurance) fills in the gap, addressing lost income and other issues that arise if your business shuts down unexpectedly.

Editor’s note: Looking for the right liability insurance for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

Here’s what business interruption insurance covers, how it works and how to obtain this coverage for your small business.

Business interruption insurance is an insurance policy that kicks in when a business can’t operate normally because a specified peril causes physical property damage, rendering the business inoperable. It covers operating expenses and other lost income for a specific period after the business shuts down. The policy spells out the types of unforeseen events that qualify for coverage.

You can obtain this type of business insurance as a stand-alone policy from many of the best commercial insurance providers. You can also include it in your business owner’s policy (BOP) or purchase it as an insurance rider or endorsement to add to a commercial property insurance policy or package.

According to Chris Peterie of Tower Street Insurance, business interruption insurance is about more than just the money. “Beyond the financial relief, it’s about giving you the breathing room to focus on what matters most — getting your business back on its feet,” Peterie explained. “It can even help preserve your relationship with customers and stakeholders by minimizing disruptions.”

Most business interruption insurance providers typically cover the following perils:

You must read your business interruption insurance policy documents carefully to understand precisely which perils your insurer covers. Here’s an example.

“We will pay for the actual loss of business income you sustain due to the necessary suspension of your ‘operations’ during the period of ‘restoration.’ The suspension must be caused by the direct physical loss, or damage, to property at premises … The loss or damage must be caused by or result from a covered cause of loss.”

Typical business interruption insurance policies include the following coverage areas, which may deviate slightly according to a carrier’s formula for calculating financial losses:

Dennis Shirshikov, an adjunct professor of economics at the City University of New York, noted that businesses must provide documentation to prove the extent of their losses. “Carriers often request financial accounts, tax returns, inventory data and extensive documentation of the incident’s effect,” Shirshikov explained.

Small business owners should understand the various types of business interruption insurance to determine which coverage suits their company best. Different policy types may include or exclude specific items. Below are standard coverage options for business interruption insurance.

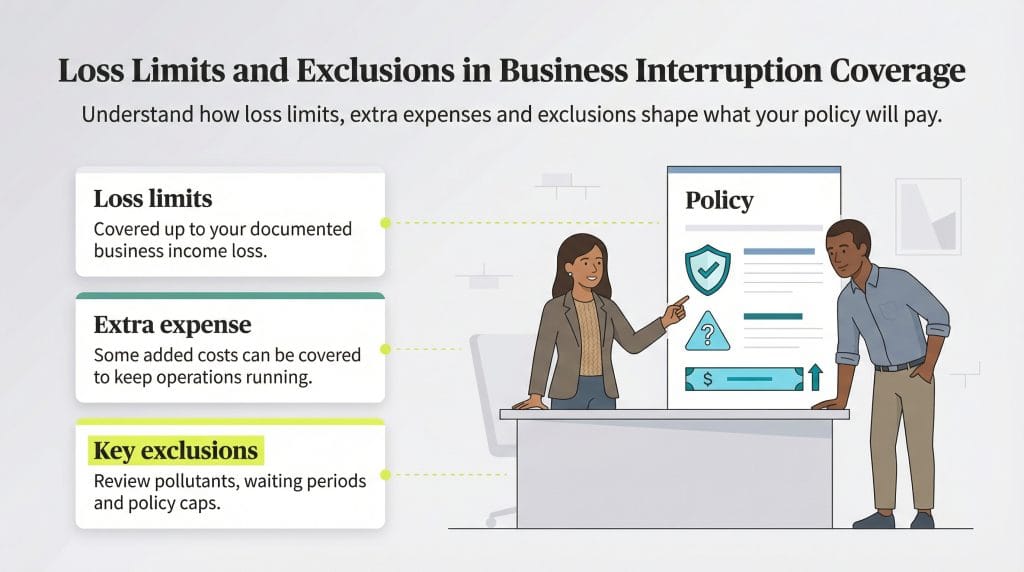

Business income coverage replaces lost income and covers ongoing expenses when a business temporarily shuts down due to a covered loss. It addresses revenue loss, payroll, rent, taxes and operational costs incurred during the closure period.

Extra expense coverage helps with costs not covered by property insurance as your business recovers from a disruption. This financial support helps businesses stay afloat during repairs, ultimately staving off a permanent closure.

Peterie offered an example: “Imagine a fire damages your office and you can’t use the space. To stay open, you decide to rent a temporary space, set up new equipment or outsource certain operations. These aren’t your everyday expenses.” Extra expense coverage handles these extra expenses to help you stay afloat.

Contingent business interruption coverage safeguards a business against losses resulting from third-party vendor disruptions. For instance, if a hurricane floods a supplier’s warehouse to the point of needing to pause equipment deliveries, this type of insurance could compensate for any income lost during the closure.

Civil authority coverage protects a business’s losses from closures or restrictions imposed by the government. While property insurance covers a closure due to damage, it may lack income coverage for any loss in revenue after the closure. Including civil authority coverage further extends business interruption coverage but often comes with time limits and a waiting period.

“Not all policies provide civil authority coverage by default,” Shirshikov cautioned. “While some do, others need it as an extra endorsement.”

Let’s say a fire damages your warehouse, leaving the building uninhabitable and destroying merchandise already packaged to send to customers. There are two primary ways business interruption coverage can reimburse you:

Review your business interruption insurance policy carefully because the insurer will have its own specifics on calculating lost income. Accounting criteria for lost income and expenses can include the following:

A restoration period is the time during which your business interruption policy will help pay for lost income and extra expenses while you reconstruct or restore the property to its original condition.

Read your policy documents carefully to understand when your restoration period starts and how long it lasts. The restoration period typically begins when the covered peril occurs and ends after a reasonable amount of time for the property to be restored and operations to fully resume.

For example, if your business was damaged on October 1, you’d obtain business interruption coverage benefits until October 1 of the following year (assuming your policy includes a 12-month restoration period), even if your policy expires before then.

If your business’s building repairs aren’t completed before the 12-month restoration period ends, your business interruption coverage will expire. This means you’d stop receiving reimbursement for lost income, for example. Check your individual policy for specifics.

When reviewing your business interruption coverage with a broker, you may want to discuss whether the following coverages are included or can be added as endorsements.

Business owners facing challenges during the restoration period can seek an endorsement that extends the restoration period by 30 days or more.

For example, if an insured business needs additional time to restore its property beyond the initial restoration period, it can purchase an extended period of indemnity endorsement. This endorsement typically allows for extensions in 30-day increments, ranging from as little as 30 days to up to 720 days. Check with your provider for specific options.

A coverage extension provides insurance for business income losses resulting from specified events, such as service interruption, contingent business interruption, leader property interruption and interruption by civil or military authority (for example, if a local, state or federal governmental entity restricts access to your property). A sublimit typically applies for each additional coverage.

You can include a service interruption extension in your business interruption policy, so ask your insurance provider for details. A service interruption extension typically provides business income coverage arising from direct physical loss, damage or destruction to any utility service’s transmission lines and related plants, substations and equipment supplying services to an insured business.

Restrictions may apply, such as waiting periods, distance limitations, the exclusion of certain perils, such as earthquakes and exclusions for overhead and transmission lines. The owners, managers or operators of such utilities or services are not named as insured under the policy. Again, check your policy specifics.

When a business income loss occurs, an insured business is obligated to take reasonable steps to prevent or minimize this loss and any further losses. Expenses incurred to reduce that loss may be covered under the policy as part of the business income loss as long as these expenses don’t exceed the actual loss.

For instance, if there is a business loss of $200 associated with the interruption of business operations, the insurer could reimburse $100 to reduce the loss but will not reimburse the business $100 if the claim is reduced by $50. If the business incurs other expenses above this claim amount to continue operating the business, those could be covered under an additional expense provision if one is included in the insurance policy.

It’s crucial to note policy verbiage and specifics. For example, insurer CNA’s policy details require “a direct physical loss” or damage that interrupts your business to qualify for coverage. Terms and exclusions may also limit or preclude coverage.

This “direct physical loss” and exclusions verbiage may determine whether the policy is upheld or denied in court.

Manufacturers should take note of exclusions for losses associated with pollutants and contaminants and information about deductibles, waiting periods and policy limits. This information is on the declarations page or within the section detailing your coverage.

Retailers and businesses in the manufacturing and service industries should consider business interruption insurance. Any business that provides a service or goods should also consider this coverage.

Speak with an insurance representative or agent about your specific business. When evaluating business interruption insurance, consider the following factors:

As with any business insurance policy, costs depend on underwriting standards, your business’s size and numerous other factors, including the following:

Contact an insurance broker or agent for specific business interruption insurance quotes.

Business interruption insurance premiums usually range from $40 to $130 monthly. Rates can be higher for businesses with higher liabilities.

You can purchase business interruption insurance via major insurers that cover commercial liability. Before purchasing a stand-alone policy for business interruption insurance, check if you already have existing coverage.

If you already have a BOP with your insurance company, check the policy details to see if business interruption coverage is included. Also, see if your general liability policy has an endorsement for business interruption insurance.

Business interruption insurance typically has a coverage limit — the maximum amount your insurer will pay toward a covered claim. You’ll pay out of pocket for any financial losses that exceed your coverage limit, so ensure the coverage amounts you elect are appropriate for your business; speak with your insurance agent if you need additional coverage.

As always, discuss any concerns with your insurance agent and refer to your company’s risk management plan to ensure adequate coverage.

Kimberlee Leonard contributed to this article.