Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Insurance is vital for small businesses to protect against risks, and costs vary based on factors, such as industry and coverage needs.

Insurance is a necessary investment for small businesses as it offers financial protection against various risks and losses that can occur during operations, including third-party injury claims, property damage, employee injuries and theft. A lack of insurance during a time of crisis can be devastating.

Your coverage and its ensuing costs will depend on your business and its specific risk factors. While most businesses with employees need essential business insurance, such as workers’ compensation, other policies can be just as crucial for comprehensive protection and peace of mind. As you shop for insurance, you’ll need to budget appropriately for your business needs. Here’s a look at the costs you can expect for suitable business coverage.

Business insurance costs depend on many factors, including your industry, number of employees and total revenue. A business’s claims history, chosen coverage, policy limits and deductibles can also affect costs. For example, “A general liability policy is determined by many criteria, including risk, kind of activities and firm size,” noted Dennis Shirshikov, adjunct professor of economics at City University of New York.

Every policy serves a different risk-protection purpose and is priced accordingly. Here are some of the most common types of business insurance and their average annual costs:

Policy type | Average annual cost |

|---|---|

General liability | $500 to $960 |

Business owner’s policy (BOP) | $684 to $1,019 |

Workers’ compensation | $540 to $600 |

Professional liability | $735 to $1,200 |

Commercial auto | $1,764 to $3,240 |

Commercial umbrella | $240 to $900 |

Sources: Insureon, Progressive Commercial and The Hartford

As this list demonstrates, insurance costs vary widely by policy type. Your business may spend more or less than these averages. High-risk industries or locations prone to natural disasters generally face higher premiums and the level of necessary coverage further determines overall costs.

“Different industries face unique risks, which directly impact insurance costs,” explained Chris Peterie of Tower Street Insurance.

Many of the best commercial insurance providers will work with you on custom coverage and quotes to ensure your business is adequately protected.

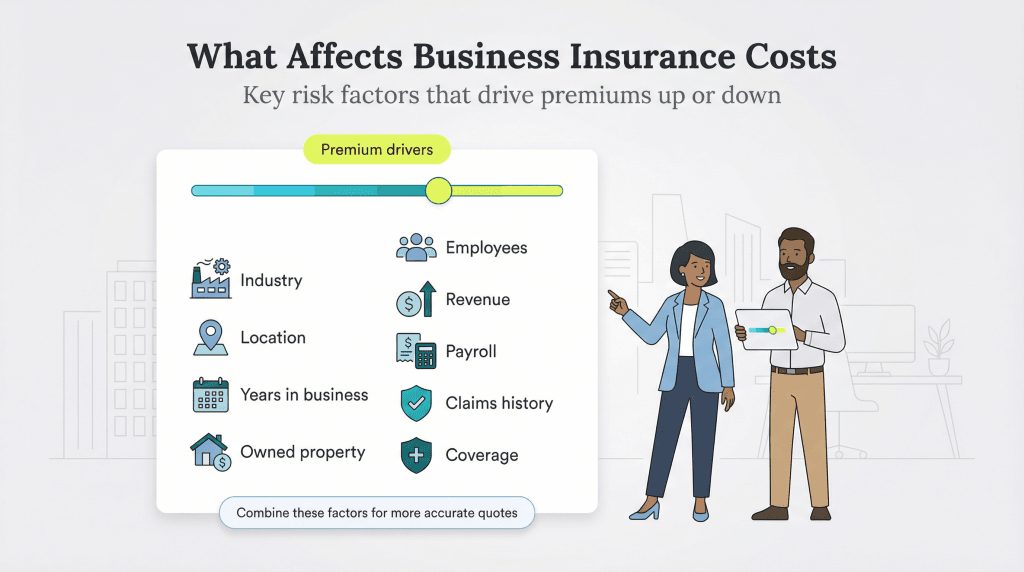

While insurance type affects the price, many other factors will cause your premiums to go up or down. Every business is unique, which means you likely won’t see two businesses with the same insurance premium unless they qualify for the same base or minimum premium.

Consider these factors when you get quotes for small business insurance.

Insurance carriers will want to know what you do so they can classify your company correctly for the insurance you’re purchasing. Keep in mind that specific industries have higher business insurance risk factors for some policy types. For example, a doctor’s professional liability policy costs more than a tutor’s because a doctor’s mistake can cost someone their life while a tutor’s error might only lead to someone failing a test.

Where your business operates will affect your insurance rates. Insurance is regulated at the state level and insurance carriers price policies based on the claims history of a business’s operational area. “Your location plays a significant role in determining risk factors, such as crime rates, exposure to natural disasters and the local legal environment,” Peterie explained. The insurance company may also break down costs by ZIP code, using city and county claims data to determine how risky it is to run a business in that location.

Insurance companies gain confidence in businesses that have been operating for years. The longer you’ve been operating, the more likely you are to conduct business safely and responsibly. For new companies, the management team’s experience can also affect the costs; rates are lower for managers knowledgeable in the industry.

Your business assets will determine how much commercial property insurance coverage you need. These assets include inventory, supplies, materials and business equipment. Businesses don’t often think about how much it would cost to replace all their office furniture and equipment, but that’s precisely what would be necessary after a total loss. Business insurance must consider your business property.

The more employees a business has, the more exposure it has to risk. This is especially true for workers’ compensation claims. The more employees on the payroll, the higher the probability that someone will get hurt on the job.

Revenue is another risk indicator. The idea is that the more you earn, the more exposure you have to the public. This higher exposure increases your chances of a claim. The higher your revenue, the more you become a target for claims in which third parties seek big paydays from deep-pocketed companies.

Payroll is used to calculate your workers’ compensation premium. The workers’ compensation equation multiplies every $100 of payroll by the job classification and your company’s claims history. As the amount of your small business payroll increases, so does the premium.

All insurance policies will consider a company’s claims history. The more claims you have, the higher your premium because you’re considered a higher risk than a company with no claims. Insurance companies see claims as a trend — and a business with claims isn’t trending in the right direction. In contrast, companies may receive a discount if they’ve gone several years without a claim.

If you select more coverage, you’ll pay more in premiums. However, it’s important to point out that double coverage for something like a general liability policy won’t cost twice as much, although it will be more expensive. Get quotes that adequately cover your financial risk to determine if the cost falls within your budget.

Here are some tips for lowering your business insurance rates:

Peterie emphasized the importance of working with the right insurer to save money. “Partner with an agency that specializes in enterprise risk management, including contract management, loss control solutions and claims management services,” Peterie advised.