Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Learn the steps employees must take to receive insurance benefits after a work-related illness or injury.

Nearly all businesses with employees are required to have workers’ compensation insurance. Workers’ comp covers medical expenses and lost wages when employees are injured on the job or develop a work-related illness. According to Liberty Mutual’s 2024 Workplace Safety Index, United States businesses spend over $1 billion each week to cover workplace injury costs — totaling more than $58 billion annually. Without workers’ compensation insurance, businesses must cover these expenses out of pocket, often risking financial devastation.

Editor‘s note: Looking for the right workers’ compensation insurance for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

Given the high cost of medical care for work-related incidents, business owners and human resources teams should familiarize themselves — and their employees — with the workers’ compensation claim process. Doing so simplifies the process while reinforcing their commitment to employee well-being.

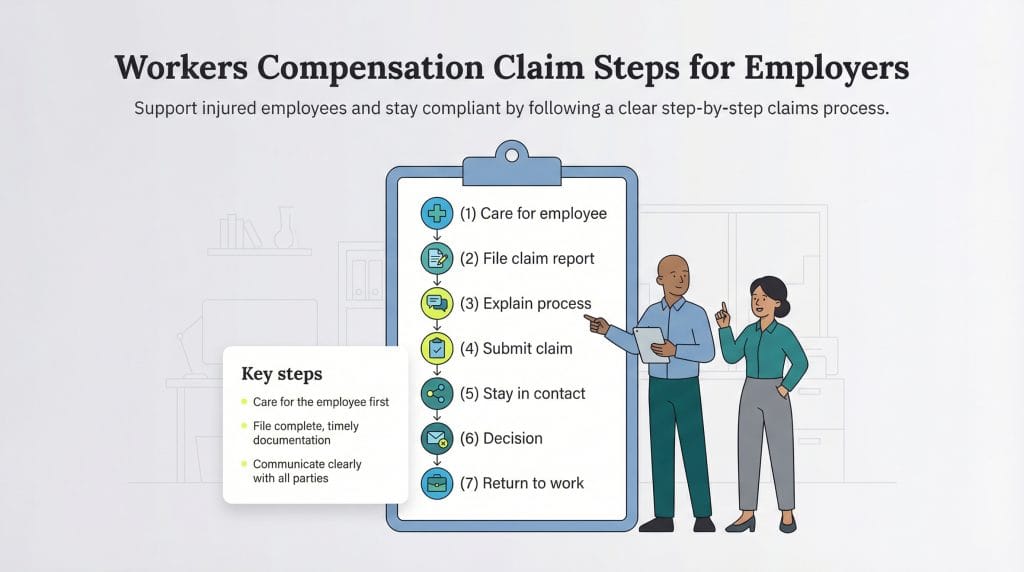

The workers’ compensation claim process is a series of steps employees must take to receive insurance benefits after a work-related illness or injury. It involves reporting incidents to the appropriate person, often an internal HR department member, who will work closely with the employee to complete their claim.

Typically, employers are involved closely in the workers’ compensation claim process to ensure that their HR team or outsourced HR provider processes claims correctly and maintains regular communication with the filing employee and the business insurance provider. Employers should also be actively involved in planning the employee’s return to work after recovery.

Dennis Shirshikov, adjunct professor of economics at City College of New York, emphasized the importance of a simple, easy-to-follow workers’ compensation claims process. “Have a clear reporting system, rapid medical access and a direct line of contact with the insurer,” Shirshikov advised.

Adhering to the workers’ compensation claim process will help you comply with your state’s requirements and provide appropriate support to your employees. While your state may have specific provisions, the following steps generally will apply.

Injured or ill employees are often unable to file claims immediately after an incident. Instead, the primary focus should be on caring for the employee.

Your HR staff — if present at or near the site of an injury — should administer first aid. If necessary, your HR team should arrange for medical care by sending the employee to a doctor or hospital and contacting the employee’s emergency contact. “Many employers may approve rapid medical care before the legal paperwork is completed,” Shirshikov noted.

After the employee’s immediate needs are met, they should file a written report within 24 to 48 hours of the incident. At that point, you’ll file a formal claim with your business insurance provider.

To begin filing the insurance claim, you and the employee should meet with your HR team. During this meeting, all parties should discuss who will complete the required injury or illness report. Sometimes, the employee will complete it alone; other times, you’ll handle it with their assistance. Your HR team can answer questions as needed.

Key information that typically must be provided includes the following:

Depending on your state, you may also need to file state workers’ comp board forms.

Chris Peterie, CEO and co-founder of Tower Street Insurance, emphasized the importance of clear communication with the affected employee. “Clear communication is key,” Peterie advised. “Educate employees about the process, provide accessible forms and designate a point person to guide them through the steps.”

Before filing a claim, walk the employee through the workers’ comp process so they know what to expect. Ensure you cover the following points:

With the previous steps complete, you can now file a formal workers’ comp claim with your insurance provider. Even if your employee completes the claims paperwork on their own, you and your HR team should file the claim on the employee’s behalf.

Before filing the claim, ask your insurance provider how it prefers to receive claims. Electronic submission works for some, while others prefer postal mail or telephone claims. You should ask your provider whether you must also file the claim with your state’s workers’ comp body. In some cases, your provider will handle this step for you.

“Ensuring claims approval requires accuracy, promptness and thorough documentation,” Peterie noted. “Open communication with your insurance provider is essential, as it thoroughly investigates and documents the incident to prevent disputes or delays.”

Once your claim is filed, maintain regular contact with your insurance provider and your employee. This way, you can complete or forward any additional documents.

Your HR staff should also update your employee on the status of their claim regularly and remind the employee when they should expect to hear from the insurance provider about medical concerns and wage replacement.

While the above steps are essential, they don’t guarantee claim approval. Ultimately,

your insurance provider decides whether to approve the claim based on whether the information provided fits your plan’s terms.

If your provider approves your claim, your employee has two options. They can either accept the benefits offered, which typically include coverage for medical costs and lost wages or negotiate for more money. Similarly, in the case of a denied claim, the employee can demand a review or approval.

After your employee has tended to the injury or illness covered in their claim, they should return to work. Before doing so, they should notify you and your insurance provider of their intended return date.

As your employee prepares to return to work, you should develop a customized program to facilitate their return. In doing so, consider the employee’s doctor-ordered medical restrictions on work duties and how these restrictions might affect their performance.

If necessary, create a temporary position for the employee until they can work at full capacity. Alternatively, if you have a current job opening that fits the employee’s restrictions better, you can assign them to this role until they are ready to return to their former position.

In some cases, your employee will be unable to return to work for an extended period, potentially meaning wage losses greater than their workers’ comp payout can cover. If so, you can try to extend the employee’s leave through FMLA, the Americans with Disabilities Act or company policy provisions.

The best time to begin thinking about workers’ compensation is before an injury or illness occurs. It’s crucial to educate your team on workers’ compensation, what it entails and how to file claims.

Consider implementing the following measures:

Kimberlee Leonard contributed to this article.