Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Learn how excess liability insurance works, what it covers, how it differs from umbrella policies and how to tell if your business needs it.

A business’s general liability coverage isn’t always enough to absorb a major claim. When policy limits under your business insurance coverage are exhausted, excess liability insurance can provide another layer of protection. This guide explains how excess liability insurance works, what it covers, how it compares to umbrella insurance and how to decide whether it’s the right fit for your business.

Excess liability insurance is additional business insurance that raises the coverage limits on an existing liability policy after that policy has been maxed out. In other words, it gives your business another layer of financial protection when a major claim exceeds the limits of your primary coverage.

It’s most commonly added to a general liability insurance policy, but it can also increase coverage under commercial auto liability policies and certain other business insurance policies. Think of excess insurance as a “second-in-line” policy: It doesn’t come into play until the underlying liability policy has paid up to its maximum limit.

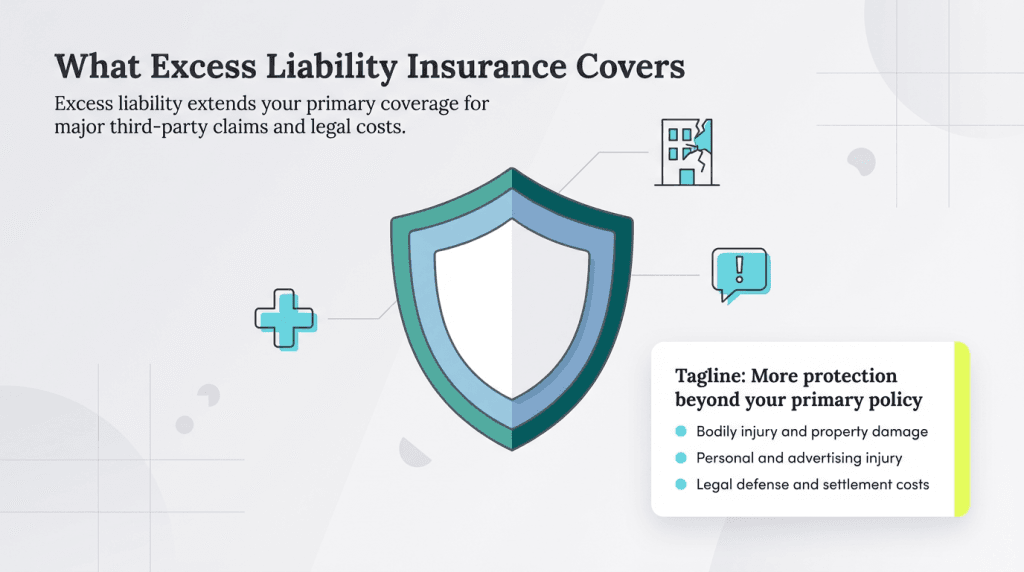

Excess liability insurance usually covers the same claims as the underlying policy, and those claims will vary depending on the policy type. For example, the excess liability policy for general liability will cover slip-and-fall accidents, while the excess liability policy for commercial auto insurance will cover at-fault accidents, third-party injuries or property damage.

The following are commonly covered by excess liability insurance:

Understanding the excess insurance meaning becomes especially important as verdicts and settlements grow larger. According to WTW’s casualty market analysis, third-party litigation funding is expected to reach $31 billion annually by 2028, fueling larger verdicts and settlements that can quickly exhaust primary liability limits.

Excess liability doesn’t typically cover the following:

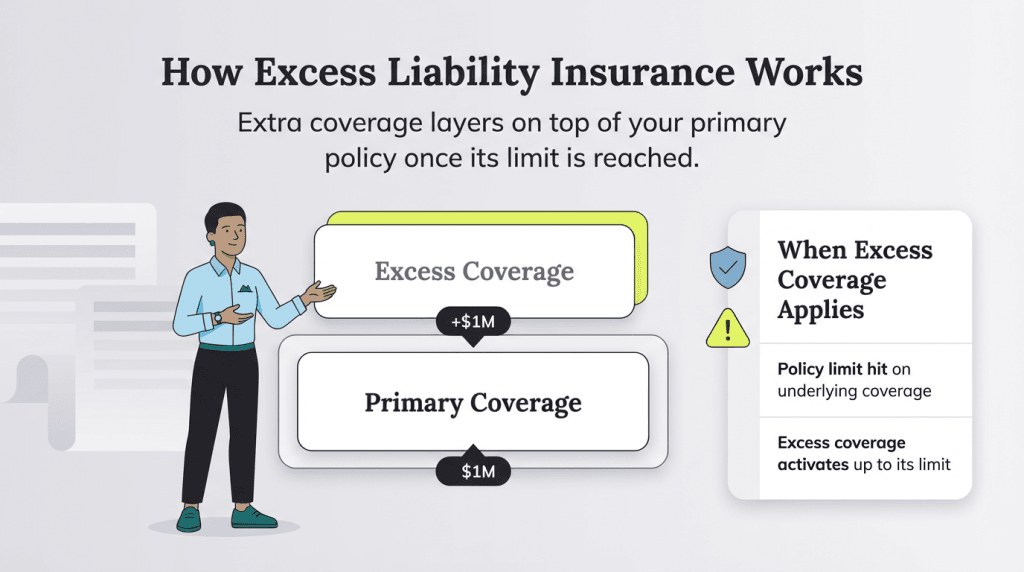

An excess liability insurance policy sits in the background until the underlying policy’s limits have been exhausted. The excess liability insurance policy will kick in once the underlying policy hits its coverage limits. Once in play, it will pay up to its policy limits.

To understand excess insurance in practice, consider this scenario: You have a general liability insurance policy with a per-occurrence limit of $1 million, plus an excess liability insurance policy providing another $1 million in coverage. Together, you have a total of $2 million in general liability protection.

If a customer who falls at your location ends up with a serious injury and sues you for $1.5 million, the general liability insurance policy would cover the first million; the excess insurance policy would handle the remaining $500,000.

However, if the customer’s claim totaled $3 million, the general liability policy would cover the first million, and the excess liability policy would cover the second million. Your business would still be responsible for the remaining million.

Consider your company’s business insurance risks and coverage needs when deciding whether to opt for excess liability insurance. Understanding what excess insurance means for your specific situation is key — it exists to protect you in those rare but financially devastating scenarios where your general liability policy simply isn’t enough.

Ask yourself the following questions about your company’s coverage:

The bigger your business — and the more interaction it has with consumers — the more likely it is that you’ll need an excess insurance policy. Businesses with increased risk, including those that use heavy machinery and equipment, have more exposure and should carry larger liability limits.

Excess liability insurance costs vary widely because policy prices depend on several factors. While rates differ by business type, size and risk profile, the premium you pay ultimately reflects how much exposure an insurer believes your business carries. Some of the biggest pricing factors include the following:

When evaluating excess liability coverage, consider the following:

Commercial umbrella insurance policies and excess liability insurance policies both add liability coverage to specific policies, but there’s a key difference. An umbrella policy usually provides coverage for more than one underlying policy. An excess liability policy is meant to extend only one underlying policy, usually general liability, but it may also cover commercial auto.

Feature | Excess Liability | Umbrella Insurance |

|---|---|---|

Coverage scope | Single underlying policy | Multiple underlying policies |

Policy breadth | Follows form of underlying policy | May provide broader coverage |

Cost | Often costs less for comparable limits | May cost more but can provide broader protection |

Flexibility | Limited to one policy type | Covers various liability exposures |

Claims handling | Often simpler when tied to one underlying policy | May involve broader claims coordination |

Coverage gaps | Typically follows the underlying policy’s terms | May provide broader gap protection, depending on the policy |

Minimum underlying limits | Varies by carrier | Typically requires higher underlying limits |

Generally speaking, both umbrella and excess liability insurance policies typically maintain the underlying insurance policies’ terms and conditions, including many of the underlying policy’s exclusions.