Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Gap Insurance for Healthcare? Look for More of It in 2026

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Health insurance is usually the core of any business’s employee benefits package. However, with escalating health insurance costs, many companies are seeking less expensive alternatives, such as high-deductible health plans (HDHPs).

Still, employees with HDHPs may struggle with high deductibles and steep out-of-pocket expenses if they experience a sudden illness or accident. That’s where gap insurance comes in. With gap insurance, employers get a chance to fill the financial gap left by HDHPs and help their staff manage healthcare costs. Here’s everything a business needs to know about offering gap insurance to its employees.

What is gap insurance in healthcare?

Gap insurance, also called supplemental health coverage, is additional group health insurance that’s paired with an HDHP. The gap plan helps cover employees’ out-of-pocket costs, including deductibles, copayments and coinsurance expenses.

A gap insurance plan is part of a company’s employee benefits package. You can structure gap plans in various ways, but they often extend coverage to prescription drug costs and other healthcare-related expenses.

Gap insurance may also help with certain nonmedical costs, such as travel for treatment, lodging during a hospital stay or even some income support if someone has to miss work while recovering. These extras can make a real difference for employees facing a tough health situation.

Combining gap insurance with an HDHP can be a cost-effective alternative to offering a low-deductible plan. The best business insurance providers can help you understand how gap policies fit into your overall benefits strategy.

What is an HDHP?

A high-deductible health plan (HDHP) is a health insurance plan with a minimum deductible of $1,700 for self-only coverage and $3,400 for family coverage in 2026, according to the IRS. Deductibles can be significantly higher in practice, and many plans exceed $5,000 for individuals.

HDHPs remain a popular option for employers and employees. In 2025, 33 percent of covered workers were enrolled in an HDHP with a savings option, according to the Kaiser Family Foundation. Additionally, 36 percent of firms with 10 or more employees that offer health benefits make an HDHP available.

Why would an employer choose an HDHP?

High-deductible health plans can be an attractive option for employers looking to manage insurance expenses while continuing to offer dependable health coverage. HDHPs generally come with lower monthly premiums, which can help companies manage rising benefits expenses. They’ve also been somewhat effective in slowing annual premium increases, making them an appealing option in tight budget years.

However, adopting an HDHP does shift more upfront costs to employees, who must cover higher deductibles, copayments and other out-of-pocket expenses before their plan begins paying for care. This cost shift is one of the main reasons employers pair HDHPs with gap insurance, HSAs or HRAs to help offset employee expenses.

Tip

As a creative perk, consider paying your employees' gap insurance premiums. If that's not financially feasible, you can still offer gap insurance as an optional benefit and let employees choose to enroll and cover the premium themselves.

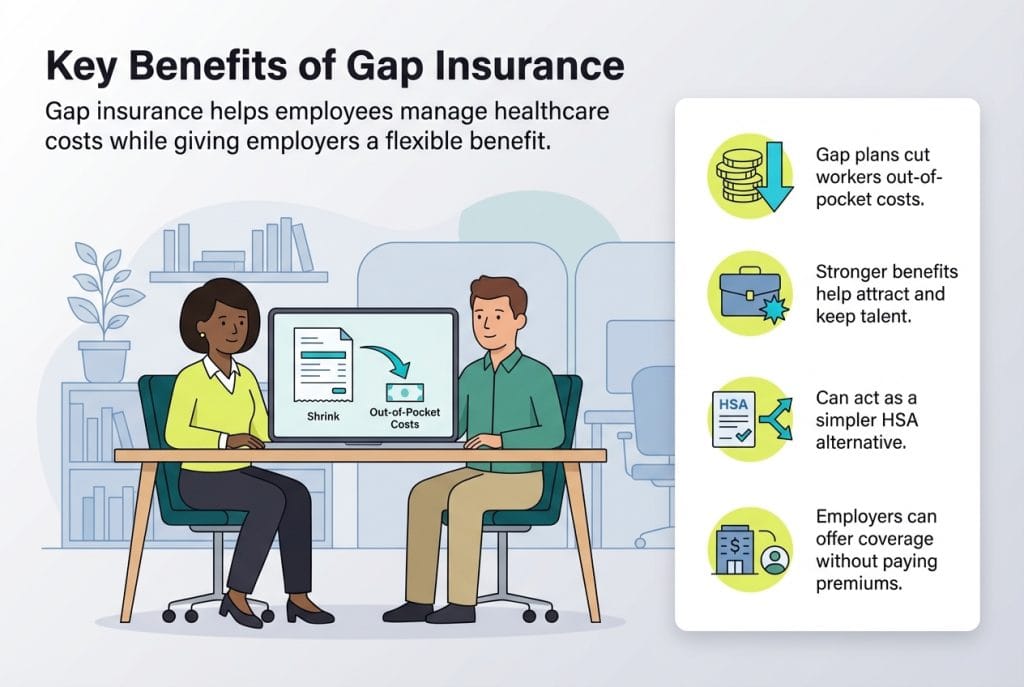

What are the benefits of gap insurance?

Gap insurance offers several meaningful advantages for both employers and employees, including the following:

Gap insurance lowers employees’ out-of-pocket costs. Pairing gap insurance with an HDHP helps ease the financial strain on employees. It reduces what they owe in deductibles, copayments and other healthcare expenses, making their coverage feel more affordable and predictable.

Gap insurance strengthens an employee benefits package. Offering gap insurance — especially alongside other creative perks — can help your business stand out during the hiring process. It signals that your company cares about employees’ financial well-being and can support efforts to attract and retain strong talent.

Gap insurance can serve as an alternative to a health savings account (HSA). Instead of funding an HSA to handle high out-of-pocket costs, employees with gap insurance often face fewer upfront expenses to begin with. For some workers, this structure feels simpler and more manageable.

Gap insurance doesn’t have to be an employer expense. Although employers may choose to cover the premiums, they aren’t required to. Gap insurance can be offered as a voluntary benefit, allowing employees to opt in and pay the premium themselves.

What are the downsides of gap insurance?

While gap insurance can be a valuable tool for many companies, it isn’t the right fit for every business or every workforce. Coverage terms vary widely by carrier, so it’s important to read the fine print to understand exactly what’s included.

Some potential downsides include the following:

Gap insurance doesn’t cover every expense. Some plans exclude certain out-of-pocket costs, such as lab work, diagnostic imaging or mental health services, leaving employees responsible for those bills.

Preexisting conditions may limit coverage. Depending on the policy, employees with preexisting conditions may be denied coverage or face waiting periods before benefits kick in.

Gap insurance may have additional fees. Even with a gap plan, employees may still pay deductibles, copayments or other fees tied to their specific policy.

Gap insurance typically has benefit limits. Most gap plans cap how much they’ll pay per illness, injury or policy year. Employees who exceed those limits could still face significant expenses.

Did You Know?

Gap insurance also exists in the commercial auto insurance world. It covers the difference between a vehicle's depreciated value and the remaining loan balance if the car is totaled.

How does gap insurance compare to an HSA?

HSAs and gap insurance offer similar advantages; both are designed to help reduce employees’ out-of-pocket medical costs. However, employees cannot contribute to an HSA and enroll in a gap plan at the same time (even though an employer can technically offer both options). Here’s how the two compare:

HSA costs: For 2026, the IRS increased Health Savings Account contribution limits to $4,400 for self-only coverage and $8,750 for family coverage, with an additional $1,000 catch-up contribution for individuals ages 55 and older. These accounts grow tax-free, roll over each year and stay with the employee. Although employers can put money into an HSA, most don’t, so employees usually have to contribute on their own to build a meaningful balance.

Gap insurance costs: Gap medical insurance policies typically cost between $30 and $75 per month, depending on the plan’s benefit levels and employee demographics. Some employers choose to cover these premiums, but even when employees pay the cost themselves, gap insurance is generally considered an affordable supplemental benefit.

HSA coverage: HSAs offer broad flexibility. Funds can be used for a wide range of qualified medical expenses, from deductibles and copayments to dental and vision care. Balances roll over year to year and can even function as a long-term savings tool for medical expenses in retirement.

Gap insurance coverage: Gap insurance is designed to cover specific gaps in HDHPs, primarily helping with deductibles, copayments, coinsurance and out-of-pocket maximums. Coverage varies by policy, so employers should review benefit limits and exclusions closely.

HSA vs. gap insurance: Side-by-side comparison

Feature

HSA

Gap insurance

Primary purpose

Helps employees save pre-tax dollars for qualified medical expenses

Helps pay high out-of-pocket costs from an HDHP (deductibles, coinsurance, OOP max)

2026 costs

Employees can contribute up to $4,400 (self-only) or $8,750 (family); optional $1,000 catch-up for age 55+

Typically $30-$75 per month ($360-$900 annually), depending on plan and demographics

Who pays?

Usually funded by the employee (employer contributions are optional but uncommon)

Employer can pay premiums, or employees can opt in and self-pay

Coverage flexibility

Broad: Can be used for many qualified medical expenses

Narrower: Designed to cover gaps in HDHPs (deductibles, coinsurance, certain OOP costs)

Rollover feature

Funds roll over year to year and are employee-owned

Benefits do not roll over; structured as annual insurance coverage

Best for

Employees who want long-term savings, tax advantages and control over spending

Employees who want help with large, immediate out-of-pocket expenses under an HDHP

Compatibility

HSA contributions cannot be made if the employee has a gap insurance plan

Gap insurance makes an employee ineligible to contribute to an HSA

Tip

Get anonymous employee feedback to determine whether your team prefers a gap insurance policy or an HSA. This could provide vital insights into employees' needs.

Should employers provide gap insurance?

Whether gap insurance is right for your business depends on your workforce’s needs and your overall benefits budget. If you already offer an HDHP, you’re likely saving money on premiums. As long as adding a gap plan doesn’t outweigh those savings, it can be a smart way to boost coverage and support employees who might otherwise struggle with high out-of-pocket costs.

Consider the following questions to decide if gap insurance makes sense for your company:

Do you offer an HDHP? If so, gap insurance can help employees cover deductibles and out-of-pocket expenses, making their healthcare costs more manageable.

Are you concerned about employees facing significant medical bills? Gap insurance can provide meaningful financial relief and may encourage employees to seek necessary care without delaying treatment due to cost.

Do you have employees with high-risk or chronic health conditions? These workers may benefit most from the extra protection a gap plan provides, especially when an HDHP leaves large coverage gaps.

Are you focused on attracting and retaining top talent? Offering gap insurance can strengthen your overall benefits package and demonstrate that your company values employee well-being.

Is giving employees peace of mind a priority? Gap insurance can ease financial uncertainty and show your team that you’re invested in their health and security.

Have you decided against offering HSAs? If administering an HSA program feels too complex — or your employees aren’t engaging with it — gap insurance is a simpler alternative that still helps offset out-of-pocket costs.

Can you afford gap insurance? If the premiums fit within your benefits budget without reducing other offerings, it’s likely worth providing. You can also offer gap insurance as a voluntary benefit and allow employees to pay the premiums themselves.

Keep in mind that gap insurance policies vary widely. Both employers and employees should review the details closely to understand exactly what’s covered. Some plans exclude specific tests, procedures or preexisting conditions, so it’s important to set clear expectations upfront.

Did You Know?

The best HR software can streamline employee benefits administration, making it easier to manage gap insurance alongside payroll and recruitment tools.

Gap insurance can be part of an attractive benefits package

For some companies, pairing an HDHP with gap insurance can be a financial lifeline. For others, it’s simply a smarter way to control healthcare costs while still offering a competitive, well-rounded benefits package.

When employers spend less on premiums for a traditional low-deductible plan, those savings can be redirected toward a richer mix of benefits, such as dental and vision coverage, corporate wellness programs or other high-value perks. This approach allows businesses to create a more flexible and appealing benefits package without absorbing the significantly higher premiums associated with lower-deductible health plans.

In this way, gap insurance helps make HDHPs more feasible, and in many cases, even more desirable, for both employers and employees.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.