Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is Claims-Made vs. Occurrence?

When choosing business insurance, business owners should understand claims-made vs. occurrence policies as each offers certain advantages and features.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Purchasing business insurance can protect your company from damages should an incident occur. When choosing business insurance, you can buy one of two types of coverage: claims-made or occurrence. While both protect against the same perils, it varies when coverage is triggered.

Here’s everything you need to know about claims-made vs. occurrence coverage, including how to determine which policy is best for your business.

What’s the difference between a claims-made and an occurrence policy?

A claims-made policy protects a business owner from incidents that occur and are reported during the policy’s term. An occurrence policy provides coverage during a specific term but will allow you to report claims after the policy term.

The key differences between claims-made and occurrence policies are as follows:

Claims-made policy

Occurrence policy

Coverage

Covers any claims made during the policy period, regardless of the date of the incident

Covers any incidents that occurred during the policy period, regardless of the date the claim is made

Reporting period

During the policy period (or extended reporting period if purchased)

Any time, as long as the incident occurred during the policy period

Tail coverage

Can be purchased to extend the reporting period if policy coverage ends

Not required/applicable

Costs of premiums

Often lower initially, but may increase over time

Often higher initially, but stable over time

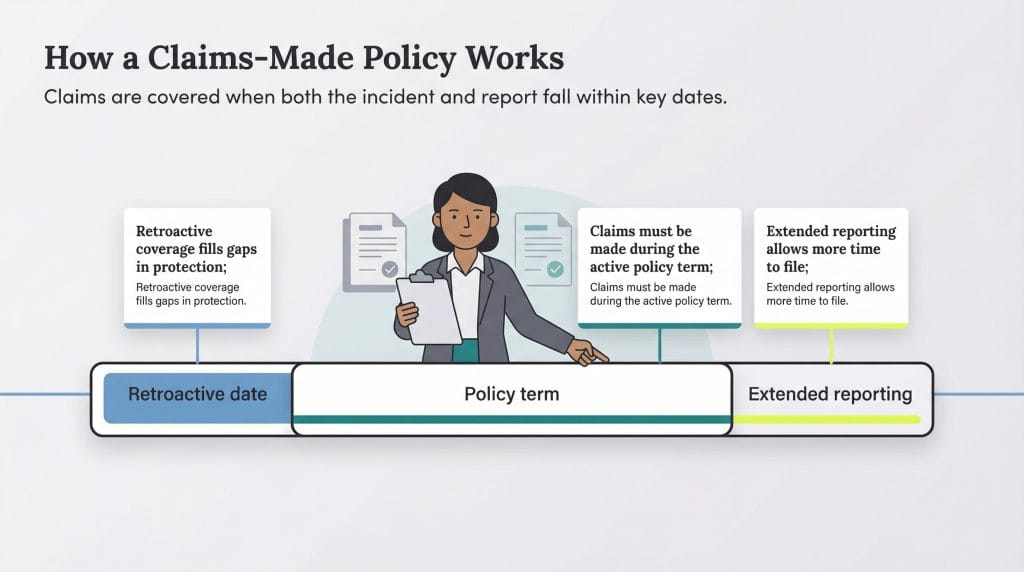

What is a claims-made policy?

Claims-made policies let you customize a coverage period. You’re protected from incidents during the policy’s term and during any added periods. Business owners can extend protection by electing retroactive coverage to a date before the policy was activated. They can also ask for an extended reporting period for more flexibility when filing a claim.

Retroactive coverage is determined by the retroactive date. This is when the policy’s coverage begins, and coverage is in effect after this date. A retroactive date provides critical coverage for a business with an insurance gap, offering protection for a time when the business didn’t have a policy in place.

In a claims-made policy, claims must be made during the policy term to be covered. For this reason, business owners may feel restricted at the end of a policy’s term. This is why opting for an extended reporting period is helpful. It permits the filing of a claim after the policy is canceled. While this isn’t extended coverage, it allows delayed reporting up to a specific date.

What’s an example of a retroactive date?

Let’s say a small business owner purchases general liability insurance, which is a claims-made policy. The policy’s effective dates are Jan. 1, 2023, to Dec. 31, 2023. Because the business owner accidentally allowed their previous policy to lapse, they elect to implement a retroactive date of Oct. 1, 2022.

On March 1, 2023, the business owner files a claim about an incident that occurred on Dec. 5, 2022. Because the incident happened after the retroactive date, this is a covered claim. If the incident had occurred on Sept. 20, 2022, the insurer wouldn’t cover it.

Example of an extended reporting period

Let’s say a business owner purchased a claims-made business owner’s policy (BOP) on Feb. 1, 2022, with a policy term ending Jan. 31, 2023. The company elects to add an extended reporting period of six months for a slightly higher premium.

On April 1, 2023, the company receives a claim for an incident that happened on Dec. 10, 2022. Because the incident happened during the policy’s term and was reported within the extended reporting period, it’s covered. It would not be covered if it were reported after July 31, 2023, because that date is past the extended reporting period.

Occurrence policies are generally more expensive than claims-made policies because they let you report a claim at any time, unlike a claims-made policy, which specifies when you can report a claim. The occurrence policy allows for claim rights that extend well beyond the policy term as long as the coverage was in effect during the time the loss occurred.

This means a business owner with an occurrence policy doesn’t have to elect an extended reporting period; the policy automatically includes extended reporting. However, occurrence policies won’t allow you to put a retroactive period in place to get coverage for a time before the policy term.

What’s an example of an occurrence policy?

Let’s say a business owner purchases professional liability insurance that is set as an occurrence policy. The policy is purchased with a term of Jan. 1, 2020, to Dec. 31, 2020. The business owner retires after Dec. 31, 2020.

On Oct. 21, 2023, the retired business owner receives notice of a claim filed for an incident that happened on Aug. 12, 2020. Since the policy was in force at the time of the incident, the claim will be processed even though it wasn’t filed until years after the incident occurred.

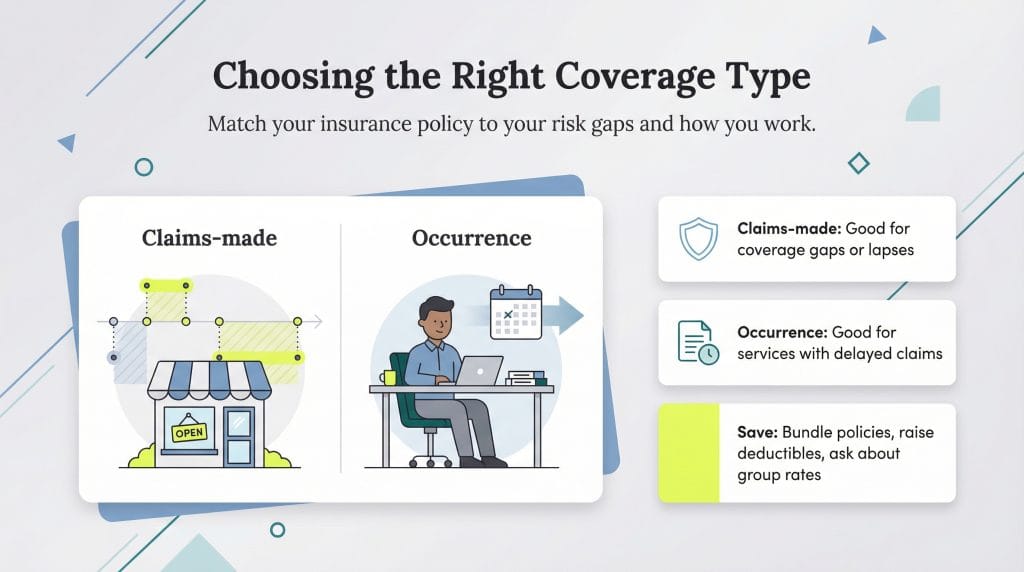

Which is the right type of coverage for you?

It can be challenging for business owners to know which type of business insurance coverage they need. As a general rule of thumb, if a business has coverage gaps, a claims-made policy is better. A claims-made policy affords coverage for incidents that might have happened while it didn’t have a policy in place.

Often, this situation affects new businesses, where insurance might not have been an immediate priority. Still, claims-made coverage is also useful for a business with an accidental coverage lapse.

Occurrence policies are a good option for professional service providers who may do the work in one period but have a claim filed much later. For example, if a tax preparer’s professional liability policy ended on April 30, 2023, and the client is audited four years later, the professional liability policy that was in place would offer coverage for any errors made.

Did You Know?

You can save money on business insurance by bundling policies into a single BOP, increasing your deductible and asking about group rates.

Claims-made vs. occurrence FAQs

For more information on claims-made and occurrence policies, read on for answers to frequently asked questions.

It’s possible to change your policy type. This could happen when you change insurance carriers or as part of a renewal review when your policy is approaching expiration.

When switching from a claims-made to an occurrence policy, note that you may be creating a coverage gap. This gap can occur because you can’t make a claim on the new policy for a loss that occurred during the claims-made policy period.

For example, say a small business has a claims-made policy in effect with no “tail coverage” from Jan. 1, 2023, to Dec. 31, 2023. On Jan. 1, 2024, it changes the policy to an occurrence policy. A claim is made on Jan. 15, 2024, for a slip-and-fall injury that happened on Dec. 27, 2023.

While the business had coverage for the incident when the policy was in force, it no longer has coverage because there is no tail coverage extending when the claim can be reported. The new policy won’t cover the claim from a previous policy term. This means you may be liable for the loss and have to pay out of pocket.

It’s important to review the risks of changing coverage forms when renewing or getting a new insurance policy. You must be certain you have adequate coverage for anything that might come up as a claim. Plus, claims are not always filed in a timely manner. The best business insurance carriers will work with you to ensure you’re not leaving your company vulnerable.

Tail coverage is another way to refer to the extended reporting period of a claims-made policy. Tail coverage is an added endorsement to a policy that allows you to report and file claims that happened during the policy’s effective period.

Tail coverage is different from an occurrence policy, where reporting can happen at any time after the policy’s termination. Tail coverage is optional and an added cost.

The exact number will depend on your policy’s aggregate limit, which refers to the level of coverage you have for any future incidents.

For a claims-made policy, your aggregate limit covers the duration of the policy. If you have a $1 million claims-made policy for your business and are sued for $1 million in your first year, you would have no remaining protection on that policy. You would need to increase your policy limit the next year to gain any additional coverage.

For an occurrence policy, your aggregate limit resets annually. If you have a $1 million occurrence-based policy for your business and are sued for $1 million in your first year, your coverage would be exhausted for that year. However, since your aggregate limit resets when your policy renews, you would be covered for an additional $1 million in occurrences for the following year.

Claims-made policies with tail coverage typically cost less than occurrence policies — at least 35 percent less at the outset, according to The Trust — because occurrence policies reset aggregate limits annually and have longer coverage periods. However, claims-made policies typically increase each year due to the increased risk of someone filing a retroactive claim.

Kimberlee Leonard contributed to the reporting and writing in this article.

Sean Peek co-founded and self-funded a small business that's grown to include more than a dozen dedicated team members. Over the years, he's become adept at navigating the intricacies of bootstrapping a new business, overseeing day-to-day operations, utilizing process automation to increase efficiencies and cut costs, and leading a small workforce. This journey has afforded him a profound understanding of the B2B landscape and the critical challenges business owners face as they start and grow their enterprises today.

At business.com, Peek covers technology solutions like document management, POS systems and email marketing services, along with topics like management theories and company culture.

In addition to running his own business, Peek shares his firsthand experiences and vast knowledge to support fellow entrepreneurs, offering guidance on everything from business software to marketing strategies to HR management. In fact, his expertise has been featured in Entrepreneur, Inc. and Forbes and with the U.S. Chamber of Commerce.