Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is Tail Insurance in Business?

You can't predict when a business insurance claim will arise. Tail coverage offers essential protection for incidents that occur during a coverage period.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

No one can predict the future. A customer may make a claim against your business with no warning, which can come at the wrong time if you’re in between insurance policies, getting ready to retire or closing down your business. In instances when your policy has ended, tail coverage can offer the protection you need if the policy was active during the claim incident. In this article, you’ll learn how tail insurance works and whether or not your business should invest in it.

What is tail coverage in insurance?

In business insurance, a policy can either be a claims-made policy or an occurrence policy. While occurrence-based policies automatically include coverage for a claim that occurs during the policy period — regardless of when it was filed — claims-made policies only cover a loss if both the incident and the claim occur while the policy is active. Enter tail insurance ― also called an extended reporting period ― which extends coverage on an insurance policy for an incident that occurs during the coverage period but gets reported after the policy expires or is canceled.

Since tail insurance is an endorsement, “typically there is a charge to add this,” advised Neokissha Penix, a commercial underwriting auditor. Tail coverage is found on commercial liability insurance policies that are claims-made policies.

Keep in mind that tail coverage differs from retroactive coverage, which covers incidents that occur before the policy’s inception date. Retroactive dates extend coverage while tail coverage extends the reporting period. [Related article: What Is an Insurance Rider?]

FYI

Tail coverage isn't necessary on occurrence-based policies because the reporting period for filing an insurance claim is indefinite with them.

How does tail insurance work?

Tail coverage gives you peace of mind that coverage for an incident exists after your policy is canceled or lapses. It is an important consideration when you anticipate coverage changes. Tail coverage is typical when a business closes, a service provider retires or a company moves to a new occurrence-based policy.

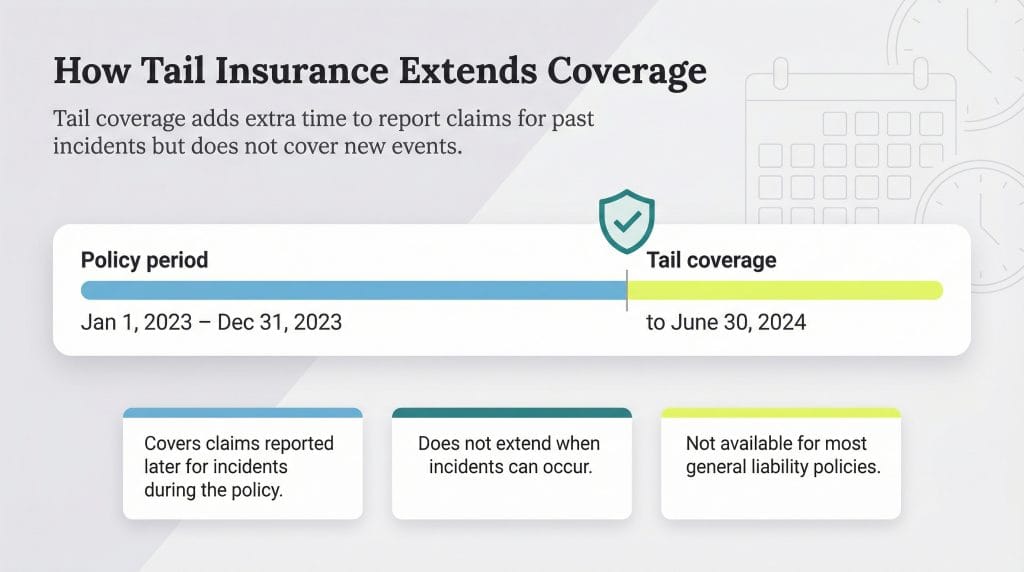

Tail coverage is straightforward: it adds a reporting period to the end of your policy term. For example, assume your policy has a term date of Jan. 1, 2023, to Dec. 31, 2023, and you request to add tail coverage to this claims-made policy for six months. This coverage means that a claim can be made through June 30, 2024, for an incident during the policy term in 2023.

Importantly, tail coverage doesn’t extend the policy period. In the above example, tail insurance won’t cover an incident that happens after Dec. 31, 2023. If an incident does occur after Dec. 31, 2023, and someone files a claim against your business, the claim will be denied and you will be responsible for any losses or damages from that claim.

Did You Know?

A general liability policy usually isn't a claims-made policy, so you can't add an extended reporting period or tail coverage.

Who should consider tail coverage?

Tail coverage should be obtained if you plan to retire or close your business in the foreseeable future. It’s also essential to get this endorsement if you’re switching to an occurrence-made policy.

Example 1: Business closure

An accountant is about to retire and has had a claims-made insurance policy from Jan. 1, 2003, to Dec. 31, 2023. The accountant retires and closes their practice as of Dec. 31, 2023; there will be no new potential exposure for a claim from that date. However, the accountant can still be sued for work they did in 2018 if the claim is filed in early 2024.

Without tail coverage, the accountant would be responsible for all legal and defense fees as well as any settlement or judgment resulting from the lawsuit. With tail coverage, provided the loss is reported within the extended reporting period, the policy limits will kick in and pay for the claim’s defense while handling the settlement costs up to the policy limits.

Example 2: Switching to an occurrence-made policy

When moving to an occurrence-made policy, remember that these policies pay only for incidents that happen during the policy period, even though the claim can be reported anytime thereafter. So, if your business moves from a claims-made policy that ends on Dec. 31, 2023, to an occurrence-made policy, there could be a coverage gap.

Imagine that an incident that occurred in December 2023 wasn’t reported until February 2024. The claims-made policy without tail coverage would not cover the incident because it wasn’t reported in the allowable period. The occurrence-made policy wouldn’t cover it because the incident happened before coverage for the new policy started.

Tip

Ask your business insurance broker if you should consider adding tail coverage ― but be sure to do this before your policy's term end date.

How long should tail coverage last?

There may be coverage gaps if your tail coverage doesn’t extend for a long enough period. For example, assume that the tail coverage on your policy ending Dec. 21, 2023, was for six months. In this case, claims reporting could happen through June 30, 2024. However, if the insurance claims process began in July 2024, your company wouldn’t have coverage because the coverage period is over.

To avoid coverage gaps, talk to your insurance representative and legal counsel. Determine the statute of limitations in your state for filing claims. Ensure you have tail coverage that lasts as long as the statute of limitations so you don’t find yourself past the reporting date and uncovered. [If you’re looking for a new insurance representative, check out our picks for the best business insurance providers]

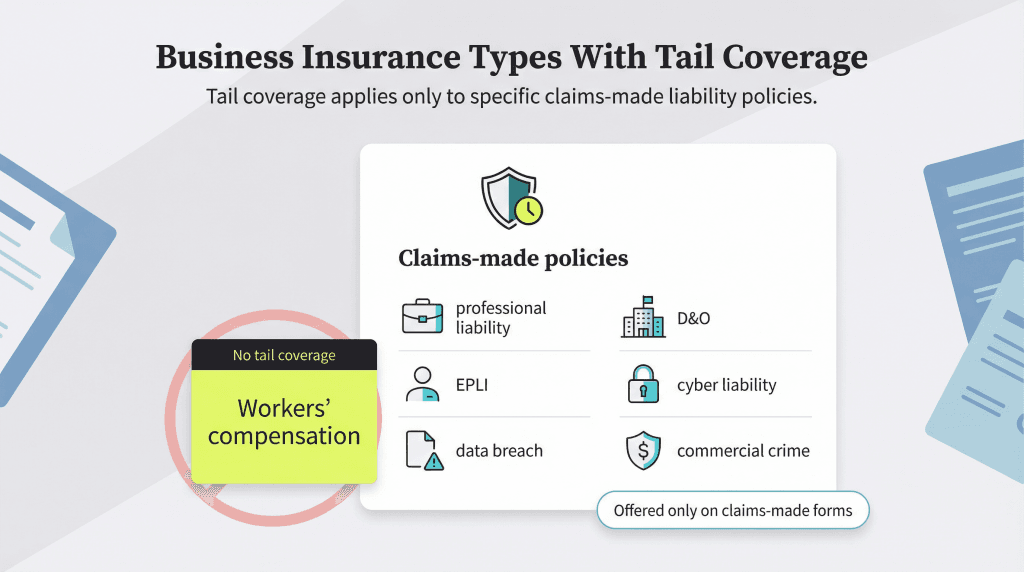

What insurance types offer tail coverage?

You can get coverage on certain types of liability policies. Again, tail coverage is offered in claims-made insurance policies but not on occurrence-made policies.

These are the most common types of business insurance policies in which you can acquire tail coverage:

One policy that you won’t need tail insurance for is workers’ compensation. It is typically an occurrence-made policy. However, it has its own unique challenges. Read more about workers’ comp insurance and how much you need.

Tail coverage FAQs

Tail coverage is part of a claims-made policy. However, not every claims-made policy has tail coverage. This optional coverage is usually added by endorsement to the policy. You'll have to ask for tail coverage, set the coverage length and pay the appropriate premium.

The cost of tail coverage will depend on your insurance type and the length of the tail coverage. One example is tail coverage added to medical malpractice insurance, which costs approximately 200 percent of the expiring premium. So, a claims-made policy with a premium of $7,500 would require another $15,000 to obtain tail coverage. Tail coverage is typically added before the policy expires or is canceled. You can add tail coverage when you receive your renewal bill or the cancelation notice. This may be two months before coverage termination. If you don't elect tail coverage before the policy's cancelation, you may have up to 60 days after the termination to add the coverage. Your insurance carrier will give you details on how to do this.

As an endorsement, it's essential to make the election for tail coverage: It isn't added automatically. Talk to your insurance carrier if you are concerned about obtaining tail coverage. Your representative will give you the details about the company's procedures for adding the endorsement and paying the additional premium.

A claims-made policy can be modified in two ways: It can extend coverage to prior acts with a retroactive date or extend the reporting period after the policy ends with tail coverage. Thus, prior acts coverage isn't the same as tail coverage. There are two different options you can choose from with a claims-made policy. You can have one without the other or you can opt for both.

Policyholders enjoy occurrence-made policies because they know they will be protected regardless of when a claim arises. However, these policies generally are more expensive than claims-made policies. To maximize cost savings, claims-made policies are the better option.

Most policies are occurrence policies. If you have a professional liability, EPLI or D&O policy, you may have a claims-made policy. Because the claims-made policy only covers incidents where the claim is made during the policy period ― or a tail coverage period ― you'll want to ask your insurance carrier how your policy is categorized. If there is tail coverage, ask for how long so you fully understand the terms of your coverage.

Runoff claims are similar to tail coverage. They apply to claims-made policies. A runoff claim states that the insurance carrier remains liable for any claim caused by the policyholder but made after the policy's termination. A runoff period is usually longer ― up to five years ― whereas an extended reporting period or tail coverage often lasts only one year. Additionally, runoff claims are usually found when an insurance merger occurs.

In claims-made insurance, nose coverage ― also referred to as prior acts coverage ― protects you against a mistake you made in a previous policy that has since ended. Sometimes, liabilities transition between policies. In these cases, nose coverage comes into play to protect you, no matter where your policy stands. The new insurer extends your coverage to protect past actions. This type of insurance only covers claims during active periods and excludes events before the policy is in place or after it's been canceled. Nose coverage is different from tail coverage in that it addresses the gap between old and new policies. While tail coverage handles legal fees for past events filed after the policy was canceled, nose coverage manages the interim period under the new policy.

Nathan Weller and Sean Peek contributed to this article.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.