Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Intellectual property insurance is vital for businesses that face the risk of infringement because it guards against costly litigation and protects intellectual assets.

Intellectual property (IP), whether it’s Apple’s proprietary operating system or the recipe for Coca-Cola, is highly valuable — sometimes worth millions of dollars. Using intellectual property without express consent can lead to expensive legal battles for both sides. [Learn how to handle a business lawsuit.]

Intellectual property insurance covers the costs of these lawsuits, so it can be particularly helpful for small businesses that lack the legal and financial resources of larger companies. Here’s everything you need to know about intellectual property insurance.

Editor’s note: Looking for the right liability insurance for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

“Intellectual property insurance is a highly specialized and complex form of coverage designed to protect businesses against claims related to IP infringement,” said Chris Peterie, CEO and co-founder of Tower Street Insurance.

Infringement claims for major corporations can quickly exceed millions of dollars. This is why intellectual property insurance is so important. IP insurance pays for the legal costs in the case of infringement or theft of the property. There are two types of coverage: infringement defense and abatement enforcement.

If you have a general liability insurance policy, you may already have limited coverage if your advertising infringes on another party’s copyright or trademark. This is important coverage for business owners.

“Intellectual property insurance is designed specifically to help cover legal expenses and potential damages if a business is accused of infringing on another party’s intellectual property,” said Dennis Shirshikov, an adjunct professor of economics at the City University of New York. “General liability insurance, on the other hand, typically covers bodily injury, property damage and broader claims often unrelated to intellectual property.”

However, the scope of general liability insurance is limited, and the claim limits are based on the general liability limits. The general liability policy protects a business only for claims resulting from advertising activities. Many businesses are engaged in activities with intellectual property that go beyond the scope of advertising and thus need further protection.

Intellectual property insurance covers you for a wider range, including abatement enforcement, and generally maintains higher limits. It’s a specialized policy for companies that are concerned about the risk of major intellectual property battles. [Read more about professional liability insurance.]

Historically, intellectual property insurance was not a popular coverage option. “Due to its high cost and limited coverage scope, very few businesses purchase intellectual property insurance,” Peterie said. However, intellectual property infringement is becoming more common in the digital age, which is why it’s important to get intellectual property insurance if you are at risk.

Any business that holds patents or trademarks needs intellectual property insurance. A company with patents could be vulnerable to time-consuming and expensive patent litigation. If competitors use your intellectual property — often, a trademark — without consent, it could damage your brand and harm your company’s reputation.

A small business that is at risk of violating intellectual property laws only through advertising will need coverage, but this is often part of a general liability insurance policy. It will not provide coverage to fund legal counsel if you are infringed upon. It covers only defense, so you’ll want additional coverage if that’s a concern.

>> Find a policy that fits your needs with our picks for the best business insurance.

Small businesses should assess their need for intellectual property insurance. Without coverage, a smaller business may not be able to bear the costs of a rights violation. This is especially true of a violation by a larger firm, which may try to litigate your business out of the market as a tactic of dealing with competition.

That means small companies that are heavily reliant on patent work, trademarks and copyrights need to consider acquiring intellectual property coverage. “A small company might invest in IP insurance to safeguard its new designs against alleged duplication of competitors’ patents,” Shirshikov said.

>> Learn more: Business Insurance Guide

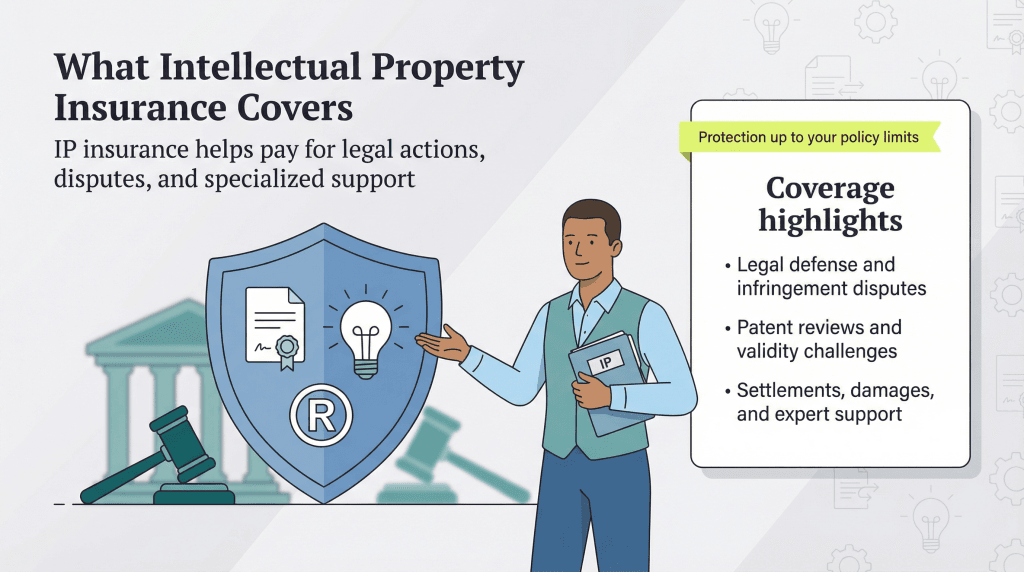

Intellectual property insurance provides financial coverage up to the policy limits. Depending on your policy, the limits may include the legal fees associated with an intellectual property claim.

The intellectual property insurance policy covers the following expenses:

You can schedule coverage for specific products, processes and services to ensure you are protected. Coverage applies both to cases where a competitor is infringing on your intellectual property and to cases brought by so-called trolls, or nonpracticing entities. The coverage includes appeals and counterclaims that you may want to file.

Policies also include coverage in cases where you have contractual indemnity and are indemnified by party defense, which pays for damages or losses sustained by a third party as the result of future occurrences. Your policy will also pay for any needed expert witness testimony, technical analysis and design-arounds needed to prove your case.

Your coverage allows you to choose legal counsel so that you are confident in the legal actions taken. Counsel coverage doesn’t end when the trial is over; you also receive post-incident responses that are written and filed on your behalf to close out the case.

A policy may offer one or both types of intellectual property coverage.

Type | Definition |

|---|---|

Infringement defense | The foundation of all policies, this coverage protects you if you are accused of using another company’s intellectual property without authorization. It pays for the legal defense, settlement or damages to another party for the violation of their patent, copyright or trademark rights. |

Abatement enforcement coverage | Often an add-on, this coverage gives you the resources to legally pursue action against those violating your intellectual property rights. |

The cost of intellectual property insurance varies. The underwriter bases the premium on your industry risk, your revenue and the types of intellectual property you are insuring. For limited coverage through a general liability insurance policy, a small business could expect to pay as little as $500 per year. However, for a specialized policy designed to protect you from specific risk, you could pay tens of thousands of dollars annually.

Intellectual property coverage is considered a specialty insurance policy. This means you may have trouble finding a carrier that offers the coverage and even more difficulty finding competitive rates.

Assess your company’s need for abatement enforcement coverage. Remember that this isn’t always included automatically, so you’ll need to ask for a quote with and without this coverage. Every insurance carrier has its own appetite for certain industries, meaning it is more likely to insure certain types of companies than others. You may have to shop around for an insurance carrier that meets your company’s needs.

Even with insurance, your best course of action is to prevent a loss in the first place. To mitigate intellectual property risk, develop company protocols that protect your property through the course of business. For example, follow these best practices:

By taking measures to protect your intellectual property, you can reduce claims and keep your insurance premiums down. With a reduction in claims and risk mitigation strategies in place, insurance carriers take on less risk and can transfer those savings to clients.

Sean Peek contributed to this article.