When getting ready to launch a new business, you must find the thousands — sometimes hundreds of thousands — of dollars often required to get started. Options for startup capital include debt financing and equity financing. While debt financing involves borrowing money and repaying it with interest, equity financing involves selling shares of your company. While you can pursue both types of funding, you should understand the differences before making a decision.

Debt vs. equity financing

In finance, a company’s capital structure consists of debt and equity. If you look at a statement of shareholder equity, you’ll see that equity is calculated as the difference between the value of the business’s total assets and liabilities. Debt financing and equity financing both have pros and cons. The right option for your business depends on your startup’s financial situation and your goals as a business owner.

What is debt financing?

Debt financing involves taking out a loan to fund your startup. As with any loan, you pay back the principal with interest over a specified time period. Term loans and lines of credit are two common types of business loans.

“Debt financing in simple terms is ‘using other people’s money,’ a.k.a. O.P.M. In exchange, you pay them interest for a specific period of time until paid back in full,” said Katrina Cooks Fitten, CEO and CFO of New Day For You Financial.

>> Looking to borrow money? Check out our picks for the best small business loans.

Pros of debt financing

These are some of the benefits of debt financing.

- Independence: Debt financing providers don’t get a say in how you run your startup. In contrast, equity financing requires you to hand over a stake in your company, which gives investors more sway over your business decisions.

- No profit sharing: With debt financing, your profits remain entirely yours. With equity financing, investors are eventually entitled to a portion of your profits.

- Easy budget forecasting: With a fixed-rate loan, your loan payments won’t change. That’s why budget forecasting is significantly easier when you opt for debt financing over other types of funding. With unchanging monthly fees, your future expenses are more predictable. [Business.com’s free small business budget template can help.]

- Less complicated: Options for debt financing include personal loans, credit cards, family loans with interest, bank loans and SBA loans. These methods let you retain full ownership of your business while meeting the obligation to repay the borrowed amount with interest.

Cons of debt financing

These are some drawbacks of debt financing.

- Repayment: Unlike with equity financing, you must repay the money you receive from debt financing. If your startup doesn’t generate the cash flow needed to service the debt, you may end up defaulting on your business loan. Before you jump into an agreement, ensure that you know how to calculate loan payments. [Use our free debt payoff calculator.]

- Interest: Your monthly interest expenses on the loan could be quite large at a time when you must minimize your startup costs. The good news is that any interest you pay on debt financing is tax-deductible. In the long run, that deduction could outweigh the immediate financial burden.

- Liability: Even if your business structure limits your personal liability in the event of a lawsuit, certain debt financing providers require you to put up your assets as collateral. If you fail to repay your loan, your lender may be able to acquire your assets.

Uber, Airbnb and Dropbox are a few well-known companies that used debt financing as part of their growth strategies.

What is equity financing?

Equity financing involves selling a stake in your company to an investor in exchange for the capital your business needs to grow.

“Instead of a loan, someone is investing in your business and typically receiving shares of the company in return,” said Joe DiSanto, a fractional CFO and financial consultant. “Essentially, you’re taking on a partner who now owns a portion of the company.”

Startup investors include angel investors and venture capitalists. Angel investors are often individuals who provide early-stage funding, while venture capitalists are firms that step in at a later stage.

Pros of equity financing

These are some of the advantages of equity financing as a source of capital.

- No repayment: You’re not required to repay funds obtained through equity financing. Instead, investors are betting they will make money from future cash flows or from selling their stake. “Equity financing eliminates the risk of default, as there are no fixed repayment schedules,” explained Jay Jung, founder of Embarc Advisors and a former investment banker. “This makes it an attractive option for businesses in early or volatile stages where cash flow predictability is low.”

- No interest: Since equity financing doesn’t require debt repayment, you don’t have to worry about making interest payments.

- Cash preservation: Unlike other types of funding, equity financing doesn’t require regular payments. This allows you to conserve more cash to grow your business, rather than having it go to interest payments and loan payback.

- Additional benefits: Taking on partners through equity financing can lead to extra perks. “These partners may contribute not only financial resources but also their network, expertise and vested interest in the success of your business,” said DiSanto.

Cons of equity financing

The drawbacks of equity financing primarily relate to the ownership you grant your investor.

- Loss of independence: Equity investors often take an active role in the startup. If your ownership stake is diluted through repeated equity offerings, you risk losing control of the business.

- Profit sharing: An ownership stake entitles investors to a portion of your future profits. For example, say you offer an investor 30 percent ownership in exchange for capital. In this case, you may need to set aside 30 percent of your profits for that investor.

- Differences of opinion: You and your new shareholders won’t always agree on how the company should be run. If you don’t have strategies in place to solve these conflicts, it could cause tremendous strife within your organization.

- Not feasible for all businesses: For smaller businesses — e.g., a cafe or yoga studio — it’s more difficult to attract venture capital or angel investors unless they’re friends or family. “Investors like these typically focus on startups with significant scalability and the potential to go public or be sold at a high value,” explained DiSanto.

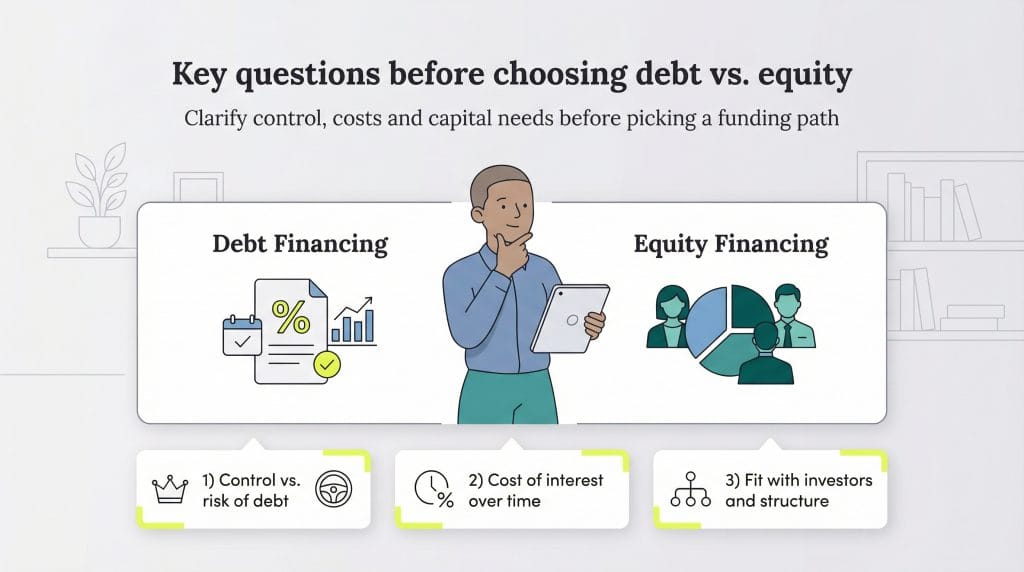

Questions to consider before choosing debt vs. equity financing

Before you decide between debt and equity financing, you should ask yourself the following questions.

1. Which is more important: decision-making authority or minimal debt?

Are you the kind of business owner who can’t stand the thought of sharing decision-making authority with someone else? Then you might see debt financing as your way out. However, let’s say you forecast your budget and determine that you might struggle to repay debt financing. In this case, it may be best to play it safe and accept the loss of control that accompanies equity funding.

2. What are the current interest rates on debt financing?

Interest rates deserve careful attention when weighing your debt financing options. Even a modest rate shift can significantly drive up borrowing costs — a reality many business owners learned firsthand during recent Federal Reserve rate cycles. Average interest rates on commercial and industrial loans have shifted considerably in recent years, making it critical to assess your repayment capacity before committing. Interest rates can make or break a new company, especially because it often takes years for a startup to achieve profitable growth.

Monthly payments on business loans can increase dramatically when interest rates start to rise.

3. How much capital do I need, and what are the consequences?

Do you need so much capital that you’re already worried about repaying the debt financing for it? If so, equity financing may be a safer bet. However, when you provide equity in return for a large amount of capital, your investors will likely require a proportionately large share of your company. If your investor requests more than 50 percent ownership of your company, your decision-making authority could disappear. This is especially true when you are no longer a startup.

4. Will my business structure easily allow equity financing?

Equity financing requires you to give ownership shares to your investors. However, not all business structures can easily explore this funding route. For example, if your company is a partnership, its ownership structure may not be flexible enough to accommodate new shareholders. You can always change your type of business operation, but it’s a lengthy process. [Learn how to dissolve a partnership agreement.]

5. Can I actually find equity financing?

Entrepreneurs often assume equity financing is readily available, but that isn’t always true. Not all business owners find investors who are interested in their companies. Other startup founders find investors only after months of searching. So, this funding option might not work for you if you need cash fast.

“For many tech startups and early-stage companies, equity financing is often the default choice,” said Jung. “These businesses typically lack the hard assets or steady cash flow required to secure traditional debt. Exceptions may include venture debt, which is underwritten based on institutional backing rather than cash flow.”

Beyond startups, equity financing is also well-suited for businesses planning significant expansion or scaling efforts — such as acquiring another company, launching new product lines or entering new markets. According to the National Venture Capital Association’s 2024 Yearbook, U.S. venture capital investment totaled more than $170 billion across nearly 14,000 deals in 2023, underscoring that equity capital remains a viable and active funding path for high-growth businesses.

On the other hand, debt financing providers will lend money to virtually any entity that qualifies. Can you show a strong credit history, present a convincing business plan and prove that you can repay the loan? If so, you might be in good shape for approval.

Whether you ultimately go with debt financing, equity financing or both, the right choice depends on your business model, growth stage and long-term goals. Taking time to evaluate both options thoroughly puts you in the best position to fuel sustainable growth.

Anna Baluch and Mike Berner contributed to this article. Source interviews were conducted for a previous version of this article.