If you’re thinking about applying for a business loan, understanding your SBSS score can make a big difference. A strong score can boost your chances of getting the funding you need, so you’re not left scrambling to make ends meet each month.

Still, many business owners haven’t heard of the SBSS score, let alone know how to improve it. We’ll break down what the SBSS score is and why it matters, and share practical tips to help you strengthen it and improve your funding prospects.

What is an SBSS score?

The FICO Small Business Scoring Service (SBSS) is one of the main models lenders use to evaluate a company’s business credit score. While FICO is best known for tracking personal credit scores, the SBSS is specifically designed for evaluating business credit.

Using automated tools and data modeling, FICO designed the SBSS score to provide lenders with a quicker and more consistent way to assess a business’s credit risk. This makes it easier for lenders to evaluate loan applications and for small business owners to access the funding they need, without delays caused by manual reviews.

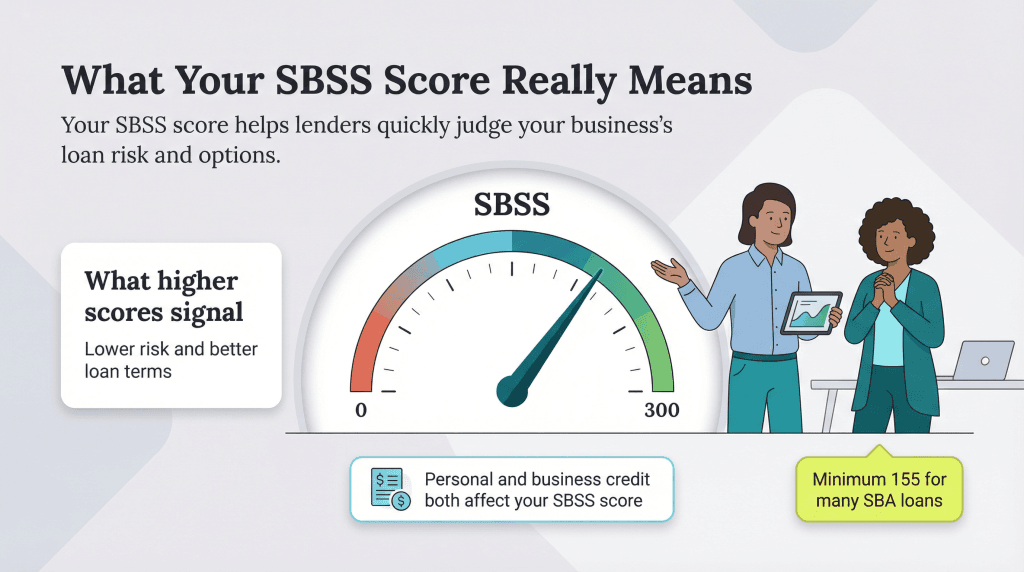

What sets the SBSS apart is that it draws from both business and personal credit data, reflecting FICO’s long track record in consumer credit scoring. This combination helps lenders get a clearer picture of a business’s financial health from the start. [Read related article: Best Business Loans for Bad Credit]

Other business credit scores:

In addition to the SBSS, lenders may also look at scores from other credit bureaus. Each agency uses its own scoring model:

- Dun & Bradstreet Paydex score: Ranges from 0 to 100. A score above 80 is considered strong.

- Experian Business Credit Score: This score also ranges from 0 to 100. Scores above 76 are typically seen as low risk.

- Equifax Business Credit Risk Score: Utilizes a proprietary model with distinct scoring ranges and risk indicators.

Unfortunately, there’s no universal scoring system for business credit. Each provider uses its own proprietary formula, making it difficult to directly compare scores across agencies and determine exactly which factors carry the most weight.

What does your SBSS score mean?

Your SBSS score falls on a scale from 0 to 300, and the higher, the better. Lenders use this score to assess how risky it might be to lend to your business.

Your score reflects both personal and business financial data, including credit history, revenue, time in business and any outstanding liens. A strong SBSS score signals that you’re a lower-risk borrower, which can help you qualify for better loan rates and repayment terms.

For example, to qualify for an SBA 7(a) Small Loan, you’ll generally need a minimum score of 155. If your score falls below that threshold, your application may still be considered; however, it will undergo a manual review and require additional documentation.

Even though your business is a separate entity, lenders may still review your personal credit history when evaluating your loan application. Paying off personal or

business debt can improve your overall profile and boost your chances of approval.

Why do you need to know your SBSS score?

Knowing your SBSS score gives you a clearer picture of how lenders view your business’s creditworthiness. It can help you spot potential red flags, understand what’s affecting your loan eligibility and make smarter financial decisions before applying for funding.

“Knowing your SBSS score gives you visibility, control and leverage,” explained Joe Camberato, CEO of National Business Capital. “It’s not just a number — it’s a roadmap to stronger financial health and greater opportunity for your business.”

Here are a few reasons why understanding your SBSS score is so important:

- Plan ahead: Knowing how your SBSS score works helps you prepare in advance, so you’re ready when it’s time to apply for a loan.

- Avoid costly surprises: Camberato emphasized that your SBSS score can make or break your financing prospects, so walking in blind is a risk. “Just like you wouldn’t blindly apply for a mortgage without knowing your personal credit score, you don’t want to walk into a business loan application not knowing where you stand,” Camberato said. “When you know your score upfront, it helps you avoid surprises and gives you a chance to fix issues before you apply.”

- Reduce the risk of rejection: Understanding your score early in the process gives you the upper hand and can help you avoid a denial — or at least better prepare for follow-up questions.

- Get better loan terms: Mark Valentino, head of business banking at Citizens, explained that a strong SBSS score can lead to more favorable financing rates, payment terms and loan agreements. “This will significantly lower costs (and stress levels), allowing you to reinvest in growth and innovation,” Valentino noted.

- Build lender and investor trust: Valentino also pointed out that solid business credit enhances your standing with partners and investors. “Maintaining excellent business credit can be a game-changer, driving success and sustainability for your enterprise,” Valentino added.

- Understand what lenders expect: There’s increasing reliance on the SBSS score, so ignoring it is no longer an option. “More lenders are using it because it helps them make faster, more accurate lending decisions. This affords them the time to make decisions in hours, not days,” said Levi King, CEO, co-founder and executive chairman of Nav, an online credit monitoring service that provides small business owners with their SBSS score.

King also noted that despite its importance, many entrepreneurs are still unaware of the score’s existence. “It’s the one credit score all business owners should know, but many have never heard of it because, until now, it’s been hard to get your hands on it,” King added. “Banks aren’t required to disclose that they use the FICO SBSS score, and very little information exists about it online,” King said.

Understanding your SBSS score gives you visibility, control and leverage. It's not just a number: It's a roadmap to stronger financial health, better

business loan approval odds and greater opportunities for your organization.

What’s a good SBSS score?

The FICO SBSS score ranges from 0 to 300, with higher scores indicating lower credit risk. While each lender sets its own thresholds, and thresholds can vary by loan type, a score above 160 to 180 is typically considered strong enough to qualify for loans under $1 million. Lower scores may still be eligible for smaller loans, though they often require more documentation or a manual review.

Because the SBSS score is used by the SBA and many private lenders, knowing where you stand can help you set realistic expectations and improve your chances of approval.

How is your SBSS score calculated?

FICO doesn’t disclose its full scoring formula, but your SBSS score is based on a mix of business and personal financial data. Key business factors include:

- Credit history

- Cash flow

- Business assets

- How reliably it pays vendors and lenders

Other considerations may include:

- Industry risk

- Time in business

- Credit utilization

- Public records (e.g., bankruptcy filings, tax liens)

Your personal FICO score also plays a role, especially if your business is newer and hasn’t yet built a strong credit profile.

FICO pulls this information from multiple sources, including your loan application, commercial credit reports and personal credit data. If your business history is limited, your personal credit may carry more weight in the score.

How do you improve your SBSS score?

Strong financial habits can help raise your SBSS score and put you in a better position when it’s time to seek funding. Valentino likened building a strong business credit rating to constructing a house.

“Each positive action, like paying bills on time or keeping accounts open, adds another brick to your credit house, making it stronger and more resilient,” Valentino said. “Just as a well-built house better withstands storms and adverse weather, a robust credit rating can help your business face financial challenges and secure better financing options.”

Here’s where to start:

1. Pay your bills on time.

Timely payments — both business and personal — play a major role in your SBSS score. That includes paying vendors, suppliers and lenders by the due date or even early if possible. Since your personal FICO score is factored into your SBSS, staying current on personal bills is equally important.

Valentino emphasized that paying on time is the foundation of a strong business credit profile.

“Setting up reminders or putting automated payment systems into place can help to ensure punctuality,” Valentino noted. “If you anticipate any difficulty in making a payment, communicate with vendors or creditors as well as with your financial advisor or banker, in order to immediately arrange a payment plan, thus avoiding a negative report.”

2. Reduce your credit utilization rate.

Your credit utilization rate is the percentage of credit you’re using compared to what’s available, and it can impact both your personal and business credit scores. For example, if you have $50,000 in available credit and you’re using $40,000, your utilization is 80 percent. That’s considered high. Aim to keep it below 30 percent to show lenders you’re managing credit responsibly without maxing it out.

3. Use good accounting practices.

Good accounting habits can go a long way in improving your SBSS score. When you manage your cash flow well, you’re more likely to pay suppliers on time and stay on top of other financial obligations. Using one of the best accounting software solutions can help simplify the process and keep your records organized.

This becomes especially important if you’re exploring nontraditional funding. Some alternative lenders report payment history to credit bureaus, which can positively impact your SBSS score if your financial records are in order and payments are on time.

Amanda Hoffman contributed to this article.