Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

As your business expands internationally, navigating GAAP, IFRS and local regulations becomes critical. Here’s how modern ERP systems help maintain compliance.

This article is sponsored by Intuit.

Imagine this scenario: Your U.S.-based company just signed its first European distribution deal. The revenue is exciting, but the financial reporting implications are immediate and complex. Alongside the Generally Accepted Accounting Principles (GAAP) your team already follows, you now need to understand International Financial Reporting Standards (IFRS), which are required or permitted in more than 150 jurisdictions worldwide. Depending on the deal structure, you may need to report under both frameworks simultaneously, each with its own rules for recognizing revenue, consolidating subsidiaries and presenting financial statements.

The stakes of getting this wrong are significant. Regulatory non-compliance can result in fines ranging from thousands to millions of dollars, depending on the jurisdiction and severity of the violation. Beyond financial penalties, businesses risk audit failures, legal action from shareholders or regulators, restricted access to international capital markets and lasting reputational damage that erodes investor confidence and customer trust.

In this article, we’ll walk through the major global accounting standards your growing business needs to understand, the most common compliance challenges that arise during international expansion, and how modern enterprise resource planning (ERP) systems like Intuit Enterprise Suite can help you maintain compliance across multiple standards without burying your finance team in manual processes.

At a high level, businesses operating internationally must contend with two major accounting frameworks.

On top of these two dominant frameworks, many countries layer their own local regulations, tax codes and reporting requirements. A business with subsidiaries in Germany, Brazil and Singapore, for example, might need to comply with EU-adopted IFRS, Brazilian GAAP (which converged with IFRS but retains local nuances) and Singapore Financial Reporting Standards — all while consolidating everything back into GAAP-compliant reports for U.S. stakeholders.

Growing businesses encounter this complexity for several reasons. International investors may require IFRS-based financial statements as a condition of funding. Cross-border transactions introduce multi-currency accounting obligations and transfer pricing considerations. And acquisitions of foreign companies bring new subsidiaries that may already be reporting under a different standard, requiring reconciliation and consolidation across frameworks.

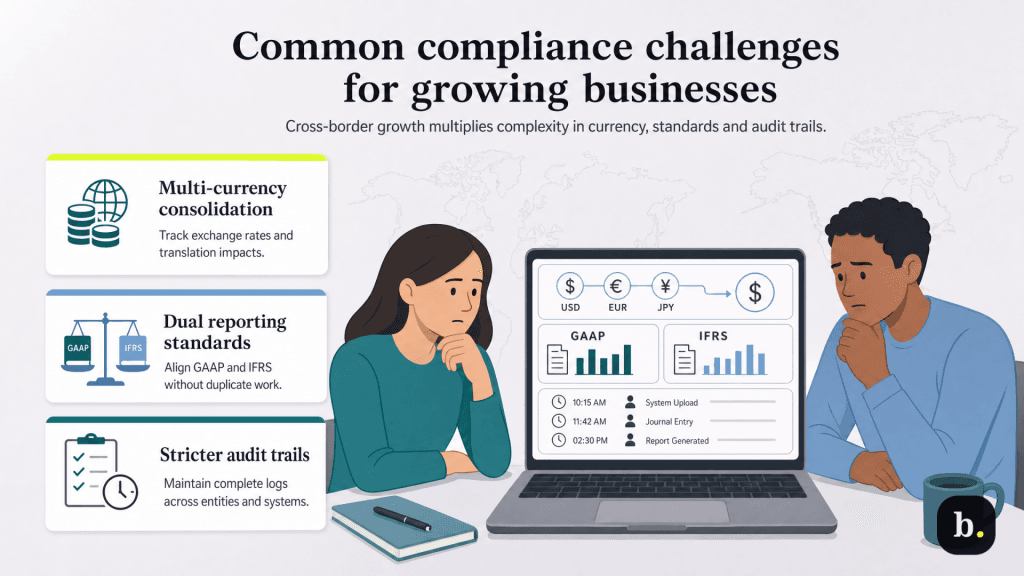

One of the first complications businesses face when operating across borders is multi-currency accounting. Every transaction involving a foreign currency must be translated into the company’s functional currency for reporting purposes, and the exchange rate used can vary depending on the type of transaction and the date it occurred.

This becomes especially challenging during financial statement consolidation. When rolling up the financials of a foreign subsidiary into the parent company’s reports, different line items may require different exchange rates, including current rates for balance sheet items, average rates for income statement items and historical rates for equity.

Fluctuations in exchange rates between reporting periods can create foreign currency translation adjustments that affect the bottom line, and managing these adjustments accurately across multiple entities requires careful tracking and consistency.

Without an automated system in place, finance teams often resort to manual spreadsheet calculations to handle currency conversions, which increases the risk of error and makes the reconciliation process slower and more labor-intensive.

Revenue recognition is one of the areas where GAAP and IFRS diverge most meaningfully, despite both frameworks adopting a similar five-step model (ASC 606 under GAAP and IFRS 15, respectively). The core steps (identify the contract, identify performance obligations, determine the transaction price, allocate the price and recognize revenue) are conceptually aligned. However, the application of these steps can produce different results.

For example, GAAP provides more prescriptive, rules-based guidance for handling specific scenarios such as licensing arrangements, contract modifications and variable consideration. IFRS, being principles-based, allows for more judgment, which can lead to different timing of revenue recognition for the same underlying transaction. A SaaS company recognizing subscription revenue, a manufacturer with long-term contracts or a service firm billing on milestones may each face situations where the two frameworks yield different reported figures.

For businesses that need to report under both standards, this creates a dual-reporting burden. Maintaining two sets of books (or at minimum, tracking the adjustments needed to reconcile one framework to the other) without introducing errors or duplicating data entry is a persistent operational challenge.

Regulatory bodies in different jurisdictions have varying expectations for what constitutes adequate financial documentation. In the U.S., the Sarbanes-Oxley Act imposes strict internal control requirements on public companies, including comprehensive audit trails that track every transaction from initiation to reporting. European regulators have their own documentation standards, and many Asian markets have adopted increasingly rigorous transparency requirements as well.

At minimum, regulators generally expect complete transaction histories with timestamps, user access logs showing who entered, approved or modified financial data, documented approval workflows for material transactions, and change tracking that shows any amendments to previously recorded entries. Maintaining this level of documentation across multiple entities, currencies and accounting frameworks compounds the administrative burden, and any gaps in the audit trail can trigger regulatory scrutiny or audit findings.

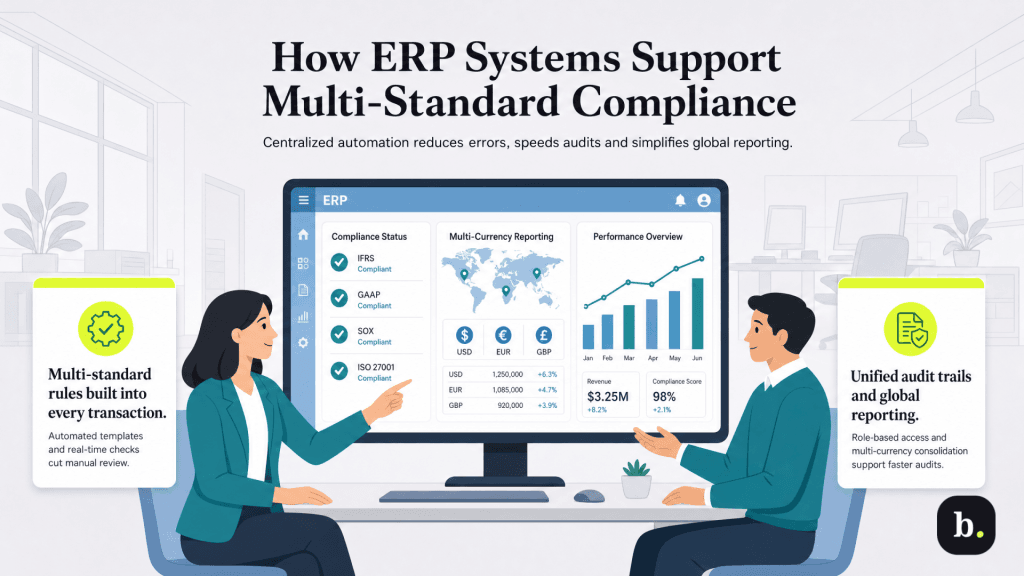

Modern ERP platforms are designed to reduce the compliance burden by embedding accounting standards directly into the system’s architecture. Rather than requiring finance teams to manually apply the rules of each framework to every transaction, these systems offer pre-configured templates, automated chart of accounts mapping and real-time compliance checking during transaction entry.

Intuit Enterprise Suite, for example, offers automated revenue recognition capabilities that create a permanent, time-stamped audit trail for every transaction. According to a Forrester study commissioned by Intuit, finance teams using Intuit Enterprise Suite estimated they spent 50% less time running ad hoc reports, a benefit that directly supports faster, more streamlined audit processes.

For companies with both U.S. and international operations, having these compliance frameworks built into the system reduces the risk of human error and ensures consistency across entities.

Multi-currency support is a critical feature for any ERP system serving businesses with international operations. Modern platforms handle currency translation, exchange rate updates and consolidated reporting across currencies, reducing the manual work and error risk associated with spreadsheet-based conversions.

Intuit Enterprise Suite supports multi-currency accounting and provides consolidated reporting with real-time dashboards for operations spanning multiple countries. Its multi-entity management capabilities allow finance teams to consolidate financial data across subsidiaries – even when those subsidiaries operate in different currencies – using automated intercompany transactions and reconciliations.

Alternative ERP solutions like NetSuite and Sage Intacct offer similar multi-currency functionality, but the right choice depends on the size and complexity of your operations, your existing technology stack and the specific compliance frameworks you need to support.

A comprehensive, centralized audit trail is one of the most important features an ERP system can provide for compliance purposes. Rather than piecing together documentation from disconnected systems, a unified ERP maintains a single record of every transaction, every approval and every modification across all entities.

Intuit Enterprise Suite enforces role-based permissions and detailed audit trails, ensuring that only authorized individuals can access or modify sensitive financial data. Its approval workflows allow businesses to route material transactions through appropriate review chains before they’re finalized and its customizable audit trail makes it straightforward to generate compliance reports for auditors.

These capabilities are especially valuable during audit season, when finance teams need to produce detailed, traceable documentation showing how every revenue figure was recognized and every account was reconciled.

Choosing the right ERP system is an important step, but technology alone doesn’t guarantee compliance. Businesses that successfully maintain multi-standard compliance over time typically follow several operational best practices.

Not every business needs an ERP from day one, but there are clear signals that your current accounting system is no longer sufficient for your compliance needs.

If your finance team is spending more time on manual workarounds – maintaining separate spreadsheets for currency conversions, manually reconciling between accounting standards, or hand-building audit documentation – than on actual financial analysis, that’s a strong indicator. Similarly, if you’re adding international entities or investors who require reporting under a different accounting framework, your current system’s limitations will become apparent quickly.

When evaluating ERP systems for compliance capabilities, ask vendors specific questions:

The answers to these questions will help you distinguish between systems that treat compliance as a core feature and those that treat it as an afterthought.