This article is sponsored by Intuit.

For small businesses, getting paid on time is the difference between making payroll and scrambling to cover it. Yet the reason customers pay late often has less to do with unwillingness than with friction. When paying an invoice means digging out a checkbook, logging into a bank portal or waiting for someone in accounts payable to cut a check, the invoice slides down the priority list.

Removing that friction by accepting the payment methods customers already prefer is one of the most direct levers a business owner has over cash flow. This guide explains why payment friction slows you down, how each major payment method affects speed, and how using a payments platform that offers multiple options can help you get paid faster.

The real cost of slow payments

Late payments are widespread and expensive. According to Intuit’s 2025 QuickBooks Small Business Late Payments Report, 56% of U.S. small businesses are currently owed money on unpaid invoices, and the average affected business is owed roughly $17,500. Nearly half report having invoices more than 30 days overdue.

The damage runs deeper than a delayed deposit. The same report found that businesses more heavily affected by late payments are over 1.4 times as likely to report cash flow problems, and are more likely to lean on credit cards, loans and lines of credit to bridge the gap. With the median U.S. small business holding only about 27 days of cash buffer (according to a JPMorgan Chase Institute analysis of hundreds of thousands of firms), a single stretched invoice can cascade into a missed supplier payment or a payroll crunch.

The strain shows up in day-to-day operations, too. Intuit’s report links heavier exposure to late payments with a greater likelihood of raising prices and with more difficulty hiring skilled workers, the knock-on effects of money that’s owed but not yet in hand. When cash is tied up in receivables, owners have fewer resources to reinvest, negotiate supplier discounts or move quickly on an opportunity.

In other words, receivables that arrive slowly actively constrain what a business can do next. Speeding up collections is therefore one of the highest-return operational changes a small business can make, and it often costs far less than the credit it replaces. And unlike raising prices or cutting costs, it doesn’t require asking customers to pay more or accepting less yourself, it simply gets money you’ve already earned into your account sooner.

Why payment friction is really a speed problem

It’s tempting to treat a late payment as a customer problem, but usually it’s a process problem. When paying is inconvenient, invoices get set aside — not out of bad faith, but because the path of least resistance is to deal with it later.

The friction points are familiar. Paper checks have to be written, signed, and mailed, then clear over a period of days; the Consumer Financial Protection Bureau notes banks can take up to two business days just to settle a check once it’s deposited, on top of the time to prepare and mail it. Manual bank transfers require the payer to log in, re-enter your account details and initiate the transfer. Each added step is another opportunity for the payment to stall.

Customer preference compounds the issue. Research from TreviPay found that 72% of B2B buyers say they’re more loyal to businesses that let them pay with their preferred method. When you accept only one or two methods, you’re effectively asking some customers to go out of their way to pay you. Remove that mismatch, and payments move faster because paying is easy.

Timing matters as much as method. A customer is most likely to pay in the moment they’re actually looking at the invoice, which is when the amount, the reason and the intent to pay are all top of mind. If paying requires closing the invoice and coming back later through a separate channel, the payment competes with everything else on the customer’s plate. The methods that collect fastest are the ones that let a customer act on the impulse to pay the instant they have it.

Every extra step between "invoice received" and "payment sent" adds days to your collection cycle. Digital methods that let a customer pay directly from the invoice remove those steps, which is why they consistently settle faster than paper alternatives.

The main payment options (and what each does for speed)

No single payment method suits every customer, and each involves trade-offs among speed, cost and convenience. Here’s how the most common options stack up.

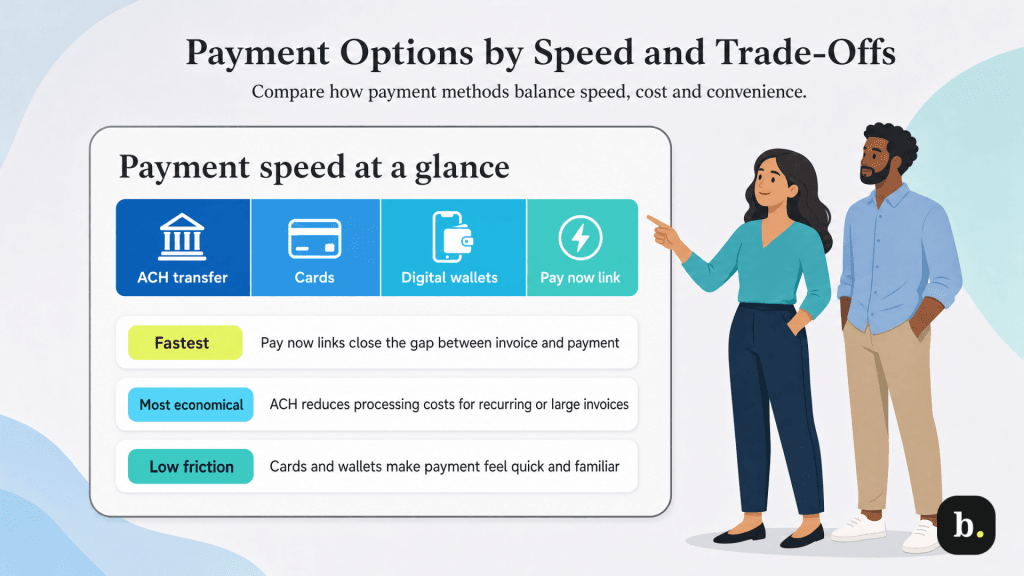

ACH and bank transfers

ACH transfers move money directly between bank accounts and are a workhorse of B2B payments, largely because they’re inexpensive. They’re meaningfully faster than paper checks; ACH batches settle several times per business day. For recurring or high-value invoices where processing cost matters, ACH is often the most economical choice, and it removes the mailing and check-clearing delays entirely.

One caveat worth noting: when ACH is offered as the only electronic option, some customers still find the setup – which involves locating account numbers and initiating the transfer – cumbersome, which is precisely why pairing it with a one-click alternative helps.

Credit and debit cards

Credit and debit card payments are familiar and low-friction: a customer can pay the moment they see the invoice, often in a couple of clicks. That immediacy is exactly what speeds collections, and it’s why cards frequently get invoices paid the same day they’re received.

The trade-off is you’ll incur payment processing fees, which run a percentage of each transaction. For many businesses, faster access to cash and a higher likelihood of prompt payment justify the fee, particularly when the alternative is waiting weeks or drawing on credit.

Digital wallets

Digital wallets and payment services let customers pay from a mobile device using credentials they’ve already stored. Adoption continues to climb as buyers increasingly expect the same quick, tap-to-pay experience they get as consumers. For businesses whose customers skew toward mobile or want minimal-effort checkout, offering a wallet option removes yet another reason to delay.

“Pay now” invoice links

Perhaps the single biggest speed unlock is embedding a payment link directly in the invoice. Instead of receiving a bill and then separately figuring out how to pay it, the customer clicks “pay” and completes the transaction in the same moment, often routing to a card, ACH or wallet behind the scenes. Removing the gap between “I should pay this” and “I’ve paid this” is what turns a 30-day invoice into a same-week one.

Why offering several options compounds the effect

Each method speeds things up on its own. Offered together, they do something more: they eliminate the excuse. When an invoice supports cards, ACH and a wallet, virtually every customer can pay the way that’s fastest and most natural for them, so almost no one is left waiting on a method they find inconvenient.

This matters because the customer who prefers a card and the customer who prefers a bank transfer are two different people, and forcing either onto the other’s method introduces delay. Meeting each where they are shortens the average time to payment across your whole receivables base, not just for one segment.

There’s a retention benefit as well. Because buyers report being more loyal to businesses that accommodate their preferred payment method, offering options can also make customers more inclined to keep working with you and to pay promptly the next time. Convenience and goodwill tend to reinforce each other.

Providing payment options also opens the door to autopay and recurring billing for repeat clients. Once a customer stores a preferred method, subsequent invoices can be paid automatically or in a single tap, collapsing the collection cycle for ongoing relationships to nearly zero effort on either side. For businesses built on retainers, subscriptions or repeat orders, that shift from chasing each invoice to collecting on a schedule can transform cash flow predictability.

Putting it into practice

Turning payment optionality into faster cash flow comes down to a few practical moves:

- Enable multiple methods on every invoice. Give customers a genuine choice – card, ACH and a digital wallet at minimum – so no one has to leave the invoice to pay it.

- Embed a “pay now” link. Make the invoice itself the point of payment rather than a prompt to go pay somewhere else. The fewer clicks between receipt and payment, the faster the money lands.

- Automate reminders. A polite, automatic nudge before and after the due date recovers a surprising share of invoices that would otherwise drift, without the awkwardness of chasing manually.

- Automate reconciliation. Matching incoming payments to open invoices by hand is slow and error-prone. Systems that reconcile automatically free up time and keep your books accurate as volume grows.

This is where a connected tool earns its keep. QuickBooks Online, for example, lets businesses add multiple payment options directly to invoices through QuickBooks Payments, so a customer can settle a bill the moment they open it. Because payments and bookkeeping live in the same platform, incoming payments are matched to invoices and reconciled automatically, and automated reminders can go out without anyone remembering to send them. The result is fewer manual steps between issuing an invoice and seeing the cash, which is the whole point of expanding your payment options in the first place.

Speed payments up by making it easy for your customers

Slow payments are rarely a sign that customers won’t pay; more often, they’re a sign that paying is harder than it needs to be. By accepting the methods customers already prefer and letting them pay straight from the invoice, businesses remove the friction that turns a two-week payment into a two-month one. Among the levers a small business owner can pull to protect cash flow, expanding payment options is one of the lowest-effort and highest-return moves available.