Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

ACH payments can help small businesses lower costs, improve cash flow and move money more efficiently.

If your business sends payroll through direct deposit, pays vendors electronically or collects recurring customer payments straight from a bank account, you’re probably already using ACH, even if you’ve never thought much about the system behind it.

For small businesses, ACH payments are one of the most affordable ways to move money. Transaction fees are usually far lower than credit card processing costs, making ACH especially attractive for recurring billing, high-ticket invoices and B2B payments. The trade-off? ACH payments typically take longer to settle than card transactions. But for many businesses, the cost savings are well worth the extra time. This guide explains what ACH payments are, how they work, what they cost, how long they take and how to set them up for your business.

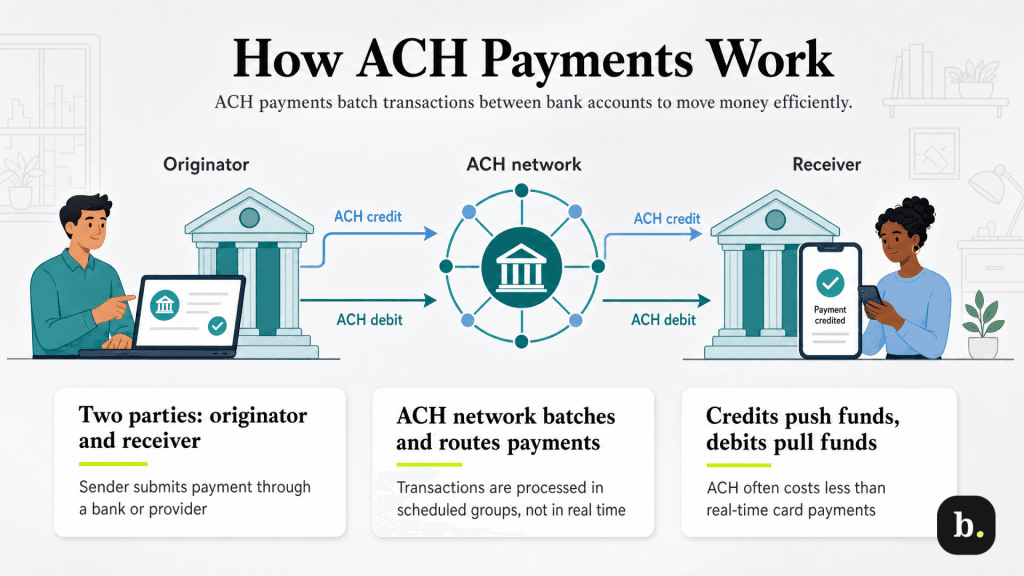

ACH payments are electronic bank-to-bank transfers processed through the Automated Clearing House network, the system that moves money between financial institutions in the United States. If you’ve ever received a paycheck through direct deposit, paid a utility bill through autopay or transferred money electronically from one bank account to another, you’ve used the ACH network.

For businesses, ACH payments are commonly used for payroll, vendor payments, recurring customer billing, tax payments and other account-to-account transfers. Unlike credit card payments, ACH transactions move money directly between bank accounts, which usually keeps payment processing costs low, especially for larger amounts.

Every ACH transaction involves two parties:

The originator submits the payment through a bank or third-party payment provider to the ACH network, which is operated by Nacha, the organization that governs ACH payments in the U.S. The network groups transactions together, routes them to the receiving bank and ultimately credits or debits the receiver’s account.

There are two main types of ACH transactions:

Unlike credit card payments, which are authorized in real time, ACH transactions are processed in batches at scheduled intervals. That’s one reason ACH transfers typically take longer to settle — and one reason they usually cost less.

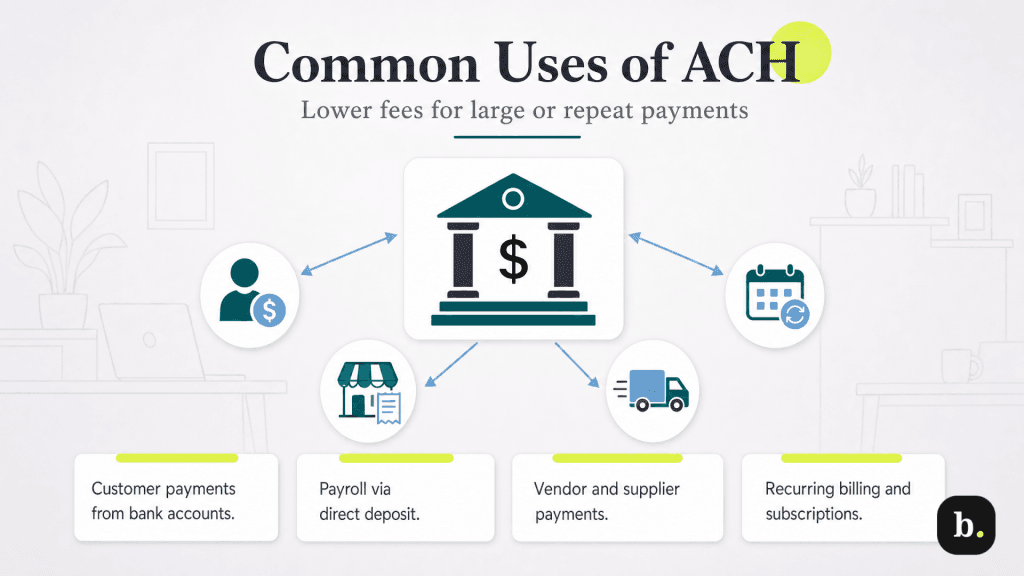

Small businesses use ACH for everything from collecting customer payments and paying vendors to running payroll, reimbursing employees and setting up recurring billing. Because ACH fees are usually lower than credit card processing costs, it can be especially useful for larger transactions, repeat payments and back-office transfers where speed matters less than cost savings.

Here are some of the most common ways small businesses use ACH payments:

ACH is becoming a go-to payment method for businesses that want to keep processing costs under control, especially on larger invoices where card fees can add up fast. When you give customers the option to pay directly from their bank account, the savings can be significant. A $5,000 invoice paid by credit card at 2.9 percent + $0.30 costs $145.30 in processing fees. The same invoice paid through ACH at a typical $0.50 flat fee costs 50 cents.

ACH also works well for recurring billing. Subscription businesses, membership organizations, property managers collecting rent and service providers on monthly retainers can set up automatic ACH debits that pull payment on a set schedule. Over time, those lower transaction costs can add up to meaningful savings.

ACH can be a much simpler alternative to paper checks when you’re paying vendors, suppliers or other recurring business expenses. Compared with mailing a check, ACH payments are usually faster, easier to track and far less vulnerable to check fraud. Instead of waiting on mail delivery and bank processing, you can see exactly when a payment was sent and when it clears.

Many businesses also use ACH for recurring obligations like rent, equipment leases and regular supply orders. And because many of the best accounting software platforms support ACH vendor payments, you can often send those transfers directly from your bookkeeping software.

If your business pays employees through direct deposit, you’re already using ACH. Those payroll deposits move through the ACH network every time your provider sends wages to employees’ bank accounts.

For many small businesses, payroll is the most familiar ACH use case, and in many cases, it’s already happening behind the scenes through many of the best online payroll services like Gusto, ADP, Paychex and QuickBooks Payroll. Because most employees expect to be paid by direct deposit, ACH payroll has become the standard for businesses with staff.

ACH is also commonly used for business tax payments. Federal taxes can be paid electronically through the Electronic Federal Tax Payment System (EFTPS), and most state tax agencies accept ACH payments for income tax, sales tax and payroll tax obligations.

For larger businesses — or businesses with higher tax liabilities — electronic payment may be required, not optional. Either way, ACH makes it easier to pay taxes on time without mailing checks or worrying about when they’ll clear.

For many small businesses, ACH’s biggest advantage comes down to cost. Transaction fees are usually much lower than credit card processing, which can make a meaningful difference on larger invoices, recurring payments and other high-volume transactions.

ACH fees often fall into one of three pricing models: a flat fee per transaction (commonly $0.20 to $1.50), a percentage-based fee (typically 0.5 percent to 1.5 percent of the transaction amount) or a combination of both.

Many providers using percentage-based pricing cap the fee at a maximum amount per transaction — for example, 1 percent with a $10 maximum. That’s one reason ACH can be especially cost-effective for larger payments.

The table below uses a common credit card processing rate (2.9 percent + $0.30) and a sample ACH flat fee ($0.50) to show how costs can compare at different transaction amounts.

Transaction amount | Credit card (2.9% + $0.30) | ACH (flat $0.50) | Savings with ACH |

|---|---|---|---|

$100 | $3.20 | $0.50 | $2.70 |

$500 | $14.80 | $0.50 | $14.30 |

$1,000 | $29.30 | $0.50 | $28.80 |

$5,000 | $145.30 | $0.50 | $144.80 |

$10,000 | $290.30 | $0.50 | $289.80 |

As you can see, the bigger the transaction, the bigger the savings. For a business processing $50,000 per month in 10 $5,000 payments that could be routed through ACH instead of credit cards, annual savings could easily exceed $15,000.

Beyond per-transaction pricing, some ACH providers also charge monthly platform fees, batch processing fees or setup fees. Be sure to factor those into your total cost comparison. For many small businesses, though, the lower transaction costs on ACH more than offset any fixed monthly fees.

Standard ACH processing usually takes one to three business days from the time a transaction is submitted. The exact timing depends on when the payment is initiated, the ACH network’s processing windows and how quickly the sending and receiving banks process the transfer.

For businesses that need faster settlement, Same Day ACH is also an option. Payments (which can be as high as $10 million per payment starting in 2027) submitted before the provider’s cutoff time may settle the same business day, though some providers charge a small additional fee for expedited processing.

Note that ACH doesn’t process on weekends or federal bank holidays, so, for example, a payment submitted late on Friday may not begin processing until Monday — and funds may not settle until Tuesday or later. If cash flow timing matters, those delays are worth planning for, especially around long weekends and holidays.

The table below compares ACH timing with other common payment methods.

Payment method | Typical settlement | Notes |

|---|---|---|

ACH (standard) | 1-3 business days | Batch processed; no weekends or holidays |

ACH (same-day) | Same day (when cutoff times are met) | Must meet cutoff times; small additional fee may apply |

Credit/debit card | 1-3 business days | Authorization is instant; settlement takes 1-3 days |

Wire transfer | Same day | Immediate and irrevocable; fees typically $15-$50+ |

Paper check | 5+ business days | Includes mail time and bank clearing; risk of loss or fraud |

Both ACH and wire transfers move money directly between bank accounts, but they’re built for very different situations.

For many small businesses, ACH and credit cards aren’t competing options; they often work best together.

For many businesses, the smartest approach is to offer both: credit cards for everyday purchases and ACH for larger, recurring or business-to-business payments.

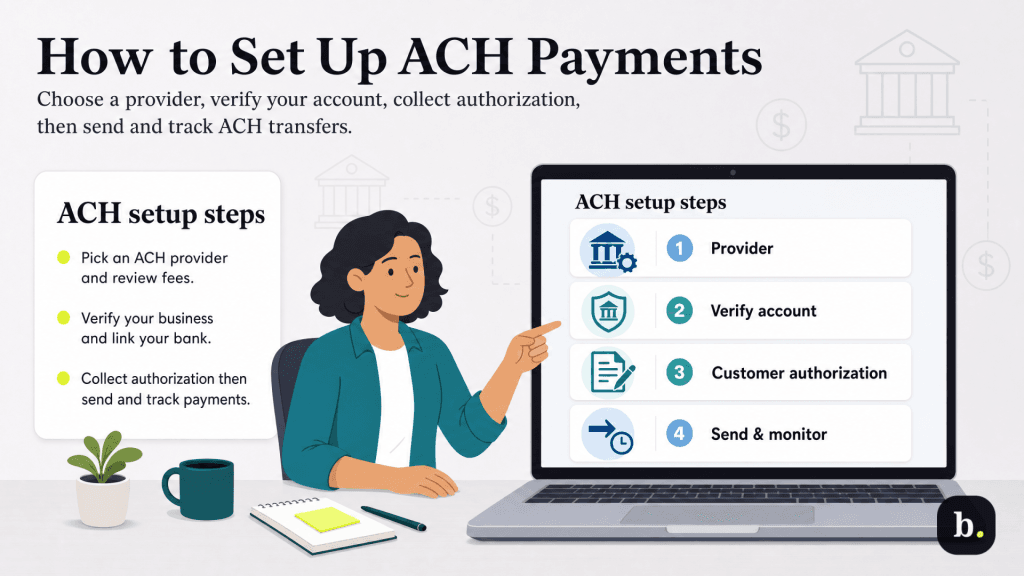

Getting started with ACH usually isn’t complicated, especially if you already use online banking, accounting software or a payment processor. In most cases, the setup comes down to choosing a provider, verifying your business, collecting customer authorization and monitoring your transactions.

Here’s how to get started:

Start by deciding whether you mainly want to send ACH payments, accept ACH payments or do both. Some banks, payroll platforms and payment providers can handle multiple ACH workflows in one place, while others focus on just one use case.

If you’re mainly sending payments, many business banks offer ACH origination, and payroll providers like Gusto, ADP and Paychex can handle payroll deposits behind the scenes.

If you’re mainly accepting ACH payments from customers, many of the best payment processors — including Stripe, Square and PayPal — support bank-to-bank payments alongside card processing, while accounting platforms like QuickBooks, FreshBooks and Xero may build ACH directly into invoicing workflows.

As you compare providers, pay attention to transaction fees, monthly platform fees, integration with your existing tools, Same Day ACH support and any volume limits.

Once you choose a provider, you’ll need to verify your business and connect your business bank account. Depending on the provider, verification may happen through micro-deposits, instant bank verification or standard banking documents.

Approval times vary. Some all-in-one payment platforms approve ACH quickly, while traditional bank-based ACH services may involve a longer underwriting process.

If you plan to collect payments directly from a customer’s bank account, you’ll need their routing number, account number and clear authorization to debit the account.

That authorization isn’t optional. Nacha requires businesses to document customer consent before initiating ACH debits. Many payment platforms handle this automatically through secure online payment forms.

Once your account is active and customer authorization is in place, you can begin sending one-time or recurring ACH payments through your provider’s dashboard, API or invoicing platform.

Keep an eye on payment status as transactions move through the system. If a payment is returned, follow up quickly so you can update your records and avoid disruptions to cash flow.

ACH payments don’t always go through as planned. When a transaction fails, is disputed or can’t be completed, it may come back as an ACH return — essentially the ACH version of a reversed or failed payment.

Returns are assigned standardized reason codes. Some of the most common include insufficient funds, closed or invalid accounts and unauthorized debits, where a customer claims they never approved the transaction.

Most ACH returns happen within two business days of settlement. Unauthorized debit claims can take much longer. Under Nacha rules, customers generally have up to 60 calendar days to dispute an unauthorized ACH debit, which is one reason clear customer authorization matters so much.

Your ACH provider may also charge a small return fee, often $2 to $5 per transaction. One or two returns usually aren’t a major concern, but if they start happening regularly, your provider or originating bank may take a closer look.

To help avoid returns, verify bank account details before initiating debits, keep authorization records current and give customers a heads-up before pulling first-time or variable-amount payments.

ACH security isn’t just your provider’s responsibility. While your bank or payment platform handles much of the technical compliance behind the scenes, your business still plays an important role in preventing fraud, protecting customer data and following the rules around ACH authorization.

Here are some important areas to pay attention to:

ACH isn’t the right fit for every payment, but for many small businesses, it can be one of the easiest ways to lower payment costs.

Recurring invoices, B2B payments, retainers, payroll and other higher-value transactions are often a natural fit for ACH, especially when credit card fees start eating into your margins. Even a business processing $20,000 per month in payments that could move from cards to ACH could save more than $6,000 per year.

The downside is speed. ACH payments usually take one to three business days to settle, and the network goes quiet on weekends and bank holidays. When instant approval matters — think retail purchases or other customer-facing transactions — credit cards will usually be the better fit.

But for the many business payments that don’t need real-time authorization, ACH can deliver the same result at a fraction of the cost. And with most banks, payroll platforms and payment providers now supporting ACH, getting started is often easier than business owners expect.