Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Compensate your employees fairly and legally for appropriate expenditures.

Many situations require employees to make expenditures on behalf of their company. However, if they’re paying out of pocket, they’ll expect timely and accurate reimbursements. To ensure this, businesses should create and communicate a clear expense reimbursement plan outlining all reimbursable expenses, amount limits by category, expense report formats and submission time requirements. We’ll explain what every business owner should know about employee expense reimbursements.

Employee expense reimbursements are monetary repayments to employees who use their own funds for approved work-related expenditures. “Employee expense reimbursements are about paying employees back for work-related costs they cover upfront,” explained Sami Andreani, chief financial officer at Oppizi.

It’s crucial to have an expense reimbursement policy so businesses aren’t hit with unexpected bills and employees aren’t left covering costs due to a mistake. “It sounds simple, but it can get tricky if the process isn’t clear,” Andreani cautioned. “From what qualifies as an expense to how reimbursements are taxed, there’s a lot that employers and employees need to know.”

Steven Kibbel, certified financial planner and founder of Kibbel Financial Planning, emphasized that expense reimbursement plans are about fairness. “Employee expense reimbursement is a process that ensures employees are compensated for work-related costs they pay out of pocket,” Kibbel explained. “At its core, it’s about fairness because employees shouldn’t have to bear the financial burden of performing their job. It’s a structured process with rules, timelines and documentation.”

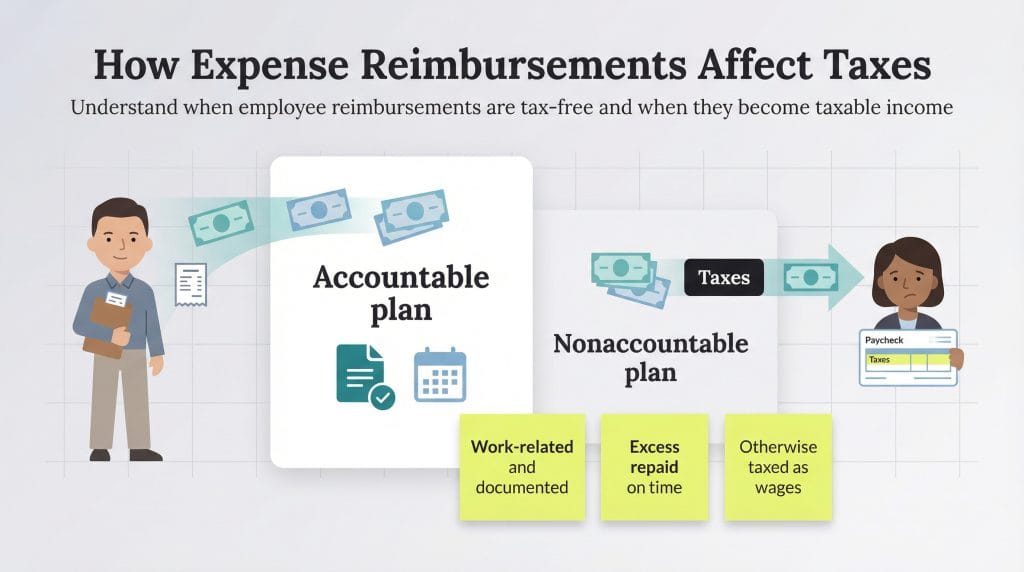

Because money changes hands, employers must carefully manage expense reimbursements to prevent the IRS from classifying the funds as taxable income. Kibbel explained that reimbursements can be handled in two primary ways: accountable plans and nonaccountable plans. Accountable plans are the most common.

According to the IRS Employer’s Tax Guide (Publication 15), if a business has an “accountable plan,” it doesn’t have to count expense reimbursements as part of its employees’ wages, meaning the money is not subject to taxation. This setup is typically most desirable for both employees and employers.

“Accountable plans are more structured,” Kibbel explained. “The employee has to prove the expense was work-related and return any excess reimbursement. With these plans, the employer doesn’t withhold taxes on the reimbursement.”

To qualify as an accountable plan, an expense reimbursement policy must meet the following conditions:

What is a reasonable time frame?

These rules reference “reasonable” time frames, but the IRS does not set a strict definition since circumstances vary. For practical guidance, the IRS considers the following time frames to be reasonable:

If expenses do not meet the accountable plan criteria, the employee reimbursement is treated as paid under a nonaccountable plan. This means the reimbursement is subject to all applicable income and employer payroll taxes.

“Nonaccountable plans … don’t have strict rules, but reimbursements are treated as taxable income, which means employees pay taxes on them,” Andreani explained. “Most companies avoid this because it’s less efficient and can hurt employees financially.”

Payments qualify as part of a nonaccountable plan if they meet one or more of the following criteria:

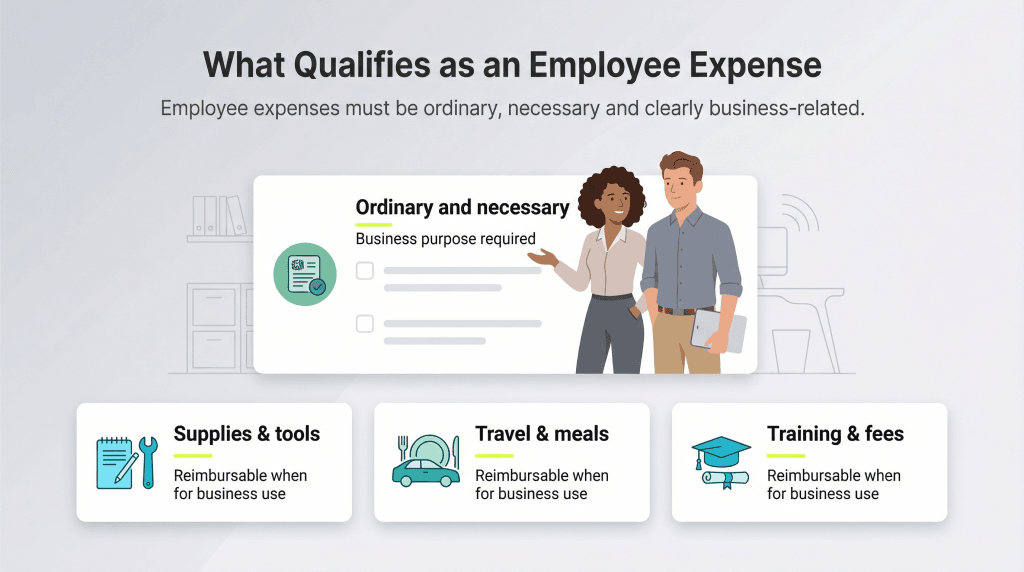

Reimbursable employee expenses must meet the IRS rules for deductible business expenses. According to IRS Publication 535, deductible business expenses must be ordinary and necessary:

Examples of ordinary and necessary expenses include the following:

Employer-reimbursed expenses typically fall into one of these categories:

If an employee purchases supplies for business purposes, such as office supplies, the employer can reimburse the expenses at cost.

According to the IRS, travel expenses qualify as ordinary and necessary when an employee must travel to perform their job. Employees may also be reimbursed for using their personal vehicles for business purposes. The IRS sets the standard mileage rate for business-related vehicle use, but commuting from home to work is not typically reimbursable. IRS Publication 15-B lists the standard mileage rates that cover driving expenses.

Transportation expenses are separate from travel expenses that the employee incurs while traveling away from their home area. Employers may reimburse transportation expenses when the employee travels to a temporary workstation under the following conditions:

Employers can reimburse employees for meal and entertainment costs they incur within their tax home if those expenses have a clear business purpose. Employees can be reimbursed for 100 percent of meal and entertainment costs, but employers can deduct only 50 percent of the cost.

You may reimburse employees with a fixed allowance, such as per diem for travel days or miles driven. Under this arrangement, the employee has sufficiently accounted for their expenses as long as the reimbursement rates are in line with government-established rates. Details of the government per diem rates for meals and accommodations can be found on the United States General Services Administration website.

Corporate gift-giving is common in some industries. If your employees purchase client gifts as part of doing business, you can reimburse them for the cost of those gifts. The IRS allows businesses to deduct a maximum of $25 per recipient per year for business gifts. If an item given to a client could be considered either a gift or entertainment, the IRS generally classifies it as entertainment.

Many employers also have to deal with additional reimbursement categories, including nontaxable reimbursements, fringe benefits and home office reimbursements.

Many employers reimburse the following expenses on a tax-free basis:

Each of these nontaxable reimbursements falls into its own category with specific guidelines on taxability.

Many employers include fringe benefits as part of a broader employee benefits package. According to the IRS Employer’s Tax Guide to Fringe Benefits (Publication 15-B), a fringe benefit is “a form of pay for the performance of services.” Therefore, most fringe benefits are taxable.

Even if a third party facilitates the benefit, such as a gym providing workout equipment and classes for your wellness program, the employer pays to provide it. The employee receives the fringe benefit package in exchange for providing their services to the employer, even if another person receives the benefit without performing services in exchange for money, such as if the employee’s spouse uses the gym membership.

Examples of fringe benefits include the following:

While many fringe benefits are taxable — subject to federal income tax, Social Security tax, Medicare tax and FUTA tax — the taxable portion may be reduced by amounts legally excluded from compensation or covered by the recipient.

Employers can issue work-from-home reimbursements to cover some of the expenses employees incur while working remotely. “Remote work has made reimbursement policies even more important,” Andreani noted. “If you work from home and buy a new desk or pay higher utility bills, some companies might reimburse these costs, but it’s not guaranteed. Always check your company’s policy before making purchases.”

A remote work reimbursement may cover the following:

Andreani emphasized that state laws and individual employer policies will affect remote work reimbursements. “There’s no universal rule and reimbursement for remote work expenses often varies by state or company,” Andreani explained. “For instance, California requires employers to reimburse necessary costs, but most states don’t.”

Properly recording employee expenses and reimbursements is crucial. Luckily, the best accounting software can help you record, report and reimburse expenses efficiently while ensuring compliance with tax regulations.

Both employers and employees play a role in keeping the expense reimbursement process smooth, consistent and compliant.

“For employees, the most important thing is to save receipts and follow the company’s rules when submitting expenses,” Andreani advised. “For employers, it’s about being consistent, fair and fast. A well-handled reimbursement process not only ensures compliance but also builds trust and keeps everyone focused on their work — not chasing payments.”

Consider the following four steps to establish and implement your employee expense reimbursement process.

Create an expense reimbursement report form using your accounting software or a spreadsheet. Distribute it to all employees who need to be reimbursed for business expenses. The form should include line items for the following:

Your expense reimbursement policies must be clear and include the following:

“For employers, having a clear and simple reimbursement policy is critical,” Andreani advised. “It should list what’s covered, how to submit expenses and when employees can expect reimbursement.”

After submission, an employee’s submitted expense report must be approved or denied by a designated party. This person may be the employee’s direct supervisor, a department head, an executive or a member of your accounting and finance team.

Kibbel emphasized the importance of open communication between the expense approver and the employee. “Employees need to know what’s covered, how to submit claims and what documentation is required,” Kibbel said. “Many businesses use expense management software to simplify submissions and approvals. Regardless of the method, accurate records are essential for compliance and audits.”

The designated approver should inform employees of any denied expenses and the reasons for denial. Approved expense reports should then be passed along to accounts payable for payment.

It’s essential to compensate your employees for approved expenditures promptly. Employers generally reimburse employees in one of two ways:

Paycheck record-keeping laws require businesses to maintain records of reimbursements, so ensure compliance.

Amanda Clark contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.