A business savings account is a deposit account designed to hold funds your business doesn’t need for everyday transactions. It functions similarly to a personal savings account — you deposit money, it earns interest and you withdraw it when you need it. The difference is, a business savings account is registered under your business entity rather than your personal name, and it requires business formation documents to open.

Opening a business savings account typically requires the same documentation as a business checking account: an Employer Identification Number (EIN), articles of organization or incorporation, and a valid government-issued ID. Some banks also require an existing business checking account at the same institution before they’ll open a savings account.

Read on to learn more about business savings accounts, how they’re used and whether your business could benefit from one.

If you’re considering opening a business savings account, consider our picks for the

best business bank accounts. We spent dozens of hours researching leading business banking service providers to select the best options for your business.

How is a business savings account used?

A business savings account is most valuable when it’s tied to specific purposes rather than used as a catch-all holding tank. Here are the three most common and practical applications.

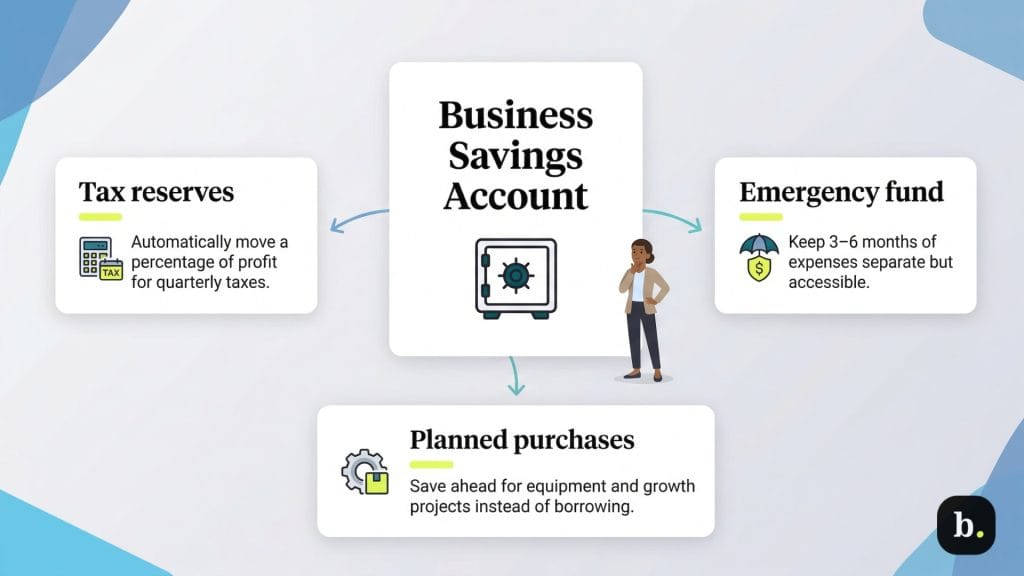

Tax reserves

For many small business owners, estimated quarterly tax payments are one of the most stressful aspects of managing cash flow. The money owed to the IRS during tax season is easy to spend on operational needs if it sits in your checking account, and you’ll find yourself scrambling when a quarterly payment comes due.

A business savings account solves this by creating a dedicated place for tax money to live. The simplest approach is a percentage-based system: every time revenue hits your checking account, transfer a fixed percentage — typically 25% to 30% of profit, depending on your tax bracket and state obligations — into your savings account. Some banks allow you to automate this transfer, removing the temptation to skip it during tight months.

When quarterly payments come due (April 15, June 15, September 15 and January 15 for most businesses), the money is already set aside and ready. You’re not pulling from operating cash, borrowing against a credit line or deferring the payment. This single habit eliminates one of the most common cash flow problems small businesses face.

Emergency fund

Every business is vulnerable to disruption, such as a major client churning, an unexpected equipment failure, a seasonal downturn that runs longer than projected or an external event that suppresses demand. An emergency fund provides a buffer that keeps your business operational while you adjust.

The standard recommendation is to maintain three to six months of operating expenses in reserve. That number may sound aggressive for early-stage businesses; building a full emergency fund takes time. The important thing is to start. Even one month of operating expenses sitting in a savings account provides meaningful protection against a short-term disruption, and you can build from there as cash flow allows.

The savings account is the right home for this reserve because it keeps the money accessible but separate. It’s not locked into a CD or invested in something illiquid; you can access it within a business day if you need it. Still, it’s not sitting in your checking account where it’s likely to get absorbed into daily spending.

Planned purchases and capital expenses

Not every major expense needs to be financed. If you know you’ll need to purchase new equipment in six months, hire an additional employee next quarter or invest in a buildout for a new location, a savings account gives you a structured way to accumulate those funds incrementally rather than taking on business debt or depleting your operating cash in a single hit.

This is particularly useful for businesses that want to avoid interest payments on equipment loans or lines of credit. Saving toward a known expense and paying for it outright may cost you the time value of money, but for many small businesses, the simplicity and certainty of paying cash and avoiding the obligation of monthly loan payments is worth the tradeoff.

The key distinction between a business savings account and a business checking account is purpose. A checking account is built for movement: payroll, vendor payments, invoices, and daily expenses flow in and out continuously. A savings account is built for stillness: it holds money you've deliberately set aside for a future need, earning interest while it waits.

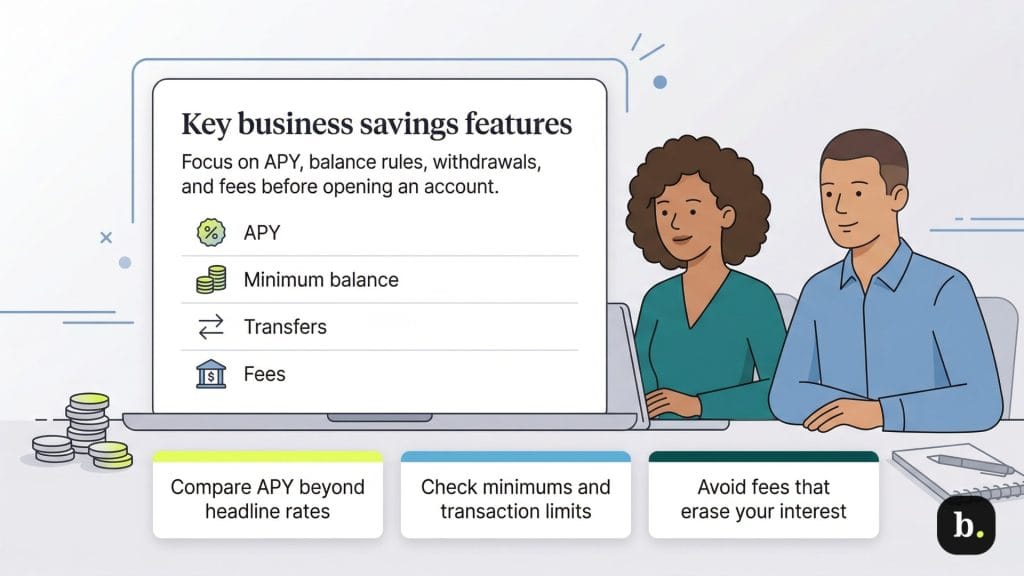

Key business savings account features to compare

When choosing a business savings account, consider the following criteria and weigh what each service provider offers against each other.

APY

The annual percentage yield on your savings account determines how much your deposits earn, and the range between banks is dramatic. As of early 2026, the national average savings rate sits around 0.39% APY, effectively a rounding error on most small business balances. But high-yield business savings accounts, particularly those offered by online banks and fintechs, are currently offering rates between roughly 3.5% and 4.5% APY. Some promotional offers push even higher, though those elevated rates are often temporary or require specific balance thresholds.

The difference matters more than most business owners realize. On a $50,000 balance, the gap between 0.39% APY and 4% APY is the difference between earning roughly $195 and $2,000 in a year. That’s essentially free money for keeping your cash in a better account.

Pay attention to rate tiers. Some banks advertise a competitive headline rate that only applies to balances above a certain threshold, like $10,000, $25,000 or even higher. If your typical balance falls below that tier, you may be earning significantly less than the advertised rate. Also note whether the rate is variable or fixed. Most savings account rates are variable, meaning they can change at any time based on market conditions and the bank’s own decisions.

Minimum balance requirements

Some business savings accounts require a minimum balance to earn interest, to earn the top-tier APY or to avoid monthly fees. These minimums range widely, from zero at many online banks to $5,000 or $25,000 at traditional institutions.

Before opening an account, honestly evaluate whether you can consistently maintain the required minimum. An account with a 2.5% APY and a $25,000 minimum balance requirement isn’t a good deal if your typical savings balance is $8,000 and you’re paying a monthly fee for falling short. Many online banks have eliminated minimum balance requirements entirely, making them a strong option for businesses with smaller or fluctuating reserves.

Withdrawal and transfer rules

Historically, the Federal Reserve’s Regulation D limited certain types of savings account withdrawals — online transfers, ACH payments, and automatic transactions — to six per month. In April 2020, the Fed eliminated that federal requirement, and it has confirmed the change is permanent.

However, many banks have kept their own withdrawal caps in place voluntarily. Some still enforce the old six-transaction limit and charge fees for exceeding it, not because they’re required to but because it aligns with their business model. Others, particularly online banks, have removed restrictions entirely.

Before opening a business savings account, confirm your bank’s specific withdrawal policy. If you anticipate needing to transfer funds more than a handful of times per month, choose a bank that has eliminated transaction limits or consider a money market account for greater flexibility.

Fees

The most common fees associated with business savings accounts are monthly maintenance charges, excess withdrawal penalties, and below-minimum-balance fees. At traditional banks, monthly maintenance fees typically range from $5 to $15, often waivable by maintaining a minimum balance. Excess withdrawal fees, charged when you exceed the bank’s transaction cap, can range from $5 to $25 per additional transaction.

Online banks have largely disrupted this model. Many offer business savings accounts with no monthly fees, no minimum balance requirements, and no withdrawal penalties. If fees are eating into the interest you’re earning, it’s worth shopping around — particularly among digital-first institutions that operate with lower overhead costs.

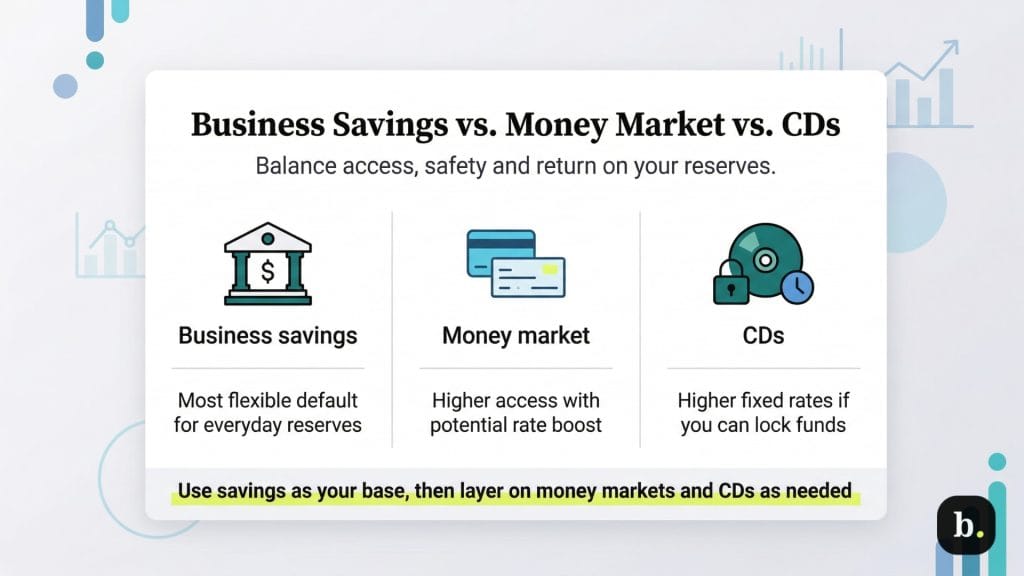

Business savings vs. money market vs. CDs

A business savings account isn’t the only place to park reserve cash, and for some businesses, a different account type may be a better fit.

Money market accounts

These accounts function as a hybrid between savings and checking. They typically offer interest rates comparable to or slightly higher than savings accounts, and they often include check-writing privileges and debit card access, features that savings accounts generally lack. The tradeoff is higher minimum balance requirements, often $10,000 or more to earn the best rate or avoid fees. If you need occasional direct access to your reserve funds (writing a check for a large purchase, for example), a money market account offers more flexibility than a standard savings account.

Certificates of deposit (CDs)

CDs offer a fixed interest rate in exchange for locking your funds for a set period — typically three months to five years. CD rates are often higher than savings account rates, especially for longer terms, but the tradeoff is liquidity: withdrawing funds before the term ends triggers an early withdrawal penalty. CDs make sense for money you won’t need within a specific, predictable timeframe — a buildout planned for nine months from now, for example. They don’t make sense for emergency funds or tax reserves, where you need access on short notice.

For most small businesses, a savings account is the most flexible default. It earns meaningful interest (provided you choose a competitive rate), keeps your reserves accessible, and requires the least management. Money market accounts and CDs are useful supplements for specific situations, but the savings account covers the broadest set of needs with the fewest constraints.

A business savings account won't transform your finances on its own, but it fills an important structural role: it separates the money you're spending from the money you're saving, earns interest on cash that would otherwise sit idle, and creates discipline around tax obligations, emergency reserves, and planned expenses. The account itself is simple — the value comes from using it intentionally, funding it consistently, and choosing a bank that offers competitive rates without burying you in fees.