Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Smarter Bookkeeping with AI-Powered Reconciliation

Manual bookkeeping is a hassle and leaves a lot of room for human error. Make your bank reconciliations simpler and more accurate with AI-powered automation features within QuickBooks.

Written by: Miranda Fraraccio, Senior WriterUpdated Jan 02, 2026

Editor Verified

Editor Verified

A business.com editor verified this analysis to ensure it meets our standards for accuracy, expertise and integrity.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Manual bookkeeping and reconciliation can be a significant drain on time and resources. With AI-powered bookkeeping tools, these tasks can now be automated, improving reconciliation speed and accuracy without adding strain to the process. Below, we’ll explore the account reconciliation process and how AI is reshaping it for SMBs and accountants.

This article is sponsored by Intuit.

What is account reconciliation?

Account reconciliation is the process of checking your bank receipts and logged transactions against your business’s financial records. To reconcile a business bank account, you gather receipts, credit card and bank statements, invoices and accounts payable and receivable reports, then compare them to your bookkeeping records.

If reconciliation is done manually, human errors can result in incorrectly logged transactions or overlooked faulty transactions, requiring extensive resources to address and correct. Manual reconciliation also only gives you a snapshot of your company’s finances at that specific point in time. The lag can lead to misguided financial decisions and lost opportunities.

Why reconciliation matters for SMBs

Regularly reconciling your accounts is critical for maintaining accurate business finances and effectively managing your financial health. The process helps you identify and address issues before they escalate into bigger problems. Without it, you could be operating using faulty data, leading toforecasting errors, inventory problems or accounting mistakes.

On a larger scale, accurate reconciliations support audit readiness by ensuring records are correct and traceable, helping you avoid potential penalties or legal troubles. When your documentation is consistently organized and easily accessible, you’re better prepared for audits, tax filings and any financial reviews that come your way.

Still, many SMBs put off reconciliation because the manual process is inherently time-consuming, requiring extensive data entry, document organization and audit trail maintenance. For time-strapped business owners, that can make regulatory tracking difficult.

Did You Know?

SMBs are required to stay up-to-date on changing laws and tax regulations that may impact their operations. AI-powered tools can make it easier for new leaders to remain compliant as they grow.

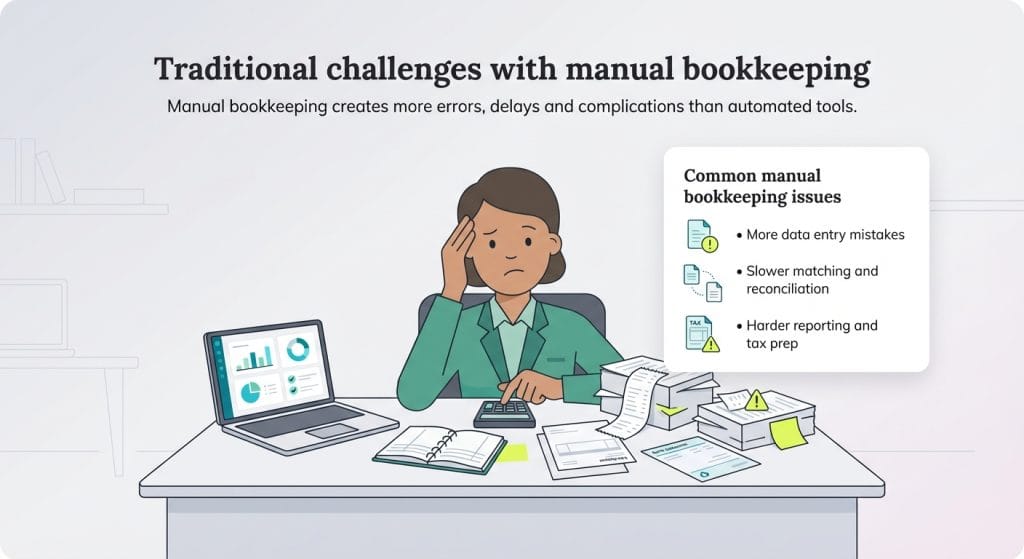

Traditional challenges with manual bookkeeping

With the advent of accounting software, bookkeeping is now less labor intensive. This is a positive shift, since manual bookkeeping processes pose challenges for businesses, including:

Data entry errors. When input manually, a simple slip of the hand could ruin your data’s accuracy — and if you don’t catch your mistake, you could wind up with false, unusable data.

Difficulty matching transactions across multiple accounts and bank statements. Manual bookkeeping requires you to collect and cross-check all your transactions, which necessitates extensive organization and staffing. Losing your receipts or documentation could impact your process.

Handling exceptions and timing differences. With manual bookkeeping, you don’t get a real-time view of your finances, which can lead to discrepancies between your recorded and actual transactions. Any exceptions or delays — such as late entries or uncleared payments — must be logged and managed to ensure accuracy.

Inconsistent reporting standards and tax preparation inefficiencies. Adhering to reporting standards can be more challenging for businesses with manual processes, which increases the likelihood of financial discrepancies. As a result, tax document preparation is more complicated.

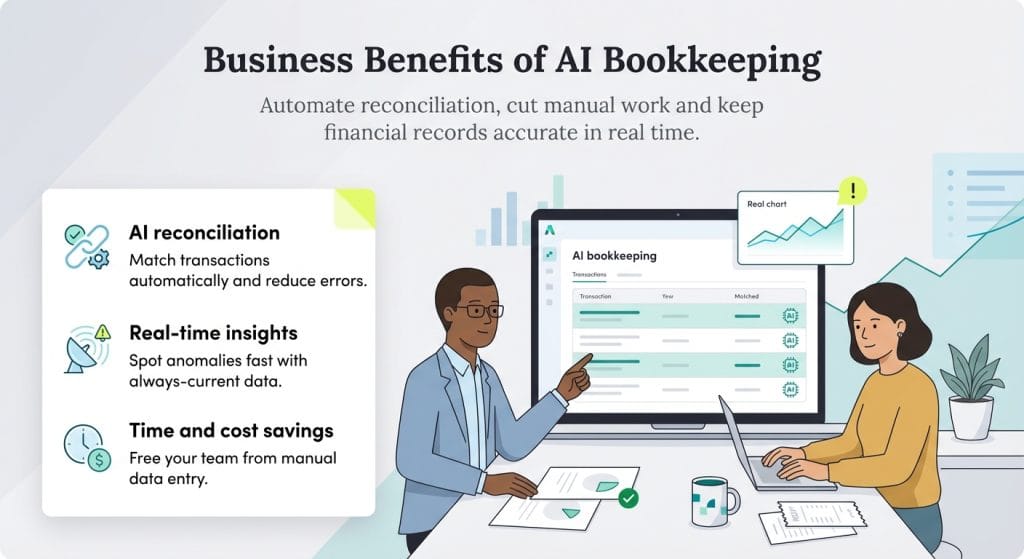

Automated matching of records and transactions. Once a manual process, AI accelerates reconciliation by automatically verifying records, flagging issues to ensure accuracy and logging each transaction.

Intelligent transaction categorization. Logged receipts can be automatically categorized using AI, eliminating repetitive tasks for employees while ensuring the company’s important financial documentation is stored correctly and remains accessible in a templated, simplified format.

Real-time anomaly detection and quality control. AI can objectively analyze data to uncover patterns and issues users may have overlooked. It also scans data in real time, rather than just providing a single financial snapshot. The process provides companies with the most up-to-date information for making accurate predictions and informed decisions.

Time and cost savings. Unsurprisingly, a major benefit of AI bookkeeping solutions is the cost savings they offer. However, beyond the cash savings is the potential for monthly hours saved, as you’re not devoting team efforts to manually inputting data and handling repetitive tasks. Instead, your team can focus on more important — and more profitable — tasks to support your business.

Improved audit readiness and document organization. AI agents can log all your transactions and records, ensuring your documents are compliant and providing an up-to-date view of your financial health. This information, organized and accessible in one location, can be referenced and pulled at any time, ensuring you’re ready to provide documentation in the event of an audit.

Scalability for businesses experiencing growth. While manual bookkeeping may be effective in the early stages, it’s generally unsustainable as your business grows and transaction volumes increase. Implementing AI solutions allows you to scale while maintaining accurate records, helping SMBs improve accounting without overburdening their teams.

Continuous learning based on user corrections and data patterns. The more feedback you provide to AI, the better it can understand your company and offer support tailored to your needs.

Example: Intuit’s AI-powered reconciliation

Tools such as Intuit’s AI agents, which are available to users with the Essentials plan and above, can quickly flag discrepancies and suggest matches. This tool helps reduce time spent on reconciliation and improve financial accuracy.

For instance, Intuit’s advanced automation technology includes the following helpful features:

Feature

Details

Bank feed integration

The tool can recognize your business’s typical payment patterns to identify issues, forecast cash flow and automate processes such as invoice reminders and transaction posting.

Automated transaction matching

QuickBooks’ AI-powered banking page automatically monitors and matches your transactions with invoices you’ve sent to help avoid duplicate entries and link related transactions. The process helps speed up the reconciliation process and keeps your financial records accurate and up-to-date.

Exception flagging and resolution

Sometimes, adjustments are necessary during the reconciliation process. With Intuit, users can view flagged transactions, along with AI-powered explanations and suggestions for resolution, and determine whether adjustments are needed.

Easy setup and real-time balance updates

Setting up your business with Intuit’s AI solutions is easy and allows you to dive deeper into your business’s financial health with real-time balance updates.

Tip

For optimal performance, provide feedback to Intuit's AI agents. With machine learning, these agents continuously improve based on user feedback, helping SMBs and accountants keep their books up to date with less effort.

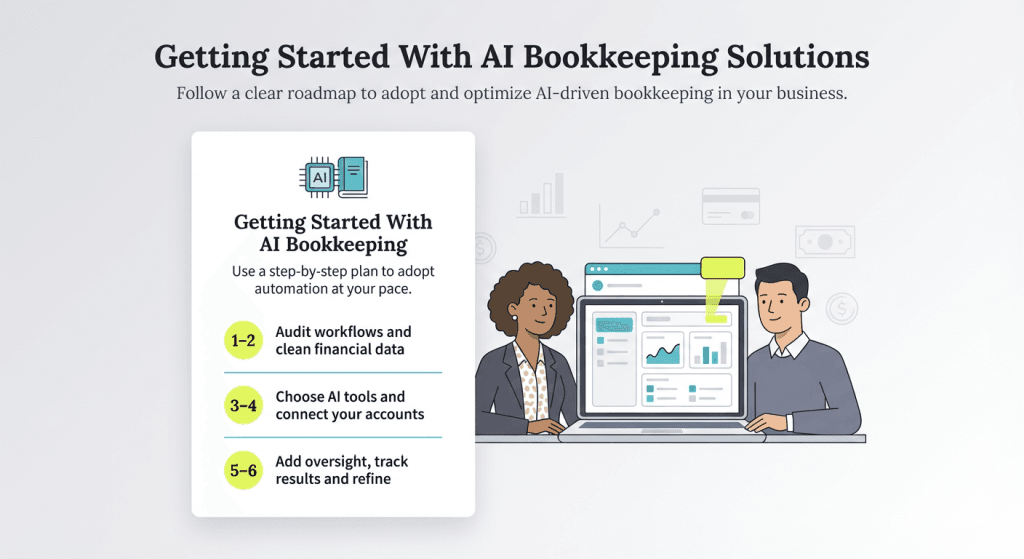

Getting started with AI bookkeeping solutions

Follow these steps to adopt AI bookkeeping technology and integrate it into your workflow.

1. Assess and document current reconciliation workflows.

Before adopting a tool, evaluate your company’s current bookkeeping processes, analyze what works and what doesn’t and document your workflows. Identify bottlenecks and areas for improvement to streamline your workflows.

Start by tracking how much time your team spends on specific tasks like data entry, transaction matching and month-end reconciliation. Document pain points such as frequent errors, missing receipts or delays in closing your books. Understanding your baseline will help you measure the impact of AI automation and identify which features will provide the most value for your business.

2. Prepare and clean your financial data.

AI tools learn from your existing data, so the quality of your historical records directly impacts how quickly and accurately the system can help you. Review your past transactions to ensure they’re properly categorized and eliminate duplicate entries or uncategorized items.

Standardize your vendor names, update your chart of accounts and resolve any outstanding reconciliation discrepancies. This preparation work may seem tedious, but it significantly improves the AI’s ability to recognize patterns and make accurate suggestions from day one. If your records need significant cleanup, consider working with a bookkeeper to get your data audit-ready before implementation.

3. Identify requirements and select appropriate AI solutions.

Determine what your business needs from a bookkeeping tool, such as scalability, ease of use and advanced features for tech-savvy users. Then, explore your options. Solutions like Intuit’s AI Accounting Agent offer a comprehensive solution suitable for a wide range of businesses.

Consider factors like your transaction volume, number of bank accounts, integration needs with other software and whether you need multi-user access. If you work with an accountant, involve them in the selection process to ensure the tool supports collaboration. Review what plan tier you’ll need to access AI features — for example, QuickBooks’ Accounting Agent is available starting with the Essentials plan.

4. Set up integrations and train your team.

Once you’ve selected your AI bookkeeping solution, connect your bank accounts, credit cards and any other relevant financial tools to enable automated data flow. Take time to configure your preferences, such as approval thresholds and notification settings, so the AI works according to your business processes.

Invest in training for anyone who will use the system. While AI tools are designed to be intuitive, understanding how to review AI suggestions, provide feedback and handle exceptions will help your team use the technology effectively. Many solutions offer guided setup assistance and tutorials to help you get started with confidence.

5. Establish feedback loops and oversight protocols.

While your AI solution can manage many repetitive tasks, ensure you have ongoing human oversight to maintain accuracy, catch context-specific errors and guide the system’s learning. Designate who will review flagged transactions, verify categorizations and provide corrections when needed.

Set up a regular review schedule — weekly for the first month, then monthly once the system is well-trained. The feedback you provide helps the AI learn your business’s unique patterns and improves its accuracy over time. Document any recurring issues or categories that need special attention so you can refine your processes.

6. Monitor performance and optimize over time.

Track key metrics like time saved, error reduction and reconciliation speed to measure the impact of your AI bookkeeping solution. Most businesses see improvements within the first 30 to 60 days as the AI learns their transaction patterns.

As your business grows and changes, revisit your workflows periodically to ensure your AI tools are still meeting your needs. You may discover opportunities to automate additional processes or adjust your configurations for better results. Stay informed about new features and updates from your provider, as AI capabilities continue to evolve rapidly.

Did You Know?

Transitioning to an AI bookkeeping system is easy with Intuit’s Accounting Agent. From setup to full integration, the process is simple. Plus, the tool learns from existing business data and workflows, helping it to understand your business from the outset and provide solutions that work for you.

Transitioning to an AI bookkeeping system is easy with Intuit’s Accounting Agent. From setup to full integration, the process is simple. Plus, the tool learns from existing business data and workflows, helping it to understand your business from the outset and provide solutions that work for you.

Did you find this content helpful?

Thank you for your feedback!

Share Article:

Written by: Miranda Fraraccio, Senior Writer

Miranda Fraraccio is a versatile small business expert who often shares her insights and guidance through the U.S. Chamber of Commerce. She leads small business owners and other business leaders to the resources necessary for their organizations to thrive, and breaks down important business concepts into actionable guides.

At business.com, Fraraccio primarily covers a range of HR topics, including management theories, onboarding and benefits, employee development and more.

Fraraccio, who studied communication at the University of Rhode Island, is also well-versed in other business areas, including funding, sales, marketing and social media management. She regularly spotlights businesses across the country that are making a difference in their communities.