Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

The True Cost of Business Financing: How to Compare Loans Beyond the Interest Rate

There’s more to the cost of business loans than just the interest rate. Here are the other factors you need to consider before accepting funding.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

This article is sponsored by Big Think Capital.

When small business owners shop for financing, the first number they compare is almost always the interest rate. It makes intuitive sense that a lower rate should mean a cheaper loan. But, in practice, the interest rate is only one component of what a loan actually costs, and in many cases it is not even the most important one.

Origination fees, factor rates, repayment frequency, prepayment penalties and other structural features can dramatically change the total cost of capital. Two loans with nearly identical headline rates can differ by thousands of dollars in total repayment, depending on how they are structured. The result is that business owners who compare loans on rate alone routinely choose the more expensive option without realizing it.

This article breaks down the components that determine the true cost of business financing and walks through side-by-side examples that show how the math actually works. The goal is simple: to give you the tools to evaluate any loan offer on its real terms, not just the rate on the cover sheet.

Why interest rate alone is misleading

Interest rate is a useful starting point, but it does not account for fees, repayment structure or term length, all of which affect what you actually pay. A loan at 10% APR repaid monthly over three years is a fundamentally different financial commitment than a loan at 10% APR repaid daily over 12 months, even though the stated rate is identical.

Part of the confusion stems from the fact that not all rates are calculated the same way. Traditional term loans and SBA loans are typically quoted in APR, which annualizes the total borrowing cost including certain fees.

Many alternative financing products, particularly merchant cash advances, use factor rates instead, a flat multiplier applied to the amount borrowed. A factor rate of 1.3 means you repay $1.30 for every $1.00 borrowed, regardless of how quickly or slowly you repay. That may sound straightforward, but it obscures the annualized cost, which can be significantly higher than a comparable APR figure.

The distinction matters because business owners comparing offers across different product types often find themselves looking at an APR on one term sheet and a factor rate on another. Without converting them to a common measure, a direct comparison is not possible.

The full cost checklist: What to look for in any loan offer

Before signing any financing agreement, business owners should evaluate the following cost components. Not every loan will include all of them, but knowing what to look for prevents surprises after funding.

Origination fees

These are charged upfront, either as a flat dollar amount or a percentage of the loan. In some cases, origination fees are deducted directly from loan proceeds, meaning you receive less than the stated loan amount but repay the full balance. A $100,000 loan with a 3% origination fee nets you $97,000, but your repayment schedule is based on $100,000. That effective cost should be factored into any comparison.

Factor rates vs. APR

Factor rates express total repayment cost as a simple multiplier. A $50,000 advance at a factor rate of 1.35 means you repay $67,500 total. To compare this against a traditional loan, you need to convert it to an approximate APR, which depends on the repayment term. Over six months, a 1.35 factor rate translates to a much higher annualized cost than over 18 months. Any lender that refuses to provide an APR equivalent should raise a red flag.

Prepayment penalties

Some financing products charge a fee for early repayment, which may seem counterintuitive. The logic from the lender’s perspective is that early repayment reduces their expected interest income. For the borrower, this means paying off a loan ahead of schedule does not necessarily save money. Always ask whether the total repayment amount decreases if you pay early, and by how much.

Draw fees and maintenance fees

Lines of credit often carry costs beyond the interest charged on drawn funds. Draw fees apply each time you access funds, and monthly or annual maintenance fees may apply whether you draw or not. These costs are easy to overlook during the application process but can add up substantially over the life of a revolving credit facility.

Daily vs. monthly repayment

Repayment frequency directly affects cash flow. Daily ACH debits, common with merchant cash advances and some short-term loans, pull funds from your account every business day. Even if the total repayment amount is the same as a monthly-payment loan, the operational impact is different: daily pulls reduce your available working capital continuously and can create cash flow strain during slow periods. Beyond the cash flow impact, daily repayment effectively increases the annualized cost of capital because you are returning funds to the lender faster, reducing the time you have to use the money.

Collateral and personal guarantees

These are not direct dollar costs, but they are risk costs that should be weighed. A loan requiring a blanket lien on business assets or a personal guarantee exposes you to losses beyond the loan itself if the business cannot repay. Two otherwise identical loans may look very different when one requires a personal guarantee and the other does not.

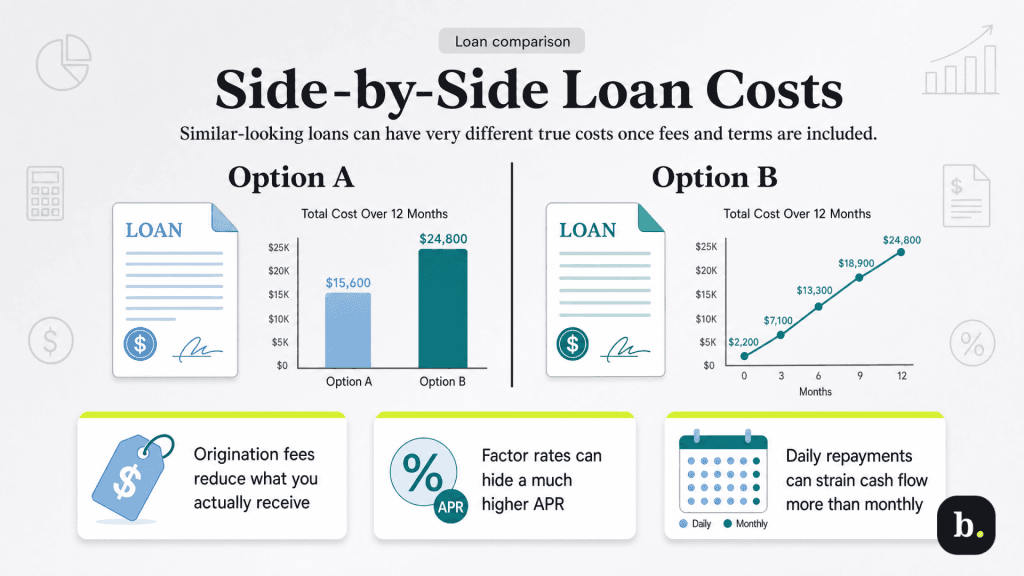

Side-by-side: How two similar-looking loans can cost very different amounts

The following examples illustrate how structural differences change the true cost of financing, even when headline numbers look comparable.

Example A: The Hidden Impact of Origination Fees

Consider two term loans for $100,000 over 24 months:

Loan A

Loan B

Stated APR

9%

11%

Origination Fee

3% ($3,000)

None

Net Proceeds

$97,000

$100,000

Monthly Payment

~$4,568

~$4,663

Total Repaid

~$109,632

~$111,912

Total Cost of Capital

~$12,632

~$11,912

Loan A

Loan B

Stated APR

9%

11%

Origination Fee

3% ($3,000)

None

Net Proceeds

$97,000

$100,000

Monthly Payment

~$4,568

~$4,663

Total Repaid

~$109,632

~$111,912

Total Cost of Capital

~$12,632

~$11,912

Loan A has the lower rate, but after accounting for the origination fee, which reduces the actual proceeds to $97,000, the total cost of borrowing is higher. The borrower pays approximately $12,632 in total financing costs for Loan A versus $11,912 for Loan B. The loan that looked cheaper on paper is actually more expensive in practice, and the borrower receives less cash upfront.

Example B: Factor Rate vs. APR

A business owner is comparing a merchant cash advance with a short-term loan. Both provide $50,000 in funding:

MCA

Short-Term Loan

Rate

1.35 factor rate

28% APR

Repayment Term

~8 months (estimated)

12 months

Total Repaid

$67,500

~$57,903

Total Cost of Capital

$17,500

~$7,903

Approx. Effective APR

~90%+

28%

The factor rate of 1.35 sounds modest compared to 28% APR, but they are measuring entirely different things. The factor rate is a flat multiplier on the total advance. When annualized over the expected eight-month repayment period, the effective APR of the MCA exceeds 90% (dependent upon the frequency of repayment). The short-term loan at 28% APR, despite its seemingly high rate, costs less than half as much in total financing charges.

This is arguably the most common comparison trap in small business financing. Factor rates are not inherently predatory, but they require conversion to understand their true cost. Any business owner considering a factor-rate product should ask the lender to provide the approximate APR equivalent.

Example C: Daily vs. Monthly Repayment

Two loans offer $75,000 at similar total repayment amounts over 12 months, but with different payment schedules:

Daily Repayment

Monthly Repayment

Loan Amount

$75,000

$75,000

Payment

~$365/business day

~$7,266/month

Total Repaid

~$91,250

~$87,192

Cost of Capital

~$16,250

~$12,192

Even setting aside the total cost difference, the daily repayment loan creates a fundamentally different cash flow experience. Approximately $365 leaves the business account every business day, reducing the operating cushion that most small businesses rely on to manage day-to-day expenses. During a slow week, those daily debits continue regardless of revenue, which can force a business to draw on other reserves or take on additional financing to cover operating costs, a cycle that compounds the cost of borrowing.

The monthly repayment loan, by contrast, gives the borrower predictable, once-a-month obligations that are easier to plan around and absorb within normal cash flow cycles.

How to ask the right questions before you sign

The math matters, but you do not need a finance degree to protect yourself. Before signing any loan agreement, ask the following questions. A reputable lender will answer all of them clearly.

What is the total repayment amount? Not the rate, not the monthly payment, but the total dollar amount you will repay over the life of the loan. This single number cuts through the complexity of rates, fees and terms.

What is the APR? If the product uses a factor rate, ask the lender to provide an APR equivalent. If they cannot or will not, treat that as a signal to proceed with caution.

Is there a prepayment penalty? If so, under what conditions, and does the total repayment amount decrease if you pay early? Some products require you to repay the full factor-rate amount regardless of when you pay, meaning early repayment saves you nothing.

Are payments daily, weekly or monthly? Understand both the dollar amount of each payment and the frequency. Model it against your actual cash flow to determine whether the schedule is sustainable during your slowest periods.

What fees are deducted from proceeds vs. charged separately? Fees deducted from proceeds reduce the actual capital you receive. If you need $100,000 and fees reduce your proceeds to $95,000, you may need to borrow more, which increases total cost.

What collateral or personal guarantees are required? Understand what is at stake beyond the loan balance itself.

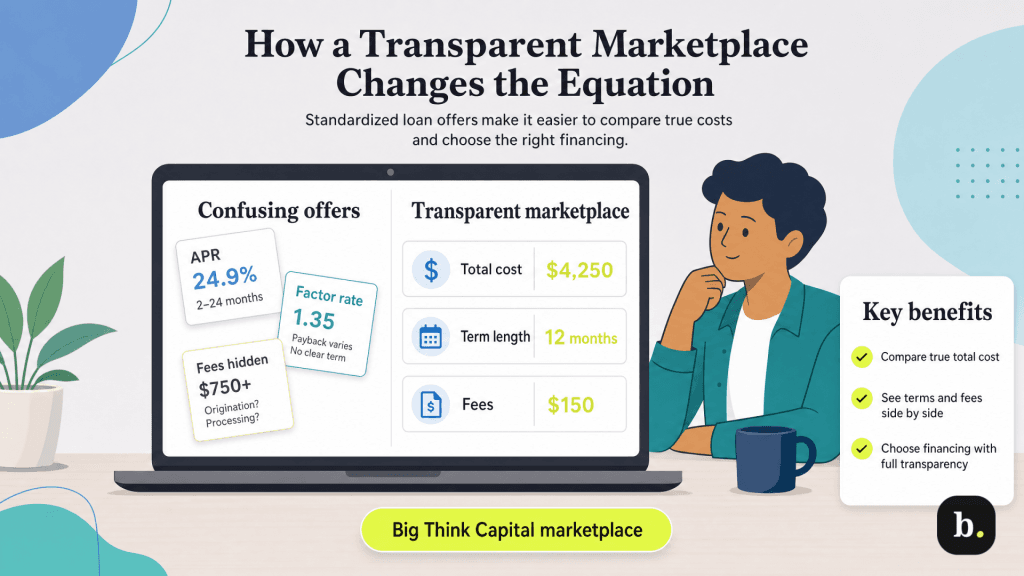

How a transparent marketplace changes the equation

One of the practical challenges of comparing financing options is that each lender presents their offer differently. Some quote APR, others use factor rates. Some bury fees in fine print, while others deduct them from proceeds without clear disclosure. Business owners end up comparing apples to oranges, and the loan that markets itself most aggressively often wins out over the loan that is genuinely the best deal.

This is where marketplace-model lenders offer a structural advantage. Rather than negotiating with a single lender and hoping the offer is competitive, marketplaces allow business owners to review multiple offers in a standardized format, making it possible to compare total cost, repayment terms and fee structures across products.

Big Think Capital operates as this type of marketplace, connecting business owners with a range of financing options, including SBA loans, term loans, lines of credit, equipment financing and working capital, and presenting them with the transparency needed to make an informed comparison. Their approach is built around showing borrowers the full cost picture rather than leading with headline rates. For business owners who want to apply the framework outlined in this article to real offers, a marketplace that prioritizes transparency over volume is the right starting point.

There’s more to business loan costs than interest rates

Interest rate is a useful data point, but it is a poor decision-making tool when used in isolation. The true cost of business financing is determined by the interplay of fees, rate structure, repayment frequency, term length, and penalty provisions. Two loans that look similar on paper can differ by thousands of dollars in actual cost and produce very different cash flow experiences.

Before signing your next loan agreement, run the total repayment math yourself. Ask every question on the checklist above. And if a lender cannot clearly explain the total cost of their product, that is the most important piece of information they have given you.

Adam Uzialko, the accomplished senior editor at Business News Daily, brings a wealth of experience that extends beyond traditional writing and editing roles. With a robust background as co-founder and managing editor of a digital marketing venture, his insights are steeped in the practicalities of small business management.

At business.com, Adam contributes to our digital marketing coverage, providing guidance on everything from measuring campaign ROI to conducting a marketing analysis to using retargeting to boost conversions.

Since 2015, Adam has also meticulously evaluated a myriad of small business solutions, including document management services and email and text message marketing software. His approach is hands-on; he not only tests the products firsthand but also engages in user interviews and direct dialogues with the companies behind them. Adam's expertise spans content strategy, editorial direction and adept team management, ensuring that his work resonates with entrepreneurs navigating the dynamic landscape of online commerce.