Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Consumers expect to pay with credit and debit cards, but finding a credit card processor in certain industries can be challenging. Here are the pros and cons of a high-risk merchant account.

Businesses in what are considered “high-risk” industries can have a hard time finding a credit card processor or merchant account provider to handle their payments — and when they do find one, they may be subject to stringent requirements or have to pay higher fees.

We’ll break down which industries are considered high-risk, explain why that matters and walk you through the pros and cons of working with a high-risk merchant account provider.

A high-risk merchant account is a type of payment processing account assigned to businesses that are more likely to experience chargebacks, refunds or credit card fraud or operate in industries considered unstable or legally complex. These accounts typically come with higher fees and stricter contract terms because they pose more liability for credit card processors and banks.

Searching for a credit card processor and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Businesses classified as high-risk may be required to maintain a rolling reserve — a portion of your credit card sales that the processor temporarily holds as a buffer against potential disputes or chargebacks.

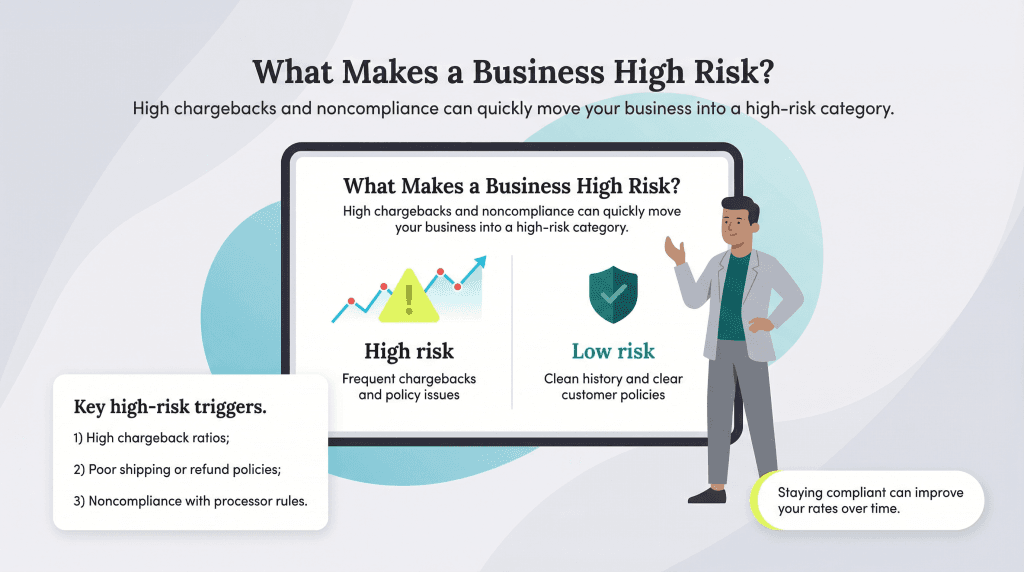

Factors that may classify a business or its industry as “high risk” include:

Businesses commonly considered high risk by most lenders include:

The best credit card processors abide by specific classifications for high-risk merchants. Here’s an overview of what may land you in the high-risk credit card processing category as opposed to the low-risk one:

High risk | Low risk |

|---|---|

$20,000 or more in monthly transactions | Less than $20,000 in monthly sales |

Average transaction of $500 or more | Average transaction of less than $500 |

High-risk industry (forex, gambling, travel) | Low-risk industry, such as clothing, home goods or books) |

Excessive chargebacks and disputes | Low chargeback ratio (less than 0.9 percent of total transactions) |

Accepts multiple currencies as payment | Only accepts one currency as payment |

Offers recurring payment options (subscriptions) | Conducts single transactions only (no subscriptions) |

Conducts business internationally | Conducts business only in the United States |

While this table serves as a general guide, whether your business is categorized as high risk or low risk is ultimately up to the credit card processing company.

Kyle Hall, CEO of PayKings, noted that chargebacks are a major red flag.

“Any business that has high chargeback ratios is also deemed high-risk. This could be due to poor shipping policies, bad product quality or a difficult refund process,” Hall said.

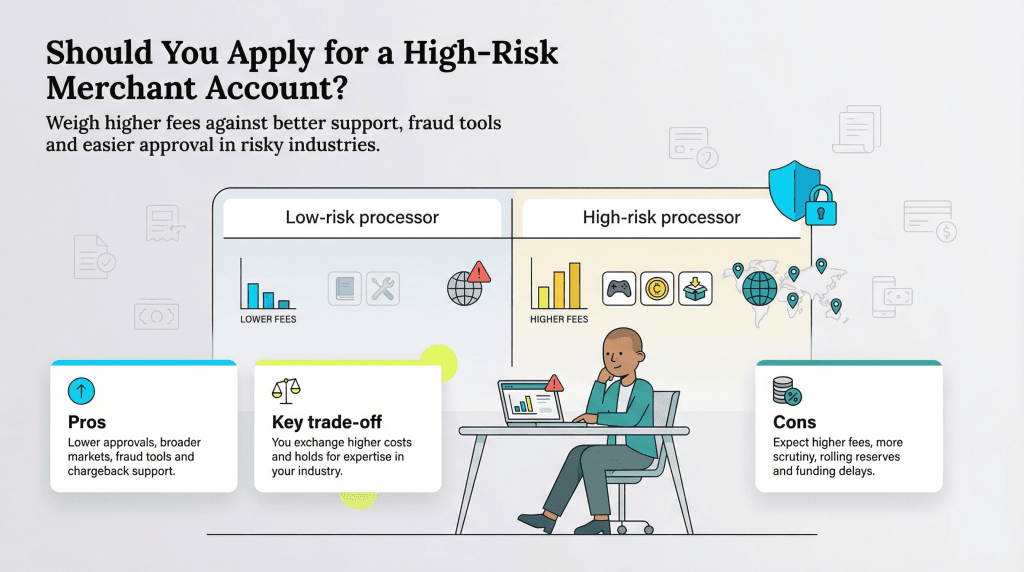

If you’re a merchant operating in a high-risk industry, you have two primary options for working with a payment processor:

It may be difficult to find a credit card processor willing to approve your account. Even after that, you’ll likely face higher processing fees, rolling reserves and stricter contract terms. On the other hand, working with a processor that specializes in high-risk industries means they understand your unique challenges and can offer support tailored to your specific business needs.

Here are a few pros and cons to consider about working with a high-risk credit card processor.

No matter which path you choose for credit card processing, the key is to shop around and find a provider with fair, transparent pricing and experience in your field. As a high-risk merchant, it’s best to be prepared for added complexity and choose a processor with experience supporting businesses like yours.