You can run a profitable business, pay your bills on time and still struggle to access financing or flexible payment terms. That’s because lenders and vendors aren’t just looking at your revenue: They’re looking at your business credit.

Business credit functions like personal credit in concept but operates on a separate infrastructure. It plays a key role in how your company accesses financing, manages cash flow and builds credibility with lenders, vendors and partners. Below, we’ll break down what business credit is, how it works and the steps you can take to build it and put your business on solid financial ground.

What is business credit?

Business credit is a measure of your company’s financial reliability, specifically, how consistently and promptly your business pays its debts, vendors and financial obligations.

Your business credit profile is tied to your Employer Identification Number (EIN) and tracked by specialized business credit bureaus, while your personal credit is tied to your Social Security number and tracked by consumer bureaus like Equifax, Experian and TransUnion. Business credit bureaus may also assign your company a business credit score or rating that lenders and vendors use to assess risk.

A strong business credit profile can benefit your company in several ways:

- Access to better financing terms: A strong profile gives you access to better terms on business loans and lines of credit, often at lower interest rates.

- Improved cash flow flexibility: It allows you to establish vendor net terms — the ability to purchase supplies or inventory now and pay 30, 60 or 90 days later — which is critical for managing cash flow in growing businesses.

- Separation of personal and business liability: It helps separate your personal liability from your business borrowing, which means that, over time, lenders and vendors can rely on your company’s track record instead of requiring a personal guarantee.

- Increased credibility: It can build credibility with partners, suppliers and potential business investors who check business credit as part of their due diligence.

Unlike personal credit, which accumulates naturally as you use credit cards, take out loans and pay bills, business credit requires intentional effort to establish. If you don’t take specific steps to build it, your business may have no credit profile at all, regardless of how long you’ve been operating or how responsibly you manage your finances.

How business credit scores work

Business credit scores aren’t universal the way personal credit scores are. Instead, multiple business credit bureaus track your company’s activity, including how you manage business debt, and each uses its own scoring model and scale. That means your business may have different scores depending on who’s evaluating it.

Here’s a closer look at who’s tracking your business credit and what factors actually influence your score.

The business credit bureaus tracking your credit

Three bureaus dominate business credit reporting, and each approaches scoring a bit differently:

- Dun & Bradstreet (D&B) — PAYDEX Score: The PAYDEX score ranges from 1 to 100 and measures how promptly your business pays its bills relative to agreed-upon terms. It’s dollar-weighted, so larger invoices carry more influence than smaller ones. A score of 80 indicates on-time payments, while 100 reflects consistent early payments. Scores below 50 signal higher risk. The PAYDEX score is based only on payment history reported by vendors and suppliers registered with D&B as trade references. In practice, that means you’ll usually need at least two trade references reporting three separate payment experiences each to generate a score.

- Experian Business — Intelliscore Plus: This score also ranges from 1 to 100, with higher scores indicating lower risk. Intelliscore Plus considers a wide range of factors — more than 800 variables — including payment history, credit utilization, outstanding balances, company size, industry risk and time in business. Scores of 76 to 100 are considered low risk, while scores below 25 indicate medium-to-high risk. In some cases, it may also factor in the business owner’s personal credit, especially for newer businesses.

- Equifax Business — Credit Risk Score: Equifax uses a different scale, ranging from 101 to 992, which can feel less familiar to business owners used to personal credit scoring. Higher scores indicate lower risk. Equifax also provides a Payment Index Score (1 to 100) that focuses on payment reliability and a Business Failure Score (1,000 to 1,880) that estimates the likelihood of business failure within the next 12 months.

Each bureau collects data independently, and not all vendors report to all three. As a result, your business credit profile may look different across bureaus, which is why it’s important to monitor each one.

Some lenders also use the

FICO Small Business Scoring Service (SBSS), a scoring model that combines your business and personal credit data. Unlike bureau scores, the SBSS ranges from 0 to 300 and is often used for loan decisions, including SBA financing.

What factors influence your business credit score

While each bureau weighs factors differently, the same core elements influence business credit scores across the board:

- Payment history: This is the most important factor. Whether you pay on time, early or late (and by how much) has the greatest impact on your scores across all major models.

- Credit utilization: Particularly important for models like Intelliscore Plus, this comes down to how much of your available credit you’re using and whether your balances are increasing or decreasing over time.

- Length of credit history: Businesses with longer track records of responsible credit use tend to be viewed more favorably than those with limited or newer credit profiles.

- Company size and industry risk: Some scoring models consider the size of your business and the level of risk typically associated with your industry.

- Public records: Tax liens, judgments, collections and personal or business bankruptcies can significantly damage your scores and may remain on your credit reports for years.

Steps to build business credit

Building business credit takes time, but the process is straightforward once you know where to start. The key is to establish your business properly, open accounts that report to credit bureaus and consistently demonstrate responsible payment behavior.

1. Establish your business identity.

Before any bureau can track your credit, your business needs to exist as a clearly identifiable entity in their systems. Start by incorporating or forming an LLC; sole proprietorships can build business credit, but having a formal entity makes the process cleaner and separates your business identity from your personal one.

Take the following steps to set up your business properly:

- Get an EIN from the IRS (free and available immediately online).

- Register your business with your state and obtain any required licenses.

- Set up a dedicated business phone number and a physical business address. Dun & Bradstreet, in particular, uses these as identifiers when creating and verifying business profiles.

- List your business phone number in a directory to help D&B locate and verify your company, which is a prerequisite for generating a D-U-N-S Number (more on this below) and, eventually, a PAYDEX score.

2. Get a D-U-N-S number.

A D-U-N-S Number is a unique nine-digit identifier issued by Dun & Bradstreet to every business entity in its database. It’s free to request and essential for building business credit. Without it, D&B can’t generate a PAYDEX score for your company.

You can apply for a D-U-N-S Number directly through Dun & Bradstreet’s website. The standard process takes approximately 30 days, though expedited options are available for a fee. Once you have your D-U-N-S Number, it serves as your business’s identity within D&B’s system and is commonly requested by government agencies (it’s required for federal contracts and business grants), vendors evaluating your creditworthiness and lenders as part of their underwriting process.

3. Open trade lines with reporting vendors.

This is where credit-building truly begins. Trade lines are accounts with vendors or suppliers that extend you credit and report your payment history to one or more business credit bureaus. The key is “reporting”; not all vendors share payment data with bureaus, and accounts that don’t report won’t help you build credit, no matter how reliably you pay.

Starter trade lines are vendors that offer net-30 terms (meaning you have 30 days to pay after receiving an invoice) to newer businesses and report those payment experiences to bureaus. Common examples include office supply companies, shipping and logistics providers and fuel card programs. When opening these accounts, confirm that the vendor reports to at least one major bureau — ideally Dun & Bradstreet or Experian.

4. Get a business credit card.

A business credit card adds another layer to your credit profile and provides a revolving credit line that bureaus can track. When choosing a card, check whether it reports to business credit bureaus, as not all do. Some report only to consumer bureaus, which may help your personal credit but won’t contribute to your business profile.

If your business is new and lacks a credit history, you may need to start with a secured business credit card, which requires a cash deposit as collateral. Secured cards function the same as unsecured cards for credit-building purposes; the bureaus don’t distinguish between the two. As you build a payment track record, you can typically transition to an unsecured card with more favorable terms.

Keep your utilization low. As with personal credit, using a high percentage of your available credit can signal risk. Aim to keep your balance below 30 percent of your credit limit and pay the balance in full each month when possible.

If your business is new or your credit is limited, you can still

get a business card with bad credit by starting with a secured option. These cards require a deposit but report your payment activity the same way as traditional cards, helping you build a track record over time.

5. Pay everything early or on time.

This is the single most important habit you can build to establish excellent business credit. D&B’s PAYDEX score is based entirely on payment timeliness: paying 30 days early can earn a perfect 100, paying on time earns an 80 and paying late can quickly lower your score. Experian and Equifax also place significant weight on payment history.

Set up autopay for recurring obligations and use calendar reminders for invoices that require manual payment. The impact of even one missed payment — from late fees to potential damage to your credit profile — can outweigh the small effort it takes to stay on schedule.

Common mistakes that slow business credit progress

Building business credit is typically straightforward, but a few common missteps can slow your progress or even undo some of the work you’ve already done. Here are some mistakes to watch for:

- Using personal credit for all business expenses: If all of your business spending runs through personal credit cards and personal bank accounts, your business has no credit activity to report. You may have an excellent personal score, but your business profile will be empty, which means lenders and vendors evaluating your company see a blank slate rather than a proven track record.

- Not confirming that vendors report to credit bureaus: Paying vendors on time only builds credit if those vendors are reporting your payment data. Before opening a trade line, confirm which bureaus the vendor reports to. If they don’t report to any, the account may have operational value, but it won’t help you build credit.

- Applying for too much credit at once: Multiple credit inquiries in a short window can signal financial distress, just as they do in the personal credit world. Spacing out your credit applications can help reduce that risk.

- Ignoring your business credit reports: Errors on business credit reports are more common than many owners realize. Incorrect payment data, outdated information or entries that belong to a different business can drag down your scores without you realizing it. It’s worth checking your reports at all three bureaus at least annually and disputing any inaccuracies promptly.

You can be

denied a business bank account even if your personal credit is strong. Banks may review your business credit profile, ChexSystems history, or business documentation, and if your business has little or no credit activity on file, it can raise red flags during the application process.

How long does it take to build business credit?

Business credit doesn’t build overnight, and anyone promising a strong score in 30 days is either misleading you or misunderstanding how the system works.

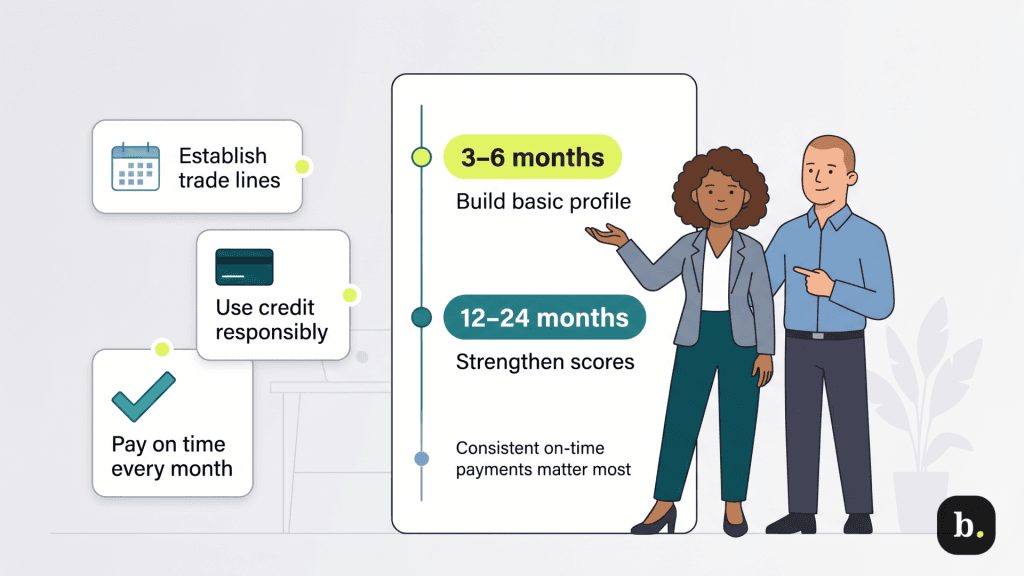

A realistic timeline: Most businesses can establish a basic credit profile (a D-U-N-S Number, two to three active trade lines and an initial PAYDEX score) within three to six months. Building that into a strong, well-rounded profile across all three bureaus typically takes 12 to 24 months of consistent activity: steady trade line payments, responsible credit card use and no negative marks.

The key is consistency. Business credit bureaus are looking for patterns, not one-time events. A year of on-time payments to three or four reporting vendors will do far more for your profile than a burst of activity followed by long gaps.

Building business credit is worth the effort

Business credit doesn’t build itself. Unlike personal credit, which accumulates through everyday financial activity, business credit requires you to take specific, intentional steps, such as registering with bureaus, opening trade lines with reporting vendors and paying everything on time or early.

The process isn’t complicated or expensive, but it does require consistency and attention over time. The payoff — better lending terms, vendor flexibility, reduced personal liability and stronger credibility — makes it one of the highest-return investments a business owner can make in their company’s financial infrastructure.