After more than a decade of decline, business bankruptcy filings are back on the rise. In the year ending September 30, 2025, business filings increased by 5.6 percent — from 22,762 in 2024 to 24,039 in 2025 — United States Courts reported. High interest rates, the lingering effects of inflation and increased business borrowing during the pandemic are all contributing factors to this uptick.

The inability to manage debt and cash flow are the primary drivers of bankruptcy. So if you want to run a business, achieve profitable growth and avoid the missteps that can lead to bankruptcy, this article will provide some actionable steps you can take.

What is business bankruptcy?

Business bankruptcy occurs when a company cannot repay its debts or other financial obligations. Filing for bankruptcy initiates a legal process establishing a plan for the business to eliminate or pay off any debt. This process, conducted under the guidance of the bankruptcy court, also provides legal protection to the bankrupt business in the process.

According to Paul Miller, managing partner and CPA at Miller & Company, LLP, some common business mistakes that lead to bankruptcy include:

- Poor cash flow management, including focusing on profits while ignoring cash reserves.

- Failing to adapt to market changes.

- Overborrowing, which can create an unsustainable debt load.

If you’re

carrying too much business debt and are concerned about making your monthly payments, ask your creditor about establishing an alternative payment plan that’s more manageable in the long term.

Types of bankruptcy

Filing for bankruptcy typically involves one of two paths: restructuring debts or selling assets. The three most common business bankruptcy filings are:

- Chapter 7 bankruptcy. Also known as liquidation, Chapter 7 bankruptcy involves selling business assets to repay creditors. This filing is most common when a business has little to no chance of financial recovery.

- Chapter 11 bankruptcy. Businesses likely to achieve financial recovery typically file for Chapter 11 bankruptcy, also called reorganization. This process allows the business to restructure its debts and repay creditors while remaining open.

- Chapter 13 bankruptcy. Under Chapter 13 bankruptcy, businesses can create a repayment plan to cover their debts over time, typically over three to five years. This type of bankruptcy, also called a wage earner’s plan, is commonly used by individuals and sole proprietors.

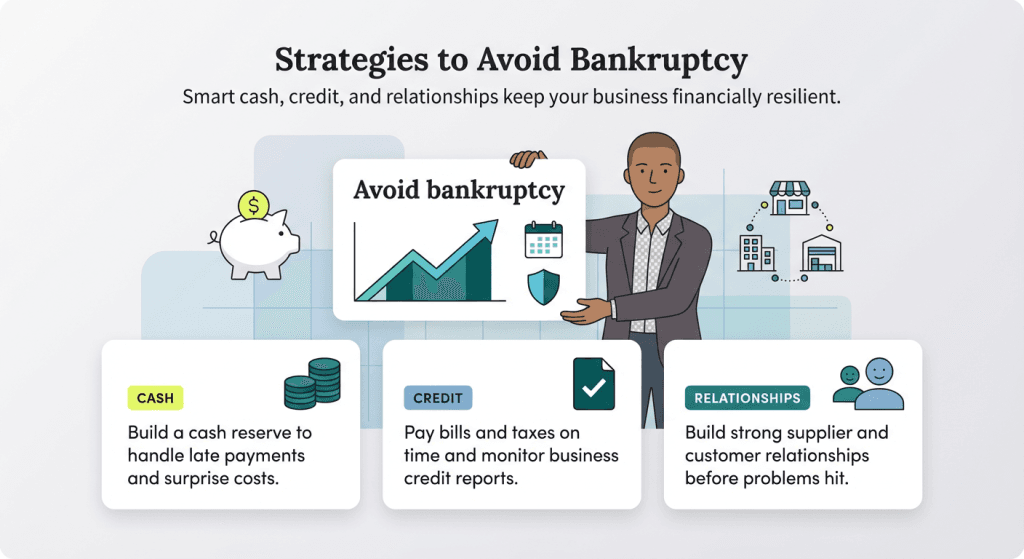

Strategies to avoid bankruptcy

To stay financially healthy and avoid bankruptcy, Miller advised building a strong cash reserve, regularly updating your business plan and diversifying your revenue streams. Let’s take a closer look at five tips to get your debt and cash flow management on track.

1. Pay your bills on time.

Don’t give yourself a reason not to pay your suppliers on time. If you aren’t making timely payments, you’re unnecessarily straining those relationships and slowly building up debt. Further, if you get too far behind on payments, your supplier might freeze services to your business altogether or even take you to court.

Your business credit score will suffer if this happens, which will put you that much closer to bankruptcy. If you foresee any problems fulfilling your payments, be honest with your suppliers. Ultimately, it’s in their best interest to help you, so they can ensure payment and your business in the future.

As a business owner, it’s crucial to keep accurate financial records for your company. The

best accounting software lets you invoice clients and track your expenses and cash flow management.

2. Pay your taxes.

The last thing you want on your credit report is a tax lien. If potential vendors see that you’re behind on your taxes, they’ll likely assume that you won’t pay for their services either. “Keeping up with tax obligations and taking advantage of tax credits can … ease financial pressure,” Miller said.

A tax mishap isn’t necessarily a financial death sentence for your business, but you don’t want the issue to snowball — and with the government, tax problems can escalate quickly. If you get off course with your taxes, be proactive. Set up a payment plan, and stay on good terms with the IRS.

3. Learn to use credit reports.

Credit reports, both your own and those of your customers, are a vital tool for your business success. Start by studying yours to determine where you stand. Potential customers and lenders will look, and you want them to be impressed with what they see.

A credit report is also essential when you’re onboarding a new customer. If a customer’s report raises red flags, you might want to think twice about doing business with them.

4. Have a cash reserve.

Even your best customers can run into financial difficulties. If you monitor their credit reports regularly, you can see early warning signs and work with them to change their payment terms or make other arrangements.

If they do face a financial downfall, you want to be prepared and have the cash on hand to weather the storm. Plan ahead and build as much cushion as possible into your reserves. The best business owners are ready for the worst-case scenario.

5. Build strong relationships.

There is a common factor in each of the previous four tips — relationships. It can be difficult to cultivate relationships in the world of finance and credit and is even harder in a B2B enterprise. But building relationships can be the single biggest factor in your organization’s successful avoidance of the bankruptcy domino effect.

Knowing your suppliers and the organizations you supply, their habits, the points of contact and their financial history goes a long way in overcoming issues. Being able to send an email or make a phone call to clear up any confusion or answer any questions can be vital to a proper understanding of a situation.

If things do become problematic, a relationship can help make hard conversations a bit easier and lead to a plan of action going forward. Further, it can be instrumental in minimizing the potential damage caused by an unavoidable bankruptcy.

It's important to reach out for help as soon as you notice signs that your business is in financial distress. The right financial and

legal support services can help you come up with strategies to get your company back on track.

Bankruptcy warning signs

It’s impossible to predict the exact scenario that will cause a business to file for bankruptcy, but there are some common warning signs to watch out for. If you’re concerned that your business or a vendor is headed down the wrong financial path, some things to watch for include:

- Changes in payment behavior. It’s a major red flag if a business has suddenly stopped making payments to its vendors or utility providers. While some businesses simply have a habit of paying their bills late, it’s almost always a bad sign if they aren’t paying for water, electricity or gas. This is by far the more predictive factor in business failures and indicates a real-time, looming cash flow problem.

- Tax liens. If companies don’t pay government taxes, these liens can add up quickly with local, state and federal entities. Government agencies will always be the first in line to get paid from the liquidation of a failed company’s assets, leaving you with nothing or a few cents for each dollar owed.

- Court judgments. If a business is taking another business to court for unpaid bills, it might be indicative of a cash flow problem. While this is not always the case, companies should see this as a red flag and investigate further. Keep a close watch on this business, as it might already be on the path to bankruptcy.

- Prior involvement with failures in other companies. If company owners have been involved in previous bankruptcies, especially recent ones, this typically increases the chances of future insolvency. A business owner who was part of an organization that went through bankruptcy is more likely to see history repeat itself.

Miller noted that if you start to see signs of financial trouble, review your finances to identify the specific problem areas and determine your next steps. “Cut unnecessary expenses, renegotiate terms with creditors and communicate openly with stakeholders,” he told Business.com. “Seeking advice from a CPA can uncover solutions you might not see on your own.”

The bankruptcy process is lengthy and challenging and not something any business wants to endure. While there is no absolute cure for avoiding the effects of bankruptcy, sound financial practices are just as important in good times as they are in bad, and proactive debt management has always been a critical part of that equation.

Matthew Debbage and Jamie Johnson contributed to the reporting and writing in this article.