This article is sponsored by Intuit.

When you own multiple businesses, it’s common to share services to support one another. But when companies intermingle assets and provide support to one another, keeping track of which business owes what to which of the other businesses can get messy quickly.

When companies rely on manual intercompany processing, it can require the frequent use of estimated “plugs” to force accounts to balance, which can skew the books and make it difficult to understand the true fiscal position of a company — not to mention lead to compliance issues. The problem is that most businesses lack the systems and processes to manage intercompany transactions cleanly, even when those transactions prove useful.

This guide breaks down what intercompany transactions are, why they create so many headaches and how to build systems, and practices that keep your multi-entity books accurate, audit-ready and on schedule. Whether you’re managing two entities or twenty, the principles are the same: standardize your processes, automate where possible and reconcile early and often.

What are intercompany transactions?

Intercompany transactions are financial transactions that occur between two or more entities under common ownership or control. Whenever a parent company charges a subsidiary for shared services, one subsidiary transfers inventory to another or a parent lends capital to a subsidiary for expansion, an intercompany transaction is created.

Common examples include management fees charged by a parent to its subsidiaries, shared service allocations for HR, IT or accounting support, inventory or product transfers between a manufacturing entity and a distribution entity, and intercompany loans with associated interest charges.

The accounting challenge is straightforward in theory but difficult in practice: each intercompany transaction must be recorded in both entities’ books (one side records a receivable, the other a payable), and then those internal transactions must be eliminated when producing consolidated financial statements. After all, a parent company can’t report revenue earned from itself. Getting both sides to match and then eliminating cleanly is where most of the pain lives.

You can avoid a lot of problems by adhering to best practices when it comes to

accounting for multiple companies. Check out our guide to learn more about the best ways to manage finances across multiple entities.

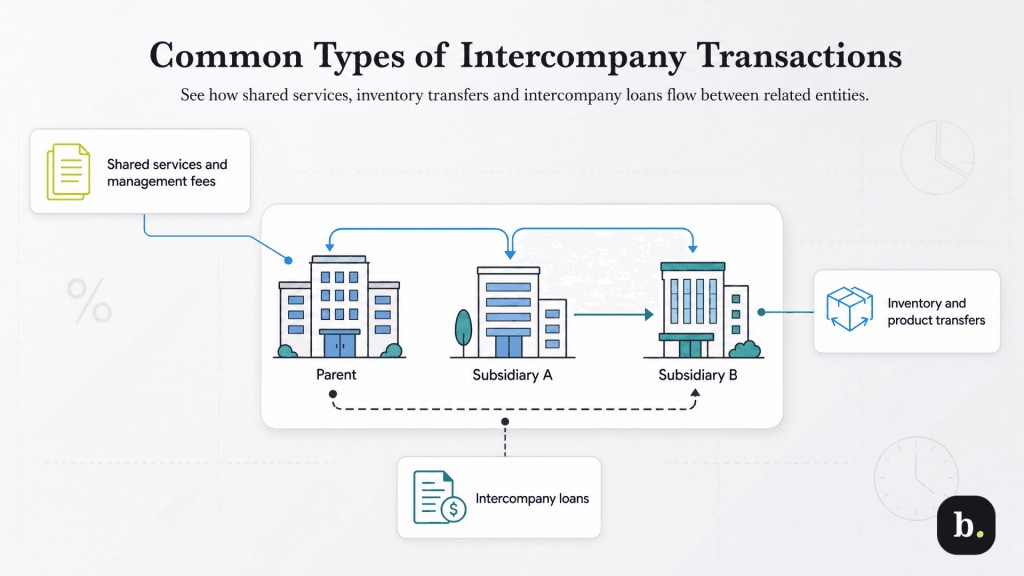

Common types of intercompany transactions

Shared services and management fees

One of the most common intercompany transaction types occurs when a parent company or designated entity provides centralized services to other entities in the group. A corporate headquarters might employ a CFO whose time is shared across three subsidiaries, or maintain an IT department that supports all entities. These costs need to be allocated fairly across the entities that benefit from them.

The key consideration is establishing a defensible allocation methodology. Common approaches include headcount-based allocation, revenue-based allocation or time-study allocation where staff track hours spent on each entity’s work. Whichever method you choose, document it thoroughly and apply it consistently.

Inventory and product transfers

When one entity in a group manufactures products and another sells them, every transfer of goods between them creates an intercompany transaction. The manufacturing entity records a sale (and receivable), while the selling entity records a purchase (and payable). These transactions carry additional complexity because transfer pricing – the price at which goods move between related entities – comes into play and has tax implications so must be documented carefully.

Goods in transit between entities add another wrinkle. If one entity ships inventory on March 30 and the receiving entity doesn’t record the receipt until April 2, month-end reconciliation will show a mismatch that requires documentation to explain to auditors.

Intercompany loans

When a parent company lends money to a subsidiary for operations or expansion, the transaction must be properly documented as a loan with defined interest rates, repayment terms and a formal loan agreement. The lending entity records a receivable and interest income; the borrowing entity records a payable and interest expense. Without proper documentation, tax authorities may reclassify the loan as a capital contribution, changing the tax treatment entirely.

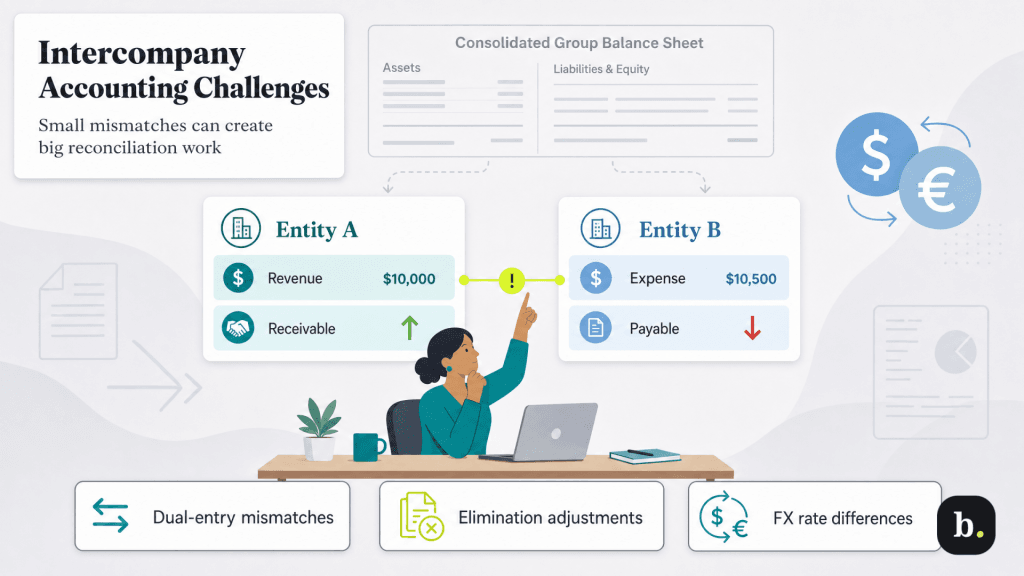

The intercompany accounting challenge

Dual-entry recording

Every intercompany transaction must be recorded in both entities’ books, and both sides must agree perfectly. Entity A records revenue and a receivable; Entity B records an expense and a payable. When these entries are created manually, discrepancies inevitably creep in. An invoice entered for $10,000 in one entity and $10,500 in another creates a $500 mismatch that someone has to track down at close.

Timing differences compound the problem. If Entity A records a charge in March but Entity B doesn’t process the corresponding bill until April, month-end reconciliation will show a discrepancy even though neither side made an error. Multiply this by dozens or hundreds of intercompany transactions per month, and the reconciliation burden becomes significant.

Elimination entries for consolidation

Consolidated financial statements must present the corporate group as a single economic entity, which means all intercompany revenue, expenses, receivables and payables need to be eliminated. If your manufacturing entity sold $5 million in goods to your distribution entity, that $5 million can’t appear as revenue in the consolidated income statement; it’s internal activity, not revenue earned from external customers.

Elimination entries reverse these intercompany transactions for consolidation purposes. The challenge is ensuring both sides match cleanly so the elimination is exact. When intercompany accounts don’t balance, finance teams resort to manual top-side adjustments or “plugs” to force accounts into balance, which raises immediate red flags with auditors.

Currency complications

For organizations with foreign subsidiaries, intercompany transactions often cross currency boundaries. When a U.S. parent charges management fees to a European subsidiary, the fee is denominated in one currency but may need to be recorded in another. Exchange rate differences between the date Entity A records the charge and the date Entity B processes the payment can create discrepancies that are simply a function of currency fluctuation.

These currency-related differences must be identified, documented and properly accounted for during consolidation. Without a system that standardizes exchange rate handling across entities, each close cycle can become a time-consuming exercise in reconciling currency-related variances.

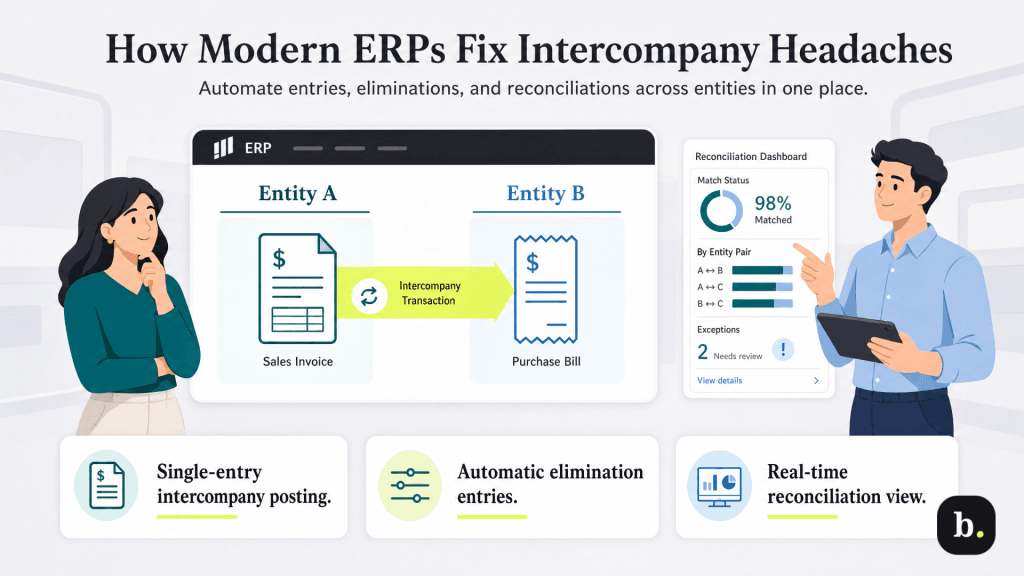

How modern ERP systems solve intercompany issues

Automated intercompany transaction processing

The single biggest improvement modern ERP systems offer is the ability to record an intercompany transaction once and have the corresponding entry automatically created in the other entity. Instead of two people in two entities manually entering the same transaction (with all the discrepancy risk that entails) the system generates both sides from a single entry.

Intuit Enterprise Suite, for example, automates intercompany sales so that when one entity creates an invoice to another entity, the system simultaneously generates the matching bill in the receiving entity. Both sides post together, ensuring the consolidated report stays accurate without manual journal entries. This eliminates the core risk of manual dual-entry: the possibility that two sides of the same transaction don’t agree.

Built-in elimination automation

Generating elimination entries manually is one of the most error-prone steps in consolidation. Modern ERPs automate this process by identifying intercompany transactions and generating the necessary elimination journal entries automatically.

Intuit Enterprise Suite introduced transaction-level eliminations, which automatically generate and track intercompany eliminations in real time rather than waiting until period-end. The platform also added bulk import of intercompany journal entries and AI-powered auto-categorization for intercompany sales.

Intercompany Reconciliation Tools

Beyond transaction processing and elimination, modern ERPs provide reconciliation dashboards and matching tools that give finance teams real-time visibility into intercompany account balances. These tools surface out-of-balance accounts immediately rather than forcing teams to discover discrepancies during the close. Features typically include aging reports for intercompany payables and receivables, exception reporting and alerts for unmatched transactions, and drill-down capabilities that let teams trace discrepancies to their source.

Intuit Enterprise Suite provides a centralized Intercompany Transactions tab within its consolidated view, giving finance teams a single source of truth for viewing, eliminating and accepting intercompany bills across entities. This centralized approach replaces the fragmented, entity-by-entity reconciliation process that bogs down so many multi-entity closes.

Best practices for intercompany management

Establish clear policies

Before any system can help, your organization needs documented policies that define which intercompany transactions are expected, how they should be priced, who must approve them, and when they must be reconciled. Without clear policies, even the best software can’t prevent process breakdowns.

Your intercompany policy should cover standard pricing for shared services and how allocations are calculated, approval workflows for intercompany charges (who can initiate, who must approve), settlement schedules (monthly, quarterly or upon demand), and documentation requirements for each transaction type. Intercompany loan agreements deserve special attention; they should include defined interest rates, repayment schedules and formal terms that satisfy tax authority scrutiny.

Use standardized processes

Standardization reduces errors more than almost any other single intervention. Use template invoices for recurring intercompany charges, apply consistent allocation methodologies across all entities and maintain a regular settlement schedule. Decide whether intercompany management should be centralized (one team manages all intercompany activity) or decentralized (each entity manages its own side), and document the decision.

Monthly reconciliation discipline

The most costly mistake in intercompany management is waiting until year-end to reconcile. Discrepancies that are minor and easy to investigate in the month they occur become major obstacles when they’ve been compounding for twelve months. APQC benchmarking data shows the median monthly close takes 6.4 calendar days. Additional research reported by CFO.com indicates that 50% of finance teams require six or more business days to close their books. Organizations that reconcile intercompany accounts as part of their monthly close catch issues when they’re small and traceable, rather than letting them accumulate into year-end reconciliation crises.

Designate clear ownership for each intercompany relationship; someone at Entity A and someone at Entity B should be accountable for ensuring their side matches. Establish an escalation process for unresolved differences, and use your ERP’s reconciliation tools for ongoing monitoring rather than periodic manual reviews.

ERPs plus SOPs equal success

Effective intercompany management comes down to two things: automation and discipline. The best ERP system in the world won’t save you if your policies are unclear and no one owns the reconciliation process. And the most rigorous manual process will eventually break down as your entity count and transaction volume grow.

Start by assessing your current intercompany pain points honestly. Where do discrepancies originate? How long does intercompany reconciliation add to your close cycle? Are you relying on “plugs” to force accounts into balance? The answers will tell you whether you need better processes, better technology or both, and they’ll help you build a business case for investing in the systems and practices that keep multi-entity accounting clean, compliant and on schedule.