When you apply for a business loan, one of the first things you should decide is whether it should be secured or unsecured. The main difference between the two comes down to collateral: a secured loan requires you to have assets that the lender can seize if you default, while an unsecured loan does not. That distinction impacts every part of the borrowing experience — from interest rates and borrowing limits to approval requirements and personal risk.

The right choice depends on what assets you have, how much capital you require, how quickly you need the loan and how much risk you’re willing to take. This guide breaks down how each loan type works, the advantages and drawbacks of both and how to determine which one is better for your business.

What is a secured business loan?

A secured business loan is backed by collateral — a tangible or financial asset that the lender has a legal claim to if the borrower defaults on the loan. The collateral serves as a safety net for the lender, reducing their risk and allowing them to offer better terms to the borrower.

Common forms of collateral for business loans include commercial real estate, equipment and machinery, inventory, accounts receivable and certificates of deposit. Sometimes lenders may also accept personal assets like a home or personal savings account. The specific collateral required depends on the loan, the lender and the amount borrowed.

In a collateral arrangement, lenders typically file a UCC (Uniform Commercial Code) financing statement, which is a public record establishing the lender’s claim to the pledged assets. A UCC filing can be tied to a specific asset — like a piece of equipment being financed — or it can take the form of a blanket lien, which gives the lender a claim to all of the business’s assets.

Blanket liens are common on traditional bank loans and

SBA loans, and they can affect your ability to secure additional financing until the lien is satisfied and released.

Several common loans fall into the secured category. SBA 504 loans, which are designed for commercial real estate and heavy equipment purchases, are secured by the asset being acquired. Equipment financing is similar, with the equipment itself serving as collateral. Traditional bank term loans often need collateral, too, particularly for larger loan amounts. Even SBA 7(a) loans — the SBA’s most popular program — require lenders to follow their standard collateral policies for loans over $50,000, and a personal guarantee from any owner holding 20 percent or more of the business is necessary on all SBA loans regardless of size.

What is an unsecured business loan?

An unsecured business loan does not require the borrower to have collateral. The lender approves the loan based on the borrower’s credit rating, business revenue, time in business and financial health. Because the lender has no specific asset to seize in the event of default, unsecured loans carry more risk for the lender — and that risk is passed on to the borrower in the form of higher interest rates, lower borrowing limits and stricter qualification criteria.

Most unsecured business loans also require a personal guarantee, which makes the business owner liable for repayment if the business cannot pay. Some lenders also file blanket UCC liens even on loans marketed as unsecured, giving them a general claim to business assets.

Common unsecured business loan products include unsecured term loans from online lenders, business lines of credit, business credit cards and some SBA 7(a) loans for smaller amounts (SBA Express and Export Express loans under $50,000 generally do not require collateral). Revenue-based financing and merchant cash advances are also typically unsecured, though they come with their own costs that can make them more expensive than traditional loans.

The term “unsecured” means no specific collateral is pledged upfront, but personal and business liability can still be substantial.

How are secured and unsecured business loans different?

While the collateral requirement is the biggest distinction that criteria impacts nearly every aspect of the borrowing experience, including:

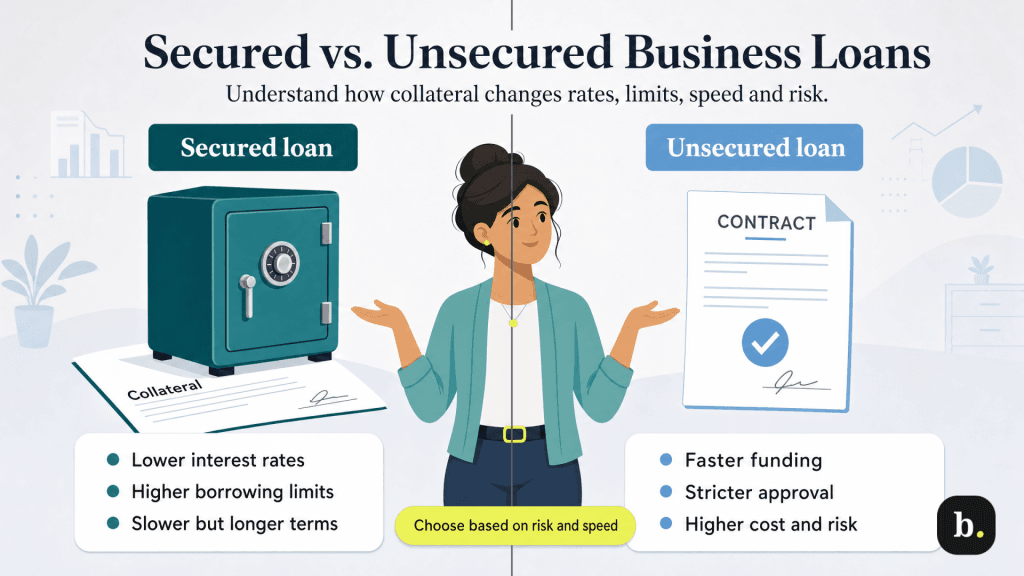

Interest rates. Secured loans almost always carry lower interest rates than unsecured loans. Because the lender has a claim to specific assets, their risk is reduced and they pass that savings on to the borrower. Secured bank loans may carry rates in the range of 7 percent to 12 percent, while unsecured loans from online lenders range from 14 percent to 36 percent or higher. That gap gets bigger for borrowers with weak credit scores.

Borrowing limits. Secured loans typically allow you to borrow more, because the collateral gives the lender confidence that they will recover their investment. It’s not uncommon for secured loans to reach six or seven figures, particularly when backed by commercial real estate. Unsecured loans are generally capped at lower amounts — often $250,000 to $500,000.

Approval criteria. Secured loans may be easier to qualify for because the collateral offsets the lender’s risk. A borrower with moderate credit but substantial collateral may still be approved for a secured loan, while an unsecured lender would likely decline or charge a much higher rate. However, unsecured lenders focus heavily on credit score, revenue and cash flow — criteria that favor established, profitable businesses with strong financial records. [Read related article: What to Do If You Can’t Get a Business Loan]

Funding speed. Unsecured loans are generally faster to process. Without the need for collateral appraisals, title searches and asset documentation, lenders can underwrite and fund unsecured loans in days rather than weeks. Some online unsecured lenders fund within 24 to 48 hours. Secured loans, particularly those involving real estate, often take several weeks or longer because of the additional due diligence required.

Repayment terms. Secured loans usually offer longer repayment terms, which leads to lower monthly payments. SBA 504 loans, for example, can extend up to 25 years for real estate or equipment purchases. Unsecured loans are usually structured with shorter terms — often one to five years — which means higher monthly payments but less total interest if the rate is comparable.

Risk to the borrower. This is where the tradeoff becomes most tangible. With a secured loan, defaulting means you could lose the pledged asset — your commercial property, your equipment or, in some cases, your personal home. With an unsecured loan, there’s no specific asset at immediate risk of seizure, but a personal guarantee still exposes the owner’s personal finances. In either case, default will damage your credit and can lead to legal action.

What are the pros and cons of secured business loans?

Secured business loans have advantages and disadvantages:

Pros:

- Interest rates are lower.

- There are higher borrowing limits and longer repayment terms.

- Borrowers with imperfect credit can qualify more easily.

- The cost of a secured loan usually costs less over its lifetime than unsecured loans.

Cons:

- You can lose your assets.

- The application process is more complex and time-consuming, often requiring appraisals, inspections and extensive documentation.

- Not all businesses have sufficient collateral to offer, such as service-based businesses, tech startups and other asset-light companies.

What are the pros and cons of unsecured business loans?

Unsecured business loans have advantages and disadvantages:

Pros:

- They are quick and simple to obtain.

- There is no collateral requirement so it is not necessary to own physical assets or risk any you might have.

- The application process is typically faster and less document-intensive.

- Many online lenders can fund within days.

Cons:

- They carry higher interest rates to compensate the lender for the additional risk, and borrowing limits are generally lower.

- Qualification criteria are stricter in terms of credit score and revenue since lenders need repayment assurance without collateral.

- Personal guarantees and blanket liens are common, so the owner’s financial exposure may be greater than expected.

How do you decide between secured and unsecured loans?

Ask a few key questions to determine whether you should opt for secured or unsecured financing:

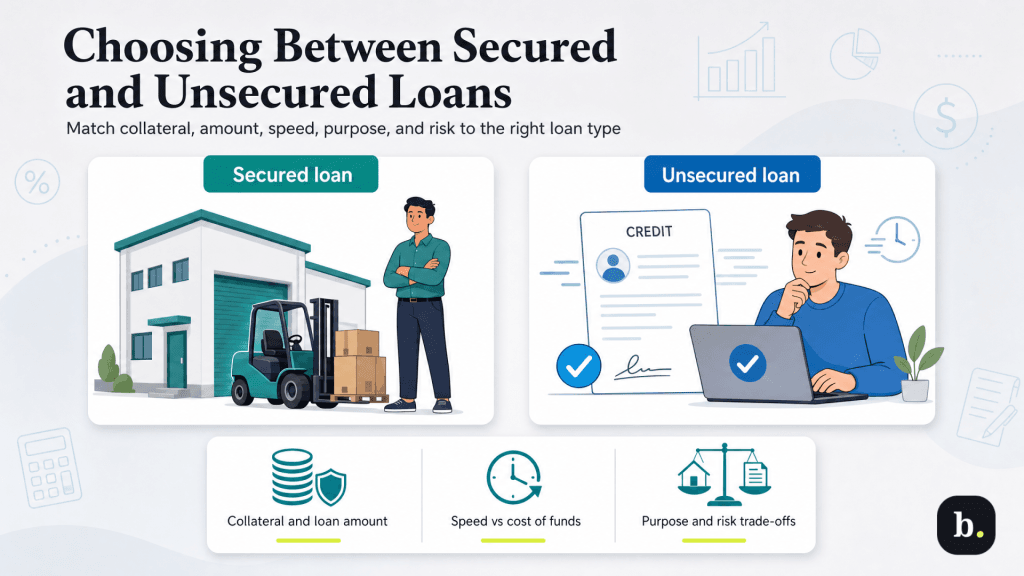

Do you have collateral to pledge? If your business owns valuable assets — real estate, equipment, substantial inventory — a secured loan will typically save you money through lower rates and more favorable terms. If your business is asset-light, an unsecured loan may be your only realistic option.

How much do you need to borrow? For larger loan amounts, secured financing is often the more practical choice. Lenders are simply more willing to extend six- and seven-figure loans when they have collateral backing the commitment. If you need a smaller amount for working capital or a short-term need, an unsecured loan or line of credit may suffice.

How quickly do you need the funds? If timing is critical — you need to cover payroll, seize a time-sensitive opportunity or manage an unexpected expense — the faster processing of unsecured loans may outweigh the cost premium. If you have the luxury of time, a secured loan’s longer application process will likely pay for itself through lower rates.

What’s the purpose of the loan? Match the loan structure to the goal. Buying commercial real estate or heavy equipment naturally lends itself to secured financing, since the asset being purchased serves as the collateral. Working capital, marketing expenses or operational costs are better suited to unsecured products like lines of credit or short-term loans.

What’s your risk tolerance? Consider what happens in a worst-case scenario. If you pledge your commercial property and the business struggles, losing that asset could be devastating. But, if you take an unsecured loan with a personal guarantee and default, your personal finances are in jeopardy. Neither path is risk-free — the question is which one is more manageable for you.

No matter which direction you choose, read the fine print carefully. Pay attention to whether a personal guarantee is required, whether the lender will file a UCC lien and what the total cost of borrowing looks like.

[Read more about some of the best loan and financing options]Which loan type is the best option?

Secured and unsecured business loans serve different purposes and suit different situations. Secured loans offer lower costs and higher borrowing limits in exchange for putting an asset on the line. Unsecured loans offer speed and flexibility but at a higher price and with lower borrowing ceilings. The “best” option is the one that aligns with your specific financial situation, your available assets, the amount you need and how much risk you’re prepared to accept.