Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Business Loan Interest Rates: What to Expect in 2026

From current rates to smart borrowing strategies, here’s what to expect in 2026

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

If you’re a small business owner shopping for a loan in 2026, the interest rate landscape is better than it was a year ago — but still far from simple. The Federal Reserve cut rates three times in the second half of 2025, bringing the federal funds rate down to a target range of 3.5 percent to 3.75 percent and the prime rate to about 6.75 percent. That relief, however, has been tempered by persistent inflation, elevated energy costs driven in part by Middle East tensions, and geopolitical uncertainty that has given the Fed reason to pause its easing cycle.

The result is a borrowing environment where rates vary dramatically, from under 7 percent at traditional banks to well over 50 percent for some alternative financing products. The rate you’ll actually pay depends on the type of loan, the lender, your creditworthiness and the collateral you bring to the table. Understanding these ranges and the forces shaping them is the first step toward applying for a business loan and securing affordable capital for your organization.

What’s driving business loan rates in 2026?

Several macroeconomic forces are shaping the business lending environment this year, and understanding these broader lending trends can help you anticipate where rates may be headed.

Federal Reserve policy

The Federal Reserve’s three rate cuts in late 2025 — each by 25 basis points, in September, October and December — brought meaningful relief after a prolonged period of elevated rates. However, the Fed held rates steady at both its January and March 2026 meetings, keeping the federal funds rate at 3.5 percent to 3.75 percent. The March meeting’s “dot plot” pointed to one additional cut this year and another in 2027, though the timing remains uncertain. Markets widely expect another hold at the upcoming April 28-29 meeting.

Inflation

While inflation has cooled considerably from its 2022 peak, it hasn’t returned to the Federal Reserve’s 2 percent target. Headline CPI rose to 3.3 percent in March 2026 — up from 2.4 percent in February — driven in part by a 12.5 percent increase in energy costs year over year. Core CPI, which strips out food and energy, rose a more modest 2.6 percent year over year, suggesting that underlying inflation remains relatively contained.

The picture may shift in the months ahead. Energy prices may moderate in the coming months, which could allow the Fed to look past the March spike and refocus on the underlying inflation trend. Even so, the Fed has made clear it wants sustained progress before resuming rate cuts, and with headline inflation running well above its 2 percent target, that timeline remains difficult to predict.

Tip

When you choose a small business loan, focus on flexibility as much as rate. In a shifting rate environment, terms like fixed versus variable interest, repayment terms and prepayment penalties can matter just as much as the headline rate.

Geopolitical uncertainty

The U.S. war with Iran has injected uncertainty into the global economy, particularly through their impact on oil prices. Rising energy costs can simultaneously push inflation higher and slow growth, putting the Federal Reserve in a difficult position. Chair Jerome Powell has acknowledged these risks but indicated the committee is taking a wait-and-see approach.

For small business borrowers, that uncertainty points to a rate environment that’s likely to stay relatively range-bound in the near term. That makes the window for refinancing business loans or locking in current rates more relevant than waiting for cuts that may not arrive on a predictable schedule.

Treasury yields

For fixed-rate loan products (particularly SBA 504 loans), Treasury bond yields matter as much as the prime rate. As of early April 2026, the five-year Treasury yield was approximately 3.92 percent, and the 10-year yield was around 4.30 percent, both higher than at the start of the year. These elevated yields have pushed up borrowing costs for fixed-rate products even as the prime rate has held steady.

Current rates by loan type

There is no single “average” business loan rate. What you’ll pay depends on your business’s financial circumstances, the product you choose and the lender you work with. Here’s an estimate of what to expect from each major category.

Loan Type

Estimated Interest Rate Range in 2026

Bank term loan

8% – 13%

Online term loan

10% – 40%

SBA 7(a) loan

9.75% – 14.75%

SBA 504 loan

5% – 7.5%

SBA microloan

8% – 13%

Merchant cash advance

40% – 350%

Note: Interest rates are subject to change based on the individual lender, a borrower’s qualifications and market conditions. These ranges are intended for estimation purposes only.

In practice, borrowing costs can vary more widely depending on the borrower and loan structure. While bank loans for stronger applicants tend to stay in the single digits, high risk business loans can reach into the double digits or higher. Expect to need a personal credit score of 680 or higher (720-plus for the best rates), at least two years in business, strong revenue and often collateral and a personal guarantee from the business owner. The application process is longer than with online lenders, typically taking several weeks from application to funding.

SBA loans

SBA loans are partially guaranteed by the federal government, which helps reduce risk for lenders and keeps borrowing costs lower than many other financing options. Here’s how rates for the most common SBA loan programs compare.

SBA 7(a) loans: The SBA’s flagship lending program offers rates structured as a base rate — typically the Wall Street Journal prime rate, currently about 6.75 percent, plus a spread that the SBA caps based on loan size and term. Maximum rates range from approximately 9.75 percent to 14.75 percent. For loans over $250,000 with maturities exceeding seven years, the ceiling is about prime plus 3 percent. Smaller loans come with higher caps — up to prime plus 6.5 percent for loans of $50,000 or less. Lenders don’t always charge the maximum, though, so it’s worth comparing offers across multiple SBA-preferred lenders.

SBA 504 loans: Designed for major fixed-asset purchases like commercial real estate and heavy equipment, SBA 504 loans offer fixed rates tied to Treasury bond yields. As of April 2026, effective borrower rates on 20-year terms are about 5 percent to 6 percent — low for a long-term loan like this. The tradeoff is a narrower use case, as you can’t use 504 loans for working capital or inventory.

SBA microloans: The SBA microloan program provides loans of up to $50,000 through nonprofit, community-based intermediary lenders. These loans target startups and small businesses that may not qualify for larger products. Rates vary by intermediary but are generally higher than 7(a) loans, with repayment terms of up to seven years.

Did You Know?

If an SBA loan goes into default, the SBA may reimburse the lender for a portion of the balance, but the borrower remains fully responsible for repayment.

Online term loans and lines of credit

Online lenders tend to prioritize speed and accessibility over price, making them a go-to option for fast business loans. Many can fund within 24 to 48 hours, compared to several weeks to a few months for SBA loans.

But that speed comes at a cost: term loan APRs range from 14 percent to 99 percent, with many lenders clustering in the 18 percent to 45 percent range for average-risk borrowers. Lines of credit through online platforms typically carry rates of about 10 percent to 35 percent APR for established businesses, though rates can run higher for newer or higher-risk borrowers.

Merchant cash advances

Merchant cash advances aren’t technically loans; they’re advances against future sales, repaid as a percentage of daily credit or debit card revenue. They use factor rates, typically between 1.1 and 1.5, rather than interest rates. When you convert that to an effective APR, MCAs can exceed 50 percent and often climb into the triple digits, depending on how quickly they’re repaid. In some cases, they can even go past 200 percent. They’re best understood as a last-resort financing option for businesses that don’t qualify for more traditional credit.

Bottom Line

The best business loans and financing options for you depend on how quickly you need funding, your credit profile and how much you're willing to pay for flexibility. Lower-cost options like bank and SBA loans take longer to secure, while faster funding typically comes with higher rates.

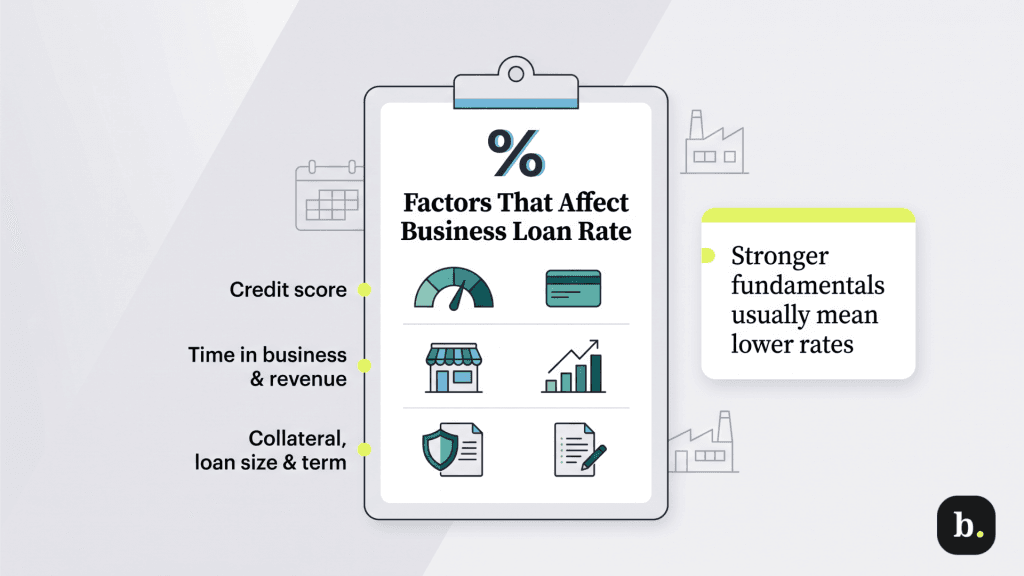

Factors that affect your business loan rate

While macroeconomic conditions set the broader rate environment, several borrower-specific factors determine the rate you’ll actually receive.

Credit score: Your personal credit score is often the single most influential factor, especially for smaller businesses without an established business credit profile. Most lenders prefer a personal score of 680 or higher for competitive rates, and borrowers above 720 tend to get the most favorable terms. Scores below 600 will significantly narrow your options and push you toward more expensive products. As your company grows, lenders may also consider your business credit score from bureaus like Dun & Bradstreet or Experian.

Time in business and revenue: Lenders use your operating history and revenue as a proxy for stability. Most traditional banks want to see at least two years in business and consistent revenue. Online lenders may accept businesses with as little as six months of history but typically offset that added risk with higher rates.

Collateral: Offering collateral — real estate, equipment, inventory or accounts receivable — reduces the lender’s risk and typically results in a lower rate. The loan-to-value ratio, which measures the loan amount against the appraised value of the collateral, also affects pricing.

Loan amount and term: Larger loans often come with lower rates because the lender’s fixed costs are spread over a bigger principal. Term length also matters. Shorter loans may carry higher rates, while longer loans spread the cost but accumulate more total interest.

Industry: Some industries are considered higher risk than others. Businesses in sectors with volatile revenue, high failure rates or regulatory uncertainty (such as cannabis businesses) may face higher rates or fewer options.

Fixed vs. variable rates: In 2026’s environment, this choice carries real strategic weight. Variable rates will decrease if the Fed cuts later this year, potentially saving money. Fixed rates lock in your cost upfront, providing predictability but no benefit if rates fall. If you believe the Fed will resume cutting, a variable rate may be advantageous. If you prefer certainty, fixed rates remove the guesswork.

How to get the best business loan rate

You can’t control the Federal Reserve or the price of oil, but there are meaningful steps you can take to secure the most competitive rate possible.

Strengthen your credit before applying: If your loan need isn’t urgent, spending a few months improving your credit can pay dividends. Pay down outstanding balances, resolve any errors on your credit report and avoid opening new accounts in the months leading up to your application.

Shop multiple lenders: This is perhaps the most underutilized strategy in small business lending. Rates can vary significantly between lenders even for the same loan product. Get quotes from at least three to five sources, including banks, credit unions, SBA-preferred lenders and online platforms. For SBA loans, remember that lenders are not required to charge the maximum; some offer prime plus 1.75 percent to 2.25 percent for well-qualified borrowers.

Consider SBA loans for rate protection: The SBA’s rate cap system means you’ll never pay above a defined ceiling, regardless of which approved lender you use. The tradeoff is a longer application process, but for many borrowers, the savings justify the wait.

Focus on total cost, not just the rate: Interest rate is just one component of borrowing cost. Origination fees, guarantee fees, closing costs and prepayment penalties all factor in. The annual percentage rate (APR) captures these costs more completely, so always compare loans on an APR basis.

Take advantage of the current window: With rates holding steady and the Fed expected to pause through at least mid-2026, borrowers have a relatively stable window to compare options without the pressure of imminent increases. The current landscape — while not as favorable as the near-zero rates of 2020-2021 — is meaningfully improved from the 2023-2024 peak.

Tip

Alternative lenders can be a useful option if you need faster funding or don't meet traditional bank requirements, but their rates are typically higher. If you go this route, compare offers carefully and look beyond the speed to understand the total cost.

What today’s rate environment means for your business

Business loan interest rates in 2026 cover a wide range, from under 7 percent at traditional banks to well over 50 percent for merchant cash advances. The Fed’s three rate cuts in late 2025 brought some real relief, but rates have held steady so far this year as policymakers watch inflation and geopolitical risks. One additional cut is possible in 2026, but the timing depends on how the broader economy plays out.

For borrowers, the takeaway is pretty simple: preparation and lender selection matter just as much as the rate environment. A well-qualified borrower who shops multiple lenders and understands the full cost of each offer will often pay significantly less than someone who takes the first option available. Rates may not return to pre-2022 levels anytime soon, but with the right approach, affordable financing is still within reach.

Adam Uzialko, the accomplished senior editor at Business News Daily, brings a wealth of experience that extends beyond traditional writing and editing roles. With a robust background as co-founder and managing editor of a digital marketing venture, his insights are steeped in the practicalities of small business management.

At business.com, Adam contributes to our digital marketing coverage, providing guidance on everything from measuring campaign ROI to conducting a marketing analysis to using retargeting to boost conversions.

Since 2015, Adam has also meticulously evaluated a myriad of small business solutions, including document management services and email and text message marketing software. His approach is hands-on; he not only tests the products firsthand but also engages in user interviews and direct dialogues with the companies behind them. Adam's expertise spans content strategy, editorial direction and adept team management, ensuring that his work resonates with entrepreneurs navigating the dynamic landscape of online commerce.