Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Use this calculator to estimate how different tax treatments could influence your investment growth over time.

Many business owners eventually face the question of how their investments should be taxed. Choosing between tax-free, tax-deferred and taxable options — or blending them — can shape how your money grows over the long term. The right approach often depends on factors like your current tax bracket, investment horizon and expected returns.

Our calculator lets you compare how savings may grow under different tax treatments by adjusting a few key assumptions, so you can compare potential outcomes side by side.

Your current investment balance is the amount you’re starting with today, before any new contributions or investment growth. It includes funds already invested or ready to invest. In the calculator, this matches the Initial balance or deposit field.

Annual contributions represent how much you plan to add to your investment each year. These are ongoing deposits made over time, not the investment’s rate of return or market growth. For example, some investors base this number on IRA contribution limits. For tax year 2026, the maximum IRA contribution is $7,500 for individuals under age 50 and $8,600 for those age 50 or older. In the calculator, this corresponds to the Annual savings amount field.

This refers to how long your money remains invested and compounding. (If you want to isolate how time alone affects growth, a compound interest calculator can help you model the impact of longer investment times.) Many people choose a timeline based on retirement goals, but you can use any period that reflects your planning horizon. It represents the length of the projection, not necessarily how long you must keep the investment. Enter this in the Number of years for the analysis field.

The before-tax return is the investment’s assumed rate of growth before taxes are applied. With taxable investments, gains are typically taxed along the way, which can influence long-term compounding. This is a performance assumption, separate from how much you contribute each year. In the calculator, this is the projected return used for the fully taxable investment scenario.

With a tax-free investment, earnings typically aren’t subject to federal or state income tax, which can change how growth compounds over time. Putting tax-free results next to taxable or tax-deferred ones makes it easier to see how taxes can change your final outcome. In the calculator, this is the return used for the tax-free investment.

Tax-deferred investments allow taxes to be paid later rather than each year. For example, taxes may apply when you withdraw funds from certain retirement accounts or sell an investment at a gain. The before-tax return represents the total expected growth rate before state and federal income taxes are applied. Like other return assumptions, this reflects projected growth rather than annual contribution amounts. In the calculator, this is the projected return used for tax-deferred investments.

Your marginal tax bracket is the highest tax rate applied to your last dollar of income. The U.S. tax system uses progressive rates, meaning you pay lower rates on some income and higher rates as earnings rise. For tax year 2026, federal brackets range from 10 percent to 37 percent, with the top rate applying to taxable income above $640,600 for single filers and $768,700 for married couples filing jointly.

In the calculator, this matches the Marginal tax bracket field. (Some investors also compare scenarios using a taxes and inflation calculator to see how long-term purchasing power may shift alongside changing tax rates.)

Investments may be taxed when you earn returns, at a later date, or in some cases, not at all. Here’s how it works:

With taxable investments, you pay taxes on income as it’s generated, such as interest, dividends or realized gains. Common examples include savings accounts, money market accounts and brokerage accounts that hold dividend-paying stocks or bonds.

Recent FDIC data shows that traditional savings accounts yield about 0.39 percent annually on average, while many high-yield savings accounts advertise rates above 4 percent, with some approaching 5 percent depending on the institution and account requirements.

You don’t receive a tax deduction for contributions to these accounts as you would with a traditional IRA. However, withdrawals typically aren’t taxed as ordinary income because contributions were made with after-tax dollars, though taxes may apply when gains are realized.

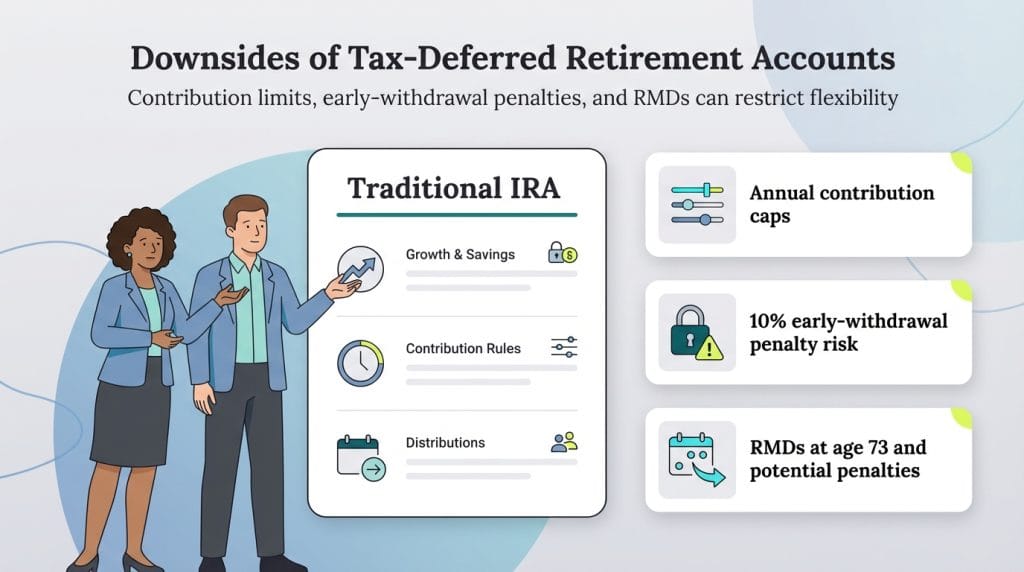

Tax-deferred investments let you postpone paying taxes until a later date, generally when you take distributions or withdraw funds.

A traditional IRA, for example, may allow you to deduct eligible contributions and defer taxes on investment earnings until you withdraw money, typically in retirement. You still pay income tax on taxable distributions from the account, but the tax liability occurs later rather than annually. Bear in mind that the calculator doesn’t account for the possibility that a tax deduction could leave you with more money available to invest in the year you contribute to a traditional IRA or other tax-advantaged retirement account.

Another strategy sometimes discussed alongside tax-deferred investing involves qualified small business stock (QSBS), which can provide significant tax advantages for certain investors. Under Section 1202 of the Internal Revenue Code, investors who hold QSBS for at least five years may exclude up to 100 percent of eligible capital gains from federal taxes, with a maximum exclusion of $10 million or 10 times the adjusted basis, whichever is greater.

Municipal bonds are among the most widely used tax-free investment options. Roughly $4.4 trillion in municipal bonds were outstanding as of the third quarter of 2025, according to SIFMA Research. Interest income is generally exempt from federal income tax, and bonds issued by your home state may also avoid state income taxes. AAA-rated 10-year municipal bond yields have recently hovered in the mid-2 percent range, which can look more attractive to higher-income investors when viewed on a tax-equivalent basis.

An easy way to invest in municipal bonds is to buy shares in a municipal bond fund.

When evaluating tax-free investments, calculate the tax-equivalent yield to make accurate comparisons. For instance, a 3.5 percent municipal bond yield equals roughly a 4.6 percent taxable yield for someone in the 24 percent federal tax bracket, making it potentially more attractive than many taxable alternatives.

Another example of a potentially nontaxable investment may be your personal residence. If you live in your home for at least two years, you may qualify to exclude up to $250,000 ($500,000 if married filing jointly) of capital gains from federal income taxes.

It’s easy to assume that paying taxes now or later leads to similar results. The future value of your deferred-tax account will typically be higher than a comparable account on which you have been paying taxes along the way. However, after you withdraw your money and pay state and federal income taxes, the difference in value may be smaller than many investors expect.

Many retirees end up with lower taxable income than they had while working, which is one reason tax deferral can matter later on. Social Security Administration data for 2026 shows the average monthly retirement benefit at about $2,071, or roughly $24,852 per year. Depending on household income and other retirement funds, that shift may move some investors into lower federal tax brackets.

Geographic arbitrage presents another potential benefit. Nine states — Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming — have no state income tax. Business owners who defer taxes while working in high-tax states like California (13.3 percent top rate) or New York (10.9 percent top rate) may realize meaningful savings by relocating to lower-tax states in retirement, depending on their circumstances.

There is one additional benefit of starting and contributing to a traditional IRA to defer taxes: the potential upfront tax deduction. Being able to take a deduction for eligible contributions can encourage consistent saving. If you’re preparing your tax return and want to reduce your current tax liability, you may still be able to contribute to an IRA for the prior tax year before the filing deadline.

One drawback is that IRA contribution limits cap how much you can invest each year. If you want to build a traditional IRA balance that meaningfully supports retirement, starting early can make a significant difference. Annual IRA contributions are limited to $7,500 for individuals under age 50 and $8,600 for those age 50 or older as of 2026.

Additionally, putting money in a tax-deferred IRA could create challenges if you need access to the funds sooner. The IRS generally imposes a 10 percent early-withdrawal penalty on distributions taken before age 59½, although certain exceptions may apply. At the same time, the possibility of penalties can encourage long-term saving by discouraging early withdrawals.

Beginning at age 73, most traditional IRA owners must take required minimum distributions (RMDs). Failing to take the required amount may result in IRS penalties.

The right mix of taxable, tax-deferred and nontaxable investments often depends on your current tax situation, how your business is structured and your long-term financial goals. The scenarios below illustrate how different strategies may apply in common planning situations.

Active traders may benefit from using tax-advantaged accounts strategically. Because trades inside most retirement accounts don’t create current taxable events, frequent trading typically doesn’t generate annual capital gains reporting. However, wash sale rules can still apply in some cases, so traders should review IRS guidance before assuming their trades are completely shielded from tax consequences.

Some traders keep frequently traded positions in a self-directed IRA while using a taxable brokerage account for strategies that require margin or more advanced options trading.

Most nontaxable investments, however, are designed for long-term income and buy-and-hold strategies, so they may not appeal to traders seeking frequent market exposure.

If you trade frequently, conducting some activity within a retirement account may reduce annual tax reporting because transactions inside qualified accounts generally aren’t reported individually on your return.

You may need to keep more cash available for your business or other short-term needs. Some tax-free, tax-deferred and taxable investments offer flexibility, but access to funds can vary. Traditional IRAs and other retirement accounts, for example, may come with taxes or penalties if you withdraw money early. Less liquid assets — including certain real estate investments — can also take longer to sell or convert to cash.

Federal law provides significant protection for certain retirement accounts. ERISA-qualified plans, such as 401(k) retirement plans, generally receive unlimited protection from creditors in bankruptcy proceedings. Traditional and Roth IRAs are protected up to $1,711,975, adjusted periodically for inflation under federal bankruptcy law. State laws may provide additional protections outside of bankruptcy, but these rules vary significantly by jurisdiction.

When income takes a dip, which can happen during the startup phase or slow times, some investors want to rethink how their accounts are taxed. As of 2026, the 12 percent federal bracket covers taxable income up to $50,400 for single filers and $100,800 for married couples filing jointly. In years like these, Roth conversions or stock option exercises sometimes come into the conversation because the tax impact may be lower.

The general rule is to recognize gains and income in years when you have a lower marginal tax rate. You definitely do not want to accept lower investment yields — for example, those from municipal bonds — when you gain little benefit from their nontaxable status.

Some higher-income business owners focus on retirement accounts that allow taxes to be deferred until later. Beyond traditional IRAs, a SEP-IRA can allow contributions of up to 25 percent of compensation, with a maximum of $72,000 for tax year 2026. Solo 401(k)s and similar defined-contribution plans follow the same overall annual additions limit, and employee elective deferrals can reach $24,500, plus an additional $8,000 catch-up contribution for participants age 50 and older. For many investors, these accounts are simply a way to reduce current taxable income while continuing to build retirement savings over time.

Tax-free investments may matter more if you expect to stay in a high tax bracket both while you’re working and after you retire. As your combined state and federal tax rate rises, tax-exempt income can start to look more competitive compared with taxable options. These investments don’t always offer the highest yields, but the tax savings may help narrow that gap for some investors.