Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Taxes and Inflation Calculator

Taxes and inflation are unavoidable, but fortunately this calculator can help you make sure you’re saving enough in your retirement fund.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

One of the main goals of building a retirement portfolio is to maintain purchasing power over time. However, factors like taxes and inflation can erode the future value of your investments. Use our calculator to determine the impact of taxes and inflation on your future purchasing power.

Key Terms

Pretax rate of return

The rate of return refers to how much, on average, the investment is expected to grow each year in percentage terms. Over the long run, United States stock market returns have averaged approximately 10 percent annually before adjusting for inflation. Government bonds have averaged around 4 percent annually over the past decade.

Inflation rate

The inflation rate refers to how much, on average, the prices of goods and services are expected to increase during the specified period. Over the last century, inflation in the U.S. has averaged around 3 percent annually.

Federal marginal tax bracket

The margin tax bracket refers to the highest tax rate that applies to your income. Consult the current federal income tax brackets and rates for your exact percentage.

State marginal tax bracket

This refers to the income tax rate applied by your state government. State tax rates vary widely, from zero percent in states like Florida and Texas to over 13 percent in California for high earners. Check your state’s department of revenue for current rates.

Itemized deductions

With itemized deductions, you add up qualified expenses for the year and subtract them from your taxable income. This differs from the standard deduction, which is a fixed amount set by the IRS every year.

Tip

Business owners should consider diversifying between tax-advantaged retirement accounts and taxable investment accounts. This provides flexibility in retirement to manage your tax bracket by strategically choosing which accounts to withdraw from each year.

How can you shield your retirement portfolio from taxes?

Business owners can leverage investment vehicles like a Roth individual retirement account (IRA) to reduce your tax liabilities. With a traditional IRA, you can contribute up to $7,000 in 2025 (or $8,000 if you’re 50 or older) with pre-tax dollars, and withdrawals are taxed as ordinary income in retirement. With a Roth IRA, contributions are made with after-tax dollars using the same contribution limits, but qualified withdrawals after age 59½ are completely tax-free.

What is purchasing power?

Purchasing power refers to the amount of goods and services that you can buy with one dollar. As the prices of goods and services rise, your purchasing power decreases. Over time, the effects of inflation tend to erode the real value of an individual’s savings. The goal of investment is to preserve (and preferably grow) purchasing power. As long as your investment portfolio’s rate of return matches or exceeds the rate of inflation, you will maintain or grow your purchasing power over time.

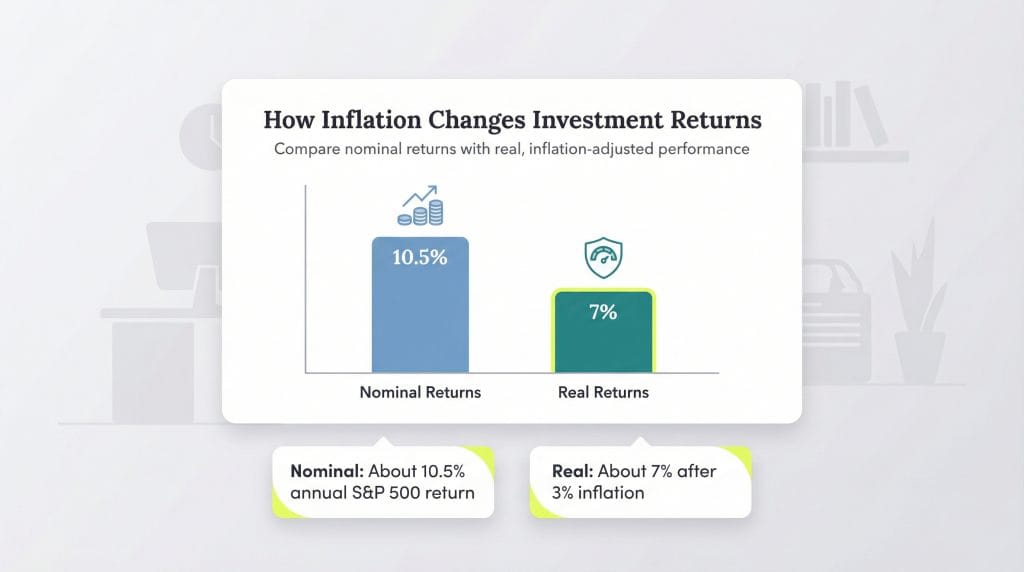

How does inflation affect investment returns?

Over the long run, U.S. stocks (as measured by the S&P 500 index) have returned approximately 10.5 percent annually. However, this number ― often referred to as the “nominal” rate of return ― doesn’t account for inflation’s impact. After adjusting for the historical 3 percent inflation rate, “real returns” for U.S. stocks average around 7 percent annually.

Mike Berner brings to business.com over half a decade of experience as a finance expert, having previously served as an economic analyst for the U.S. Army Corps of Engineers. His expertise lies in conducting quantitative analysis and research, providing invaluable guidance for navigating the modern financial landscape.

Berner, who has a bachelor's degree in economics and a bachelor of business administration in finance, enjoys simplifying complicated financial concepts for entrepreneurs and business owners. From deciphering the intricacies of business loans and accounting to identifying the best payroll systems and credit card processors, he offers comprehensive insights tailored to meet diverse business needs.

At business.com, Berner covers business plans, funding solutions, accounting software, the ins and outs of credit card processing and more.

Beyond dedicating himself to exploring and evaluating the latest financial solutions, Berner has also become adept at explaining how businesses can take advantage of artificial intelligence tools. His passion for sharing knowledge extends to various platforms, including Substack, TikTok and YouTube, where he imparts tips and strategies on topics like sales tactics, savvy investing and tax saving.