Business owners face credit card fees coming and going — when they process customer payments and when they use credit cards for business expenses. These fees can add up to a significant amount every month. Fortunately, many business-related credit card fees are tax-deductible. They’re considered part of the cost of doing business and are classified as business expenses.

On the purchasing side, deductible credit-card-related charges include interest, balance transfer charges and cash advance fees. On the selling side, all credit card processing fees, including percentage-of-sale fees, per-transaction fees, chargeback fees, PCI compliance fees and more are deductible. Here’s what business owners should know about tracking and understanding business credit card fees and maximizing their tax deductions.

Credit card fees explained

The term “credit card fees” generally refers to both the fees imposed by credit card companies and the fees incurred when a business accepts credit card payments. Here’s what’s involved.

Bank credit card fees

Credit card companies assess various fees for business credit cards, either annually or when specific events occur. Here are some examples:

- Annual fees

- Late fees and overlimit fees

- Interest charges

- Balance transfer costs

- Cash advance fees

Credit card fees vary by card and issuer, so it pays to shop around. For example, some cards don’t charge an annual fee, while others charge hundreds of dollars yearly. Interest rates may be two or three times higher on one card than another, and some rewards programs are far more valuable, too. The higher your business credit score, the better a deal you may be able to secure.

Credit card processing fees

When your business accepts credit cards, debit cards and various digital payment methods, you incur processing fees on each transaction — typically about 1.15 to 3.15 percent. Some processors also charge a minimum amount per transaction.

In exchange for processing fees, credit card companies accept liability for instances of credit card fraud, help resolve disputes, and serve as a middleman for card purchases.

Business deductions for credit card fees

According to IRS Publication 535, businesses can deduct 100 percent of credit card fees and interest on cards used exclusively for business purposes. When a business owner uses a personal credit card for work expenses and gets hit with a fee, only the fee percentage related to business spending is tax-deductible.

In addition to credit card fees, businesses can deduct any fees they pay financing institutions — such as interest fees or other expenses — as long as they’re for legitimate business activities. Other deductible banking fees include account charges, check-printing fees, stop-payment fees and wire transfer fees.

Businesses can also deduct the credit card transaction fees they pay as part of accepting credit card payments from customers. (This is represented by the difference between a business’s gross sale amount and the net payment received from its merchant service provider.)

Deduct credit card fees and other expenses in the tax year when they are applied to your credit card statement, regardless of when you pay your credit card bill.

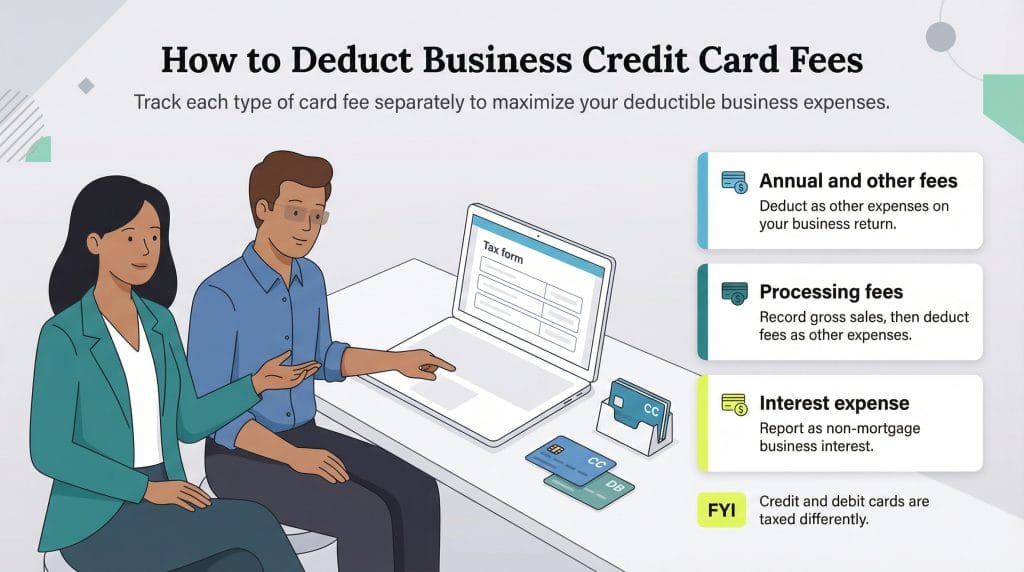

How to deduct business credit card fees on your taxes

Any business can deduct business-related credit card fees on its taxes. Here is where to deduct each type of credit card fee:

- Credit card annual and other fees: Enter all annual credit card fees, overdraft fees, cash advance fees, and other charges paid on cards used exclusively for business as “other expenses” on your business schedule or return.

- Processing fees: Report sales from credit card transactions at the gross amount — before any deductions for processing fees. TurboTax recommends entering gross revenue before fees and then reporting processing fees separately as “other expenses” on your business schedule or return.

- Interest expense: On your business schedule or return, report credit card interest on business debt as non-mortgage interest.

Business credit and debit cards differ. Credit cards can offer rewards and help build your credit score. While traditional debit cards do not build credit, some newer credit-building debit cards can help you start establishing a credit history.

Deducting business vs. personal credit card fees

Businesses can deduct credit card fees and interest — but only if the charges are directly related to the business. Individuals, however, cannot deduct fees or interest on personal credit cards.

Because of potential confusion and penalties, business owners should always use separate credit cards for business and personal expenses. Here’s why:

- Accurate deductions are harder with mixed-use cards. Commingling personal and business expenses makes it difficult to determine which portion of your credit card fees is deductible. If you use one card for both, you can only deduct the percentage of fees and interest that directly relates to business use. For example, if you use a card 50 percent for business, you can deduct 50 percent of the annual fee and other charges as business expenses. You can also deduct 50 percent of the interest as non-mortgage business interest. You cannot deduct the portion that applies to personal use.

- You could lose liability protections. There’s another crucial reason to keep business and personal finances separate and use business credit cards wisely: Combining them could cause you to lose liability protection for your business. Courts may be more likely to “pierce the corporate veil” and hold business owners personally responsible for business debts or legal issues — even if you operate as an LLC or corporation.

- It complicates accounting. Using a dedicated business credit card makes bookkeeping easier and saves time for you and your accountant. You won’t have to sort through mixed transactions and guess which ones were business-related at tax time.

Cashback, free travel and other rewards earned from using credit cards — personal or business — are not considered taxable income.

Common mistakes made when deducting credit card fees

Deducting credit card fees is relatively straightforward: If the expenses are for business use, you can deduct them. If they aren’t, you can’t. However, many people overcomplicate the process. The most common issue? Not keeping business and personal expenses separate.

Here are some of the most common mistakes people make when deducting credit card fees:

- Deducting annual fees for personal cards: Some business owners try to deduct annual fees for personal credit cards they only occasionally use for business. When you use a personal card for mixed expenses, it’s much harder to determine which fees — and how much of them — are actually business-related.

- Deducting credit card interest on a personal return: Because individuals can deduct mortgage interest, they sometimes assume personal credit card interest is also deductible. However, interest on personal credit cards hasn’t been deductible since the Tax Reform Act of 1986.

- Deducting credit card expenses that aren’t allocable to business activities: To claim a deduction, the expense must be directly connected to your business. If you can’t prove that a fee was business-related, it doesn’t qualify.

- Double-deducting processing fees: Some business owners mistakenly report only the net income they receive from their payment processor — an amount that already excludes credit card transaction fees. If you do this, you can’t deduct those fees again. To avoid this, report gross sales before fees are taken out, so your reported revenue aligns with what the IRS sees on Forms 1099-K.

Like all accounting and tax matters, deducting credit card fees is a nuanced process. When in doubt, work with a

tax consultant to keep everything above board and

avoid a tax audit.

Stay organized with your business credit cards

Using a credit card should make accounting for business expenses easier — not harder — if you use it correctly. You’re much less likely to lose track of expenses when you use a dedicated business credit card.

In addition, it’s easy to see at the end of the year how much you spent on credit card fees and interest. Staying organized helps ensure you get the full deduction for your credit card expenses while giving you a clear picture of how much it actually costs to use your card.

Dock Treece contributed to this article.