Access to funding is a persistent hurdle for many small business owners. While managing cash flow, expanding operations, or capitalizing on new opportunities typically requires ready access to capital, traditional business loans are often slow-moving, have strict qualification standards, and can be inflexible. However, many entrepreneurs may already own a powerful financing tool: their home equity.

This article is sponsored by SBG Funding.

One often overlooked strategy is using a Home Equity Line of Credit (HELOC) as an alternative funding solution, allowing business owners to leverage personal assets for business growth.

What is a HELOC?

A Home Equity Line of Credit (HELOC) is a revolving credit line secured by the equity in your home, functioning much like a credit card — you borrow what you need, up to a limit, and repay it over time.

Unlike a home equity loan, which provides a lump sum disbursal with fixed payments, a HELOC allows you to withdraw funds as needed within the “draw period,” then repay during a subsequent “repayment period” which may have higher required payments.

HELOCs typically have variable interest rates, with borrowing limits based on a percentage of your home equity (calculated as your home’s current value minus any outstanding mortgage balances).

You can apply for a HELOC or other form of small business financing with

SBG Funding. Simply answer a few questions about your business and funding needs for more details at no cost or impact to your credit score.

How small business owners use HELOCs

Owners use HELOCs for a variety of business needs, such as:

- Managing cash flow gaps during slow seasons

- Purchasing inventory or business equipment

- Funding renovations or expansion, such as opening a new location or hiring staff

- Launching marketing campaigns or new products

- Covering emergency expenses or repairs

- Bridging funding gaps when waiting on invoices or receivables

For business owners exploring funding options, companies like SBG Funding specialize in helping entrepreneurs understand a range of financing solutions, including strategic home equity use in business.

Example of how a HELOC can be used for business

Here’s a hypothetical example of how a HELOC might be used to fund a small business.

Maria owns a landscaping company that experiences strong seasonal demand from March through October but limited revenue during winter months. When a competitor went out of business in February, she had an opportunity to acquire $35,000 worth of equipment at a significant discount, but she needed to act quickly.

Rather than taking out a traditional business loan with immediate fixed payments during her slow season, Maria used her HELOC to purchase the equipment. During the low-revenue winter months, she made only the interest payments. Once her busy spring season began and revenue picked up, she started making larger payments toward the principal, ultimately paying off the balance within 18 months.

The HELOC’s flexibility allowed Maria to capitalize on a time-sensitive opportunity while managing cash flow through her seasonal business cycle.

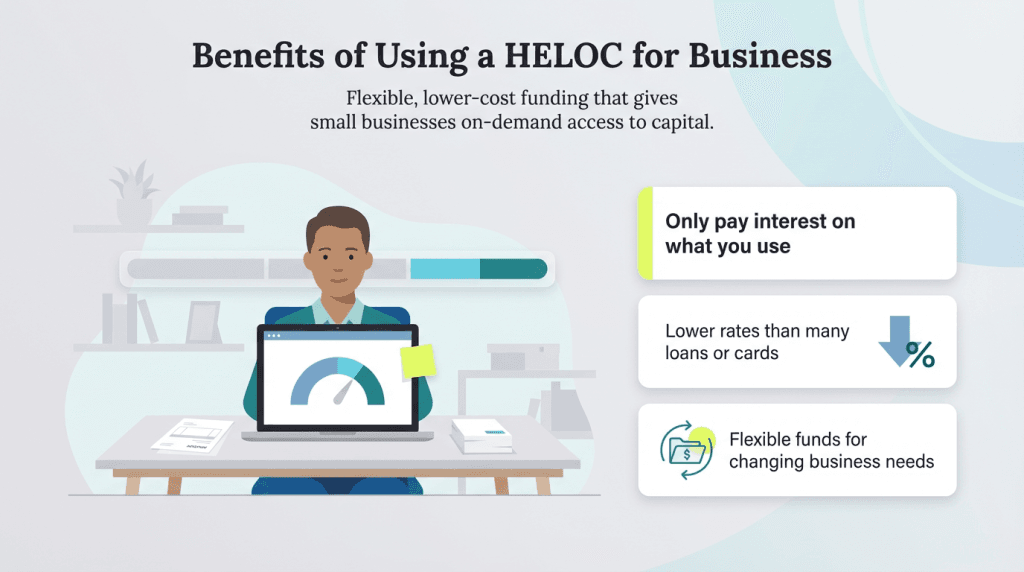

The benefits of using a HELOC for business

Flexibility

A key advantage of a HELOC lies in its flexibility, which lets small business owners draw only the amount needed at a specific time, paying interest solely on what they’ve used rather than the entire credit line. This revolving nature means that as you repay the borrowed amount, you can re-borrow up to your approved limit during the draw period, providing ongoing access to funds for unpredictable business demands.

Lower interest rates

HELOCs generally come with lower interest rates compared to unsecured business loans or business credit cards, thanks to the security provided by your home as collateral, making it a cost-effective option for funding growth without the higher costs of alternative borrowing methods.

Easier qualification

Qualification for a HELOC often focuses more on your home equity and personal credit score than on your business’s credit history alone, which can make it accessible for newer businesses that haven’t built up established business credit yet. This approach can also lead to faster loan approval processes than many traditional business loans, helping owners get capital when they need it most.

No restrictions on use

Unlike some business loans that dictate how funds must be spent, HELOCs typically impose no such limitations, allowing you the freedom to direct the money toward your highest-priority business needs, whether that’s inventory, marketing or unexpected expenses.

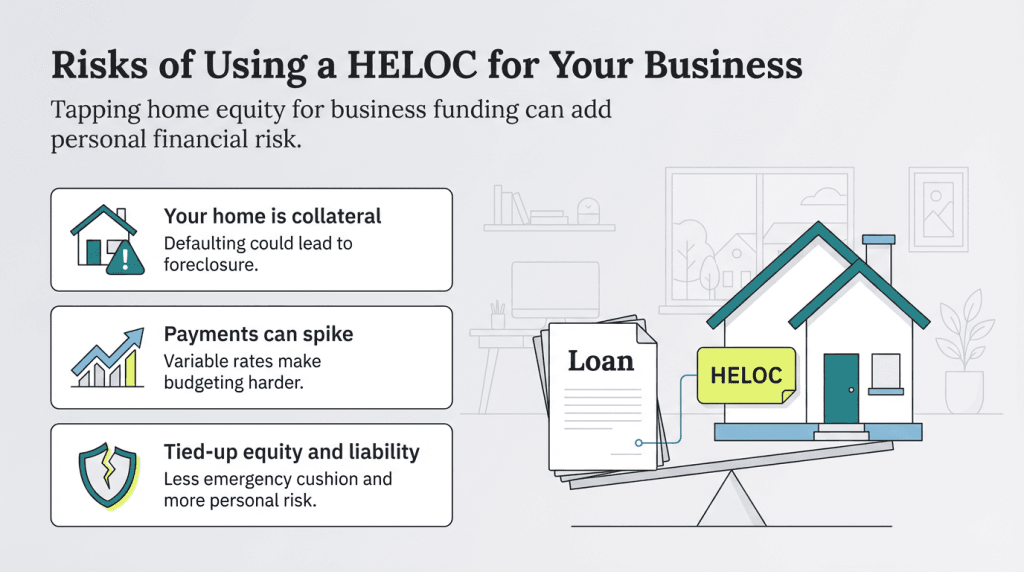

Drawbacks and risks of using a HELOC to fund your business

Your home is collateral

When you use a HELOC for business funding, your home serves as collateral, meaning defaulting on loan payments could lead to foreclosure and the loss of your primary asset. This arrangement also mixes personal and business finances, underscoring the need for a solid repayment plan to avoid jeopardizing your family’s stability.

Variable interest rates

HELOCs often feature variable interest rates that can rise over time, leading to higher monthly payments and making long-term budgeting more challenging compared to fixed-rate options. These fluctuations can catch business owners off guard, especially during periods of economic uncertainty when rates might increase unexpectedly.

May reduce personal financial security

Borrowing against your home equity diminishes the amount available for other personal or emergency needs, potentially limiting your future borrowing capacity if you need funds for non-business purposes. Additionally, if the housing market experiences a downturn, the value of your home could drop, leaving you with less equity and greater financial vulnerability.

Not ideal for long-term financing

With draw periods usually spanning five to 10 years followed by repayment phases that demand larger principal and interest payments, a HELOC is better suited for short-term or cyclical business needs rather than ongoing, long-haul investments. This structure can create cash flow pressures once the draw phase ends, requiring careful planning to avoid strained finances.

Personal liability

Even if your business operates as an LLC or corporation, a HELOC places personal liability on you as the borrower, with your home at risk regardless of your business’s legal structure. Lenders typically require a personal guarantee for approval.

Who should consider a HELOC for business?

Ideal candidates for a HELOC include:

- Established business owners with reliable revenue streams

- Owners with significant remaining home equity (usually 15% to 20% or more)

- Entrepreneurs operating seasonal businesses that need working capital flexibility

- Those who can’t obtain traditional business financing or want a faster alternative

- Businesses with predictable income to service the debt

A HELOC is generally not appropriate for:

- Very new businesses without proven revenue

- Owners with irregular or unstable income

- Anyone already financially stretched or needing capital long-term

- Those uncomfortable intertwining personal and business finances

The best business loan providers work with business owners to help determine if a HELOC or another solution is the best fit for their situation and long-term goals.

Key considerations before applying

Before pursuing a HELOC for business funding, start by calculating your available home equity and determining a realistic borrowing amount to ensure you don’t overextend. It’s crucial to assess your business’s capacity to cover payments even during slower periods, while also shopping around to compare interest rates, terms, and fees from various lenders for the best deal. Beyond that, weigh alternatives like SBA loans, business lines of credit, or equipment financing, and seek input from professionals — such as an accountant for tax implications or a financial advisor for overall risk evaluation — while developing a detailed plan for fund usage, repayment, and maintaining a buffer by avoiding maximum borrowing.

Alternative financing options to consider

If a HELOC isn’t the right fit, other business funding options include:

- SBA loans: SBA loans offer long repayment terms and favorable rates for qualifying businesses.

- Business lines of credit: These products provide revolving capital without using your home as collateral.

- Equipment financing: This option is ideal for purchasing necessary assets without tying up personal equity.

- Invoice factoring: A financing option which advances cash based on your accounts receivable.

- Business term loans: Conventional financing that provides a lump sum for major expenditures.

Not sure what type of loan would suit your business best? Check out our guides comparing: