This article is sponsored by Intuit.

Every small business owner knows the feeling: a client’s invoice is 30, 60, sometimes 90 days past due, and the money you were counting on to cover payroll or restock inventory is still nowhere in sight. It’s easy to write this off as a routine annoyance of running a business, but late payments carry real, compounding costs that touch nearly every part of a company’s operations.

Data from Intuit QuickBooks suggests small businesses with outstanding invoices are currently owed $17,500 on average. For many small businesses, it’s the difference between hiring the next employee, taking on new inventory or simply making payroll on time. Beyond the balance sheet, late payments are quietly linked to higher borrowing costs, stalled technology upgrades and even hiring slowdowns.

How common are late payments for small businesses?

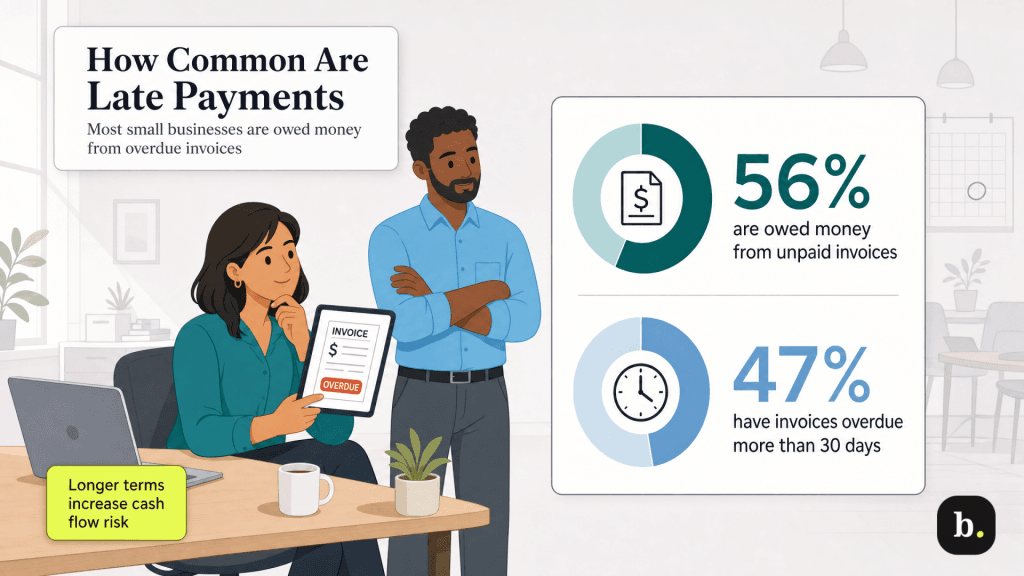

Late payments are, unfortunately, the norm for a majority of small businesses. According to the 2025 Intuit QuickBooks Small Business Late Payments Report, a survey of nearly 2,500 U.S. small businesses with up to 100 employees, 56 percent of small businesses reported being owed money from unpaid invoices, with an average of $17,500 outstanding per business. Almost half (47 percent) said a portion of their invoices were overdue by more than 30 days.

Longer payment terms make the problem worse. The same research found that small businesses with 90-day payment terms were considerably more likely to report cash flow problems than those with immediate payment terms. In other words, the payment terms a business agrees to upfront play a real role in how exposed that business is to cash flow strain down the line.

For small businesses operating on thin margins, late payments can have serious consequences. A single large client paying 60 or 90 days late can be the difference between a business comfortably meeting its obligations and one scrambling to cover a shortfall.

The direct financial cost of late payments

The most obvious cost of a late payment is the cash flow gap it creates. When money that’s owed to a business doesn’t arrive on schedule, that business still has its own bills to pay, like rent, payroll and supplier invoices. The Intuit QuickBooks research found that small businesses that were affected by late payments were more likely to rely on credit cards, lines of credit and loans to bridge the gap: 54 percent used business credit cards over the past year, compared to 46 percent of businesses less affected by late payments, and 31 percent used a line of credit, compared to 21 percent. Those more affected by late payments also carried significantly higher credit card balances relative to their limit than businesses that were paid more reliably.

Carrying that kind of revolving debt means incurring interest charges that compound over time. As a result, a business that regularly leans on credit to cover payment gaps is effectively paying extra just to stay afloat; that’s money that could otherwise go toward growth. And the same research found small businesses more affected by late payments were nearly twice as likely to be considering further price increases, suggesting some businesses are passing at least part of this cost on to customers.

A clear

invoice management and payment policy can help prevent the cash flow gaps that lead to costly credit reliance. Learn more about setting effective payment terms in our complete guide.

The hidden costs of late payments

Beyond the direct financial hit, late payments create a set of quieter costs that are easy to overlook, but no less damaging over time.

- Lost time. Chasing down a late payment takes time that could otherwise go toward serving customers or growing the business. Every follow-up email, phone call or awkward conversation about an overdue invoice is time an owner or employee isn’t spending on higher-value work.

- Strained relationships. Following up on a late payment can be uncomfortable, especially with long-standing clients or vendors. Business owners often have to weigh the relationship against the money owed, which can lead to avoiding the conversation altogether and letting the balance grow.

- Stalled growth and technology investment. The QuickBooks data shows a clear pattern: small businesses more affected by late payments had meaningfully lower adoption of digital tools across the board, including accounting software, business websites, ecommerce, and cloud services, compared to businesses less affected by payment delays. When cash is tied up in unpaid invoices, it’s not available to invest in the tools that help a business run more efficiently or reach new customers.

- Hiring slowdowns. Perhaps the least obvious cost is the effect on staffing. Small businesses facing significant payment delays were more likely to report difficulty hiring skilled workers than those less affected by late payments, a gap that widened further among businesses with longer payment terms. When cash flow is uncertain, expanding the team becomes a much bigger risk.

Taken together, these hidden costs show why the true price of a late payment

Businesses with 90-day payment terms put a larger share of their monthly expenses on credit cards, on average, than businesses with immediate payment terms, according to Intuit QuickBooks research.

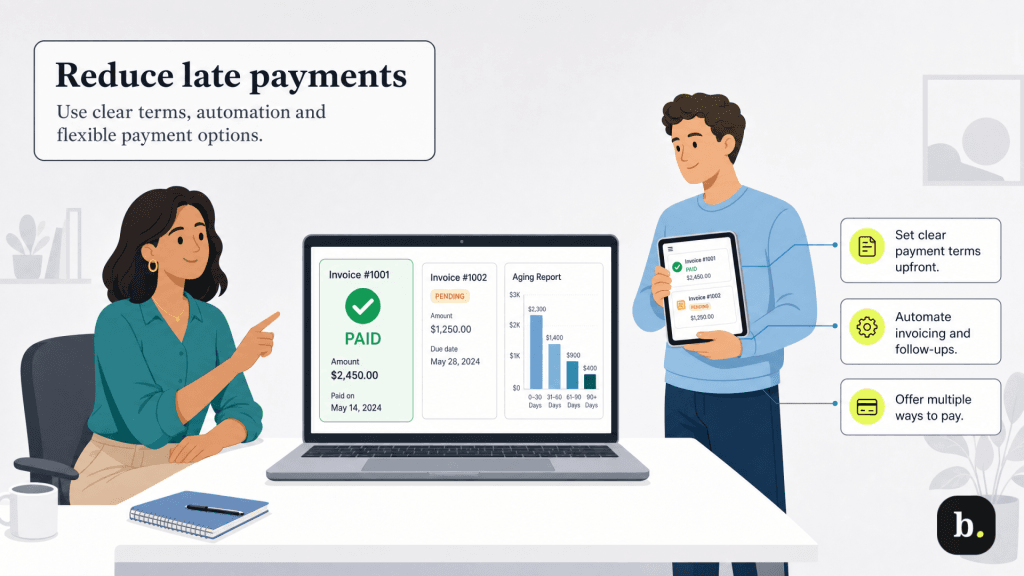

How to reduce late payments and protect cash flow

While it’s not realistic to eliminate late payments entirely, small businesses can take steps to reduce how often they happen and limit the damage when they do.

- Set clear payment terms upfront. Spell out due dates, accepted payment methods and any late fees in every contract or estimate before work begins. Ambiguity around payment expectations is one of the easiest things to fix.

- Consider deposits for larger jobs. Requiring a partial payment upfront, especially for larger projects, reduces how much of a business’s cash flow is tied up in a single unpaid invoice.

- Automate invoicing and follow-ups. Manually tracking who owes what and when is time-consuming and error-prone, especially as a business grows. Accounting software like QuickBooks Online can automatically send invoices, schedule payment reminders and flag overdue accounts so nothing slips through the cracks. QuickBooks Online also lets businesses build an aging accounts receivable report at a glance, making it easier to spot which clients are chronically late before the pattern becomes a bigger cash flow problem.

- Offer multiple payment options. The easier it is for a customer to pay, the faster they’re likely to do it. Accepting multiple payment options, including ACH transfers, credit and debit cards, and digital wallets, removes friction that can otherwise delay payment.

- Monitor accounts receivable regularly. Reviewing outstanding invoices on a weekly basis, rather than waiting until the end of the month, makes it easier to catch and address late payments before they pile up.

Looking for more ways to keep your books in order? Check out our picks for the

best accounting software for small businesses.

Minimize late payments to keep your business growing

Late payments are common, but that doesn’t mean small businesses have to absorb their full cost. The direct hit to cash flow is only part of the picture; the ripple effects on borrowing costs, technology investment and hiring can shape a business’s trajectory long after a single invoice goes unpaid. Businesses that build clear payment policies, monitor receivables closely and lean on tools that automate invoicing and reminders are better positioned to keep overdue payments from becoming a drag on growth.