Financing a small business can be approached from multiple directions. It’s important to understand what the market offers you and how to use those deals to their full potential. This initial stage in your company’s development is crucial to its long-term success.

A credit card is one of the more popular methods for financing a small business, but it comes with a few caveats that you should consider carefully. Most importantly, it’s not the exact same thing as a small business loan, and it has some different implications that you’ll need to be aware of.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

The basics of using a business credit card

Using a credit card to finance your small business should be treated no differently than a regular loan. You have to think carefully about your ability to repay the money and keep your balance in check.

However, credit cards can provide you with a lot more in the way of floating resources. They make it easy to get a smaller amount of cash when you need it. This practice helps you keep your balance in the positive while you’re waiting to get paid.

“Using a credit card to finance a business offers speed and convenience,” said Inbar Madar, founder at M.I. Business Consulting. “You can access funds immediately, without the lengthy approval process of a traditional loan. Many business credit cards also come with rewards, cashback, and short-term, interest-free financing if you pay off the balance within the billing cycle.”

In fact, most modern businesses rely heavily on perpetually open lines of credit. This is valid for pretty much all sectors of the market, including larger companies. With that in mind, you should definitely not be afraid to rely on a credit line to supplement your cash flow. It might be the best option you have in many cases. For example, if you rely on loans and some of your clients are late with their payments, unpaid invoices can affect your operations. But that doesn’t have to be the case if you can cover the negative balance with the help of a credit card.

Personal credit cards vs. business credit cards

Technically, you don’t need a business credit card to run your small business. You can use a personal credit card to handle business expenses, but you may be robbing yourself of potential financial benefits for your business.

“A SMB owner doesn’t have to go get a business loan or a line of credit,” said Nate Marshall, SVP and Regional Market Executive at Civista Bank. “A personal credit card [can be used as] seed money for your business.”

One of the biggest benefits to using a business credit card is building business credit. If you use a personal credit card for business expenses, you’re building personal credit, not business credit. Business credit is an important part of your business’s overall financial picture; without it, it may be harder to get a loan.

Another important aspect to consider is financial benefits. By signing up for and using a business credit card, you receive financial perks and benefits associated with that card. These perks include rewards programs and free cards for your employees, should you give them the financial power of a business credit card.

Most importantly, though, using a business credit card helps streamline accounting. “One thing I always tell entrepreneurs is to keep personal and business finances separate,” said Sami Andreani, chief financial officer at Oppizi. “…Business credit cards are designed for this purpose. They make it easier to track expenses and build your business credit and often come with benefits that are more useful for businesses, like higher spending limits and tools to manage spending.”

Many business credit cards require a minimum personal credit score of 700 or higher for approval.

Things to keep in mind about using credit cards

The market is full of business credit card offers, so don’t feel rushed to apply for the first one you see. Rather, take your time and compare them properly. Pay special attention to the perks they offer, and consider whether they would be useful for your business.

Talk to the different issuers and make sure that you get the full picture regarding what each card can do for you. This is especially true if you’re planning to have multiple lines of credit open. Here are six additional pointers for using credit cards to finance your business.

1. Negotiate for better terms.

Credit card deals are open for negotiation for the most part, and you can often get better terms if you have good credit. If you’re taking out a personal credit card, pay attention to your credit score. This will be a critical factor in negotiating better terms for the card, and it may even unlock special deals that are not normally available.

Have a list of the points or terms you want to discuss when you speak with the credit card issuer. If you can point out some specific information regarding the growth of your business, you should definitely bring that up.

2. Make timely payments.

The importance of paying on time cannot be overstated when it comes to using credit cards for the needs of your business. Before charging any expenses on your card, you have to be absolutely sure that you’ll be able to cover the balance without any issues. Otherwise, you are going to run into some significant debt problems with your company; they might be bad enough to bring down your entire operation.

“If you’re not responsible to pay [down your credit balance], it becomes part of the business expense and continues to trail instead of growing the business,” Marshall said.

Make a budget to ensure that your business is operating within its means. (You can use a budget template so you don’t have to start from scratch.) Use the budgeting tools in your accounting software to help you keep track of your financial streams and to notify you when payments are due. Never lose sight of your financial big picture, because the entire future of your company is tied to your success here. [Read related article: The Best Accounting and Invoice-Generating Software for 2025]

3. Correct problems immediately.

Problems are going to come up in your finances no matter what — it’s actually going to happen quite often. You need to get used to this fact and start preparing to deal with issues promptly. Otherwise, the problems will compound, and you’re going to feel stuck.

Whether it comes from the business side or your own personal finances, it doesn’t matter. The point is that you need to be on top of these issues and ensure that they’re resolved as quickly as possible.

If you need a credit card to fund a major purchase, look for a card that offers an introductory 0% APR. During the introductory period, you can carry a balance without accruing interest charges. For more information on credit possibilities, see our

Best Business Loan and Financing Options guide.

4. Always watch for better deals.

Even if you’re satisfied with your current credit card, you should never underestimate the market’s potential to surprise you with more attractive deals. Credit card companies are always looking to entice new customers, and you will find a plethora of deals to browse through if you haven’t checked in a while.

“Compare what’s out there. Look at the interest rates, fees, rewards and any extra features,” said Andreani. “Some cards work better depending on how you run your business. For example, if you travel a lot, you might want a card with travel rewards. If you make big purchases regularly, cashback cards with high limits could be better. The key is to find one that fits how your business operates.”

Definitely set some time aside to see what’s available to make sure you’re getting a good deal. This is just one part of running your business properly. Staying in touch with current market trends applies not just to your own individual market but also to the financial world as a whole.

5. Track your usage over time.

We already touched on this above, but it’s an important point to reiterate: You should pay attention to your credit card usage habits over time. Don’t just trust your instincts on this. Make sure that you’re working with hard data and that you understand exactly how your finances have shifted over time.

There are various tracking tools available that can help you get this job done easily and without having to do a lot of mental work. Applications powered by AI can be particularly useful; they can help you identify patterns in your expenses and inflow that would normally not be that obvious. This data can help you make informed decisions as your business grows.

6. Talk to your card company if your situation changes.

You should be open with your credit card company with regard to your financial situation as it changes — even if it’s changed for the worse. You’ll often find that credit card companies are much more open to negotiations than you’d expect. They have an active interest in helping you repay them, because your profit is directly tied to their own.

It may take a while to decide if using credit cards as a line of credit is the right move for your small business. Take time to make sure you understand the terms and perks of the cards you apply for. As long as you’re able to fully repay the amounts you charge on your business credit cards, you shouldn’t run into any significant financial problems with them down the line.

Best credit cards to start a business

There are many different credit cards to choose from, and your company’s financial situation will dictate which card is best for your business. Keep in mind your credit score and financial history — both personal and business-related — will be considered when applying for these cards.

Here are some popular business credit card options to consider:

- Capital One Spark 1% Classic: For new and emerging businesses, this is a good credit card option for building credit. It has a $0 annual fee, unlimited 1% cash back on all business purchases and flexible employee access.

- Capital One Spark 1.5% Cash Select: This card is a great option for small business owners looking to take advantage of cash back rewards. You’ll earn unlimited 1.5% cash back rewards on all purchases, and you’ll receive a one-time $500 bonus if you spend $4,000 within three months of opening the account. And like the Spark 1% Classic, there’s no annual fee.

- Chase Ink Business Preferred Credit Card: If you want to take advantage of travel rewards and other purchasing perks, this card is a great option for small businesses. Cardholders can earn 90,000 bonus points after spending $8,000 on purchases in the first three months. You’ll earn 3X points on the first $150,000 you spend on combined purchases of travel, shipping, internet, cable and phone purchases. It also applies to advertising purchases made on social media sites and search engines. The card does come with a $95 annual fee, though.

Before you start shopping around for business credit cards, know what specific features you’re looking for in a card. For instance, are you looking to maximize travel rewards or do you want to avoid an annual fee? Knowing this information will help you refine your search and find the right card.

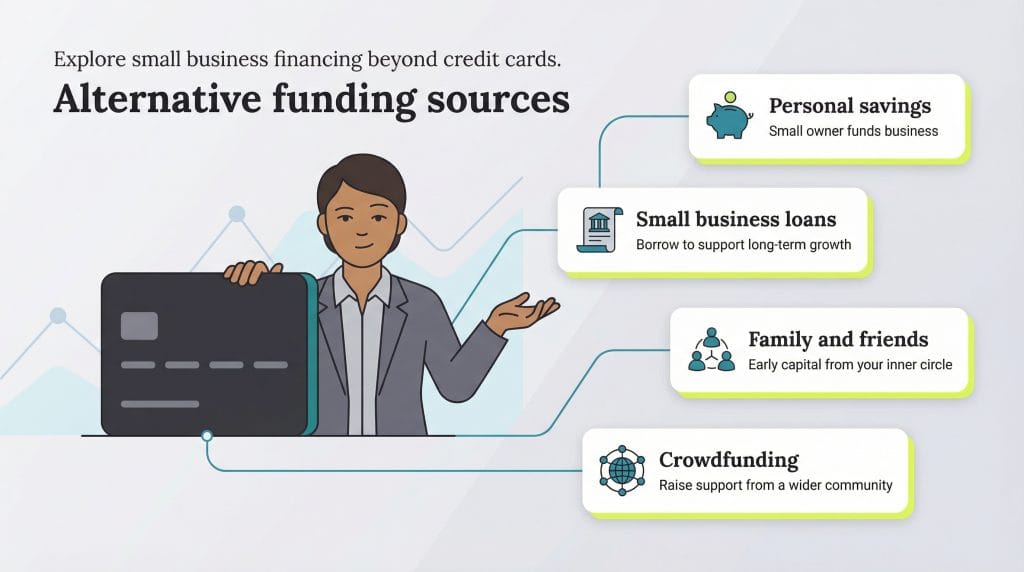

Alternative funding sources

You should also consider your other options before resorting to a credit card as a default choice of financing. As Andreani explained, credit cards work well in certain — but not all — situations. “A credit card can be a helpful tool, but it’s not the answer to every financial need,” he said. “It works well for managing cash flow or covering short-term costs, but if you’re planning something bigger, you’ll need to explore other options.”

Some of these other financing options include:

- Personal savings: Oftentimes, small business owners leverage personal assets to fund their business. This can be a good option when you’re just starting out or if a financial emergency occurs.

- Small business loans: A major source of funding for small businesses is business loans. Loans are the backbone of many small businesses, and having a good relationship with a community bank can provide a stable financial future for your company.

- Family and friends: Much like with relying on personal finances, small business owners will often seek funding from family and friends. This is especially true during the early days of a small business.

- Crowdfunding: Instead of seeking funding through traditional avenues, some small business owners elect to create profiles on crowdfunding websites to raise capital.

Credit cards for small businesses: one of many financing options

Is a business credit card the right choice for your financing needs? Only you can answer that. It all depends on your unique circumstances, from ensuring you have the cash flow for on-time payments to finding rewards that actually serve your business. If it seems like the best choice for your organization, a business credit card could be the solution to your short-term financial demands.

Natalie Hamingson and Jamie Johnson contributed to this article.