Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Open a Business Bank Account Without an EIN

Can you really open a business bank account when you don't have a federal tax ID? Here's what entrepreneurs need to know.

Written by: Skye Schooley, Senior Lead AnalystUpdated Jan 27, 2026

Editor Verified:

Editor Verified

A business.com editor verified this analysis to ensure it meets our standards for accuracy, expertise and integrity.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

When you’re launching a business, setting up a separate bank account to keep personal and business finances apart is one of the smartest moves you can make. But what if you don’t have an employer identification number (EIN) yet – or you’re wondering whether you even need one? The short answer is that yes, you often can open a business bank account without an EIN, especially if you’re a sole proprietor. However, the rules vary widely by bank and business structure, and understanding the nuances can save you time, headaches and potentially open up better banking options down the road.

Can I open a business bank account without an EIN?

Yes, you can open a business bank account without an EIN in many cases, particularly if you’re a sole proprietor or sometimes even a single-member limited liability company (LLC). Instead of an EIN, the bank will typically ask for your Social Security number (SSN) or individual taxpayer identification number (ITIN) to verify your identity and meet federal know-your-customer (KYC) requirements.

That said, bank policies differ. Some financial institutions welcome sole proprietors who use their SSN, while others require an EIN regardless of your business structure. Multi-member LLCs, partnerships and corporations almost always need an EIN because the Internal Revenue Service (IRS) classifies them as separate tax entities. Before you head to a branch or start an online application, confirm the current policy with the specific bank you’re considering.

Tip

Call the bank's business banking team or check the account-opening checklist on their website to confirm whether they accept SSN or ITIN in lieu of an EIN for your entity type.

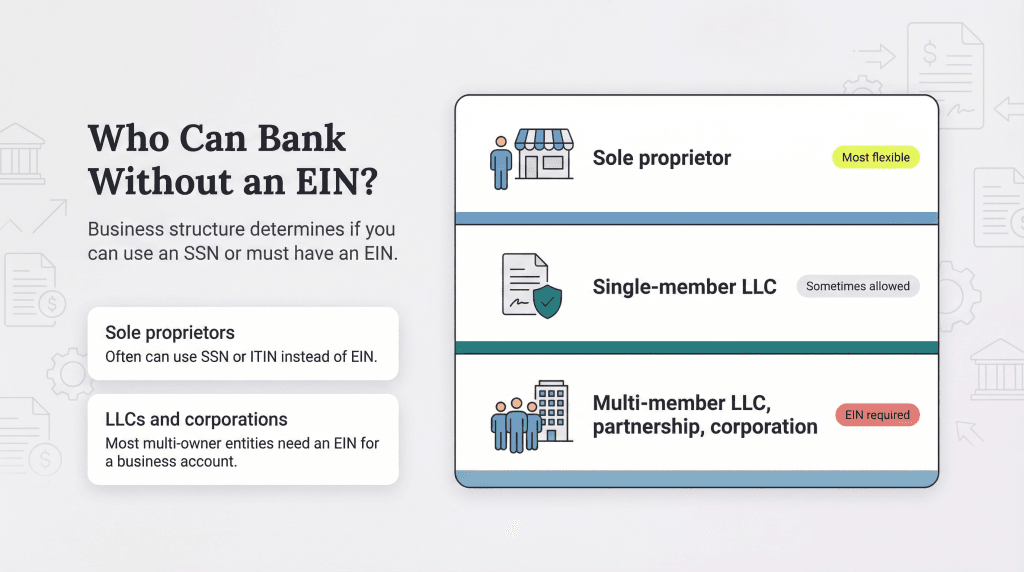

Who can (and can’t) bank without an EIN?

Whether you can skip the EIN depends almost entirely on how your business is legally organized. Here’s a quick breakdown by entity type.

Sole proprietors

Sole proprietors are the most likely candidates to open a business account using just an SSN or ITIN. Because a sole proprietorship isn’t a separate legal entity (i.e., it’s simply you doing business under your own name or a trade name) many banks treat the account as an extension of your personal banking relationship. You’ll still need to prove you’re conducting legitimate business activity, but an EIN isn’t mandatory at most institutions.

According to the U.S. Census Bureau, nonemployer firms (primarily sole proprietorships) accounted for roughly 27.9 million businesses in recent data, making this the most common structure among new entrepreneurs. If you’re in this group and don’t yet have employees or a partnership, the SSN route is often the simplest path forward.

Single-member LLCs

Single-member LLCs occupy a middle ground. For tax purposes, the IRS treats a single-member LLC as a “disregarded entity” by default, meaning income and expenses flow through to your personal return using your SSN. Some banks recognize this and allow you to open an account with your SSN, especially if you’re operating under your personal name.

However, many banks still prefer or outright require an EIN for LLC accounts, even when you’re the sole member. The reason is risk management: banks want a clean separation between personal and business liability, and an EIN reinforces that distinction. Always verify the policy before applying, and be prepared to obtain an EIN if the institution insists on it.

Multi-member LLCs, partnerships and corporations

If your business has more than one owner – whether it’s a multi-member LLC, a general or limited partnership, or any type of corporation (C-corp or S-corp) – you will almost always need an EIN. The IRS requires these entities to file separate tax returns, and banks follow suit by requiring a federal tax ID for account opening. There’s no workaround here: plan to apply for an EIN before you start shopping for business accounts.

Bottom Line

Sole proprietors typically have the most flexibility to use an SSN or ITIN instead of an EIN; single-member LLCs sometimes do; and multi-owner entities almost never can skip the EIN.

Banks that may accept SSN/ITIN (no EIN) for sole props

A growing number of online and traditional banks understand that sole proprietors and some single-member LLCs want to get started quickly without waiting for an EIN. While we can’t endorse specific institutions (policies change frequently and vary by state), several well-known national and regional banks have historically allowed business account applications using an SSN or ITIN for qualifying sole proprietorships.

Examples of institutions that have offered this option in the past include large national banks with robust online platforms, community banks focused on local small-business lending and digital-only business banks designed for freelancers and gig workers. The key is to confirm the current requirements directly with the bank before you apply. Ask specifically:

Do you accept SSN or ITIN for sole proprietor business accounts?

What additional documents will I need to provide?

Are there any restrictions on account features if I don’t have an EIN?

Keep in mind that even when a bank accepts your SSN, you may face limitations; for example, lower transaction limits, fewer integrations with accounting software or requirements to upgrade to an EIN-backed account if you later add employees or incorporate.

Did You Know?

According to the Small Business Administration, there were nearly 34.8 million small businesses in the United States as of 2024, and the vast majority start as sole proprietorships.

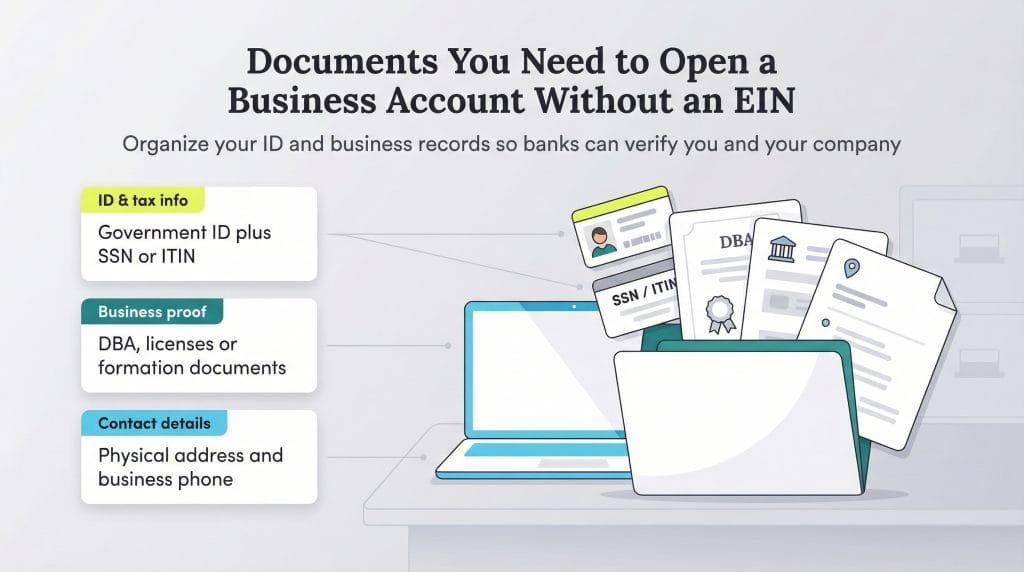

What documents do I bring if I don’t have an EIN?

Opening a business account without an EIN doesn’t mean you can walk in empty-handed. Banks still need to verify your identity, comply with federal anti-money-laundering rules and confirm that your business is legitimate. Here’s what you should gather before you apply.

Government-issued identification: You’ll need a valid driver’s license, state ID or passport. If you’re a non-U.S. citizen, an ITIN and passport are typically acceptable. The bank will photocopy or scan these documents as part of their KYC process.

Social Security number or ITIN: This is your tax identifier in lieu of an EIN. The bank will use it to run credit checks (if applicable) and report interest or other taxable activity to the IRS. Make sure you have the number memorized or written down securely.

Doing-business-as (DBA) certificate or fictitious name filing: If you operate under a trade name, such as “Lopez Landscaping” instead of “Maria Lopez”, most banks require proof that you’ve registered that name with your county or state. This is usually a DBA certificate or fictitious business name statement. If you’re simply using your legal name for business, you may not need this.

Formation or ownership documents: Even as a sole proprietor, some banks ask for proof of business existence. Some examples include a business license, professional license or articles of organization if you’re a single-member LLC. Have digital and physical copies ready.

Business address and contact information: You’ll need to provide a physical business address (a P.O. box often isn’t sufficient for the primary address) and a phone number. If you work from home, that’s usually fine, just be prepared to explain your business model if asked.

Tip

Organize all your documents in a dedicated folder – both digital and physical – so you can grab them quickly whether you're applying online or visiting a branch in person.

Why getting an EIN anyway is a smart move

Even if a bank will let you open an account with just your SSN or ITIN, there are compelling reasons to apply for an EIN before you start banking. The process is free, fast and can unlock significant advantages as your business grows.

Privacy and security

When you use your SSN for various business purposes, you’re exposing your personal identifier over and over again. An EIN functions as a firewall, keeping your SSN out of the hands of third parties and reducing the risk of identity theft. If a vendor’s system is breached, your EIN is compromised, not your Social Security number.

More banking options and better features

Many premium business accounts, credit cards and lending products require an EIN. If you want access to higher transaction limits, integration with payroll services or the ability to add authorized signers, an EIN often opens those doors. Starting with an EIN also means you won’t have to re-apply or re-paper your account later when your needs evolve.

Preparing for employees and growth

The moment you hire your first employee – even a part-time contractor in some cases – you’ll need an EIN to withhold payroll taxes and file employment tax returns. If you’re planning to grow, it’s easier to set up your banking infrastructure with an EIN from the start rather than switching mid-stream.

Building business credit

Establishing a credit profile separate from your personal credit often requires an EIN. Business credit bureaus like Dun & Bradstreet and Experian track your company’s payment history and creditworthiness using your EIN. A strong business credit score can help you secure better loan terms, net payment terms with suppliers and lower insurance premiums.

Speed and simplicity of the application

Applying for an EIN through the IRS online EIN application is free and typically takes less than 15 minutes. You’ll receive your EIN immediately upon completion if you apply online during business hours. There’s no fee, no waiting period and no downside, making it one of the easiest administrative tasks you can check off your startup to-do list.

Bottom Line

An EIN is free, fast and future-proofs your business banking, hiring and credit-building efforts, even when it's technically optional.

How to decide whether to use SSN or get an EIN

Still on the fence? Here’s a quick decision framework to help you choose the right path based on your situation.

Use the SSN or ITIN route if:

You’re a sole proprietor with no employees and no immediate plans to hire.

You need to open a business account today and can’t wait for any administrative delays.

The bank you prefer explicitly accepts SSN or ITIN for your business structure.

You’re running a very small side business or freelance operation and want minimal paperwork.

Get an EIN first if:

You’ve formed an LLC (even single-member) or any corporation.

You plan to hire employees or independent contractors in the near future.

You want maximum privacy and prefer not to share your SSN with multiple vendors and institutions.

You’re shopping for business credit cards, lines of credit or other financial products that require an EIN.

You want the widest range of banking options and aren’t concerned about spending 15 minutes on an IRS application.

In most cases, we recommend getting the EIN even if it’s optional. The upfront effort is minimal, and the long-term flexibility is worth it. That said, if you’re truly in a time crunch and meet the criteria for SSN-based banking, it’s a viable short-term solution. Just be prepared to revisit the decision as your business evolves.

FAQs about opening a business account without an EIN

No. Banks still require government-issued ID for all account owners, along with business formation documents, a business address and sometimes a DBA certificate or business license to satisfy KYC regulations.

Some banks accept an ITIN in place of an SSN for non-U.S. citizens, but policies vary widely. Check with individual institutions and be prepared to provide a passport and proof of U.S. business activity.

Oftentimes, yes. Many banks offer fewer account types, lower limits and less robust features for SSN-based accounts, and you may need to re-apply or upgrade your account if you later obtain an EIN.

If you apply online through the IRS website during business hours, you'll receive your EIN immediately; paper and fax applications can take several weeks to process.

Skye Schooley is a dedicated business professional who is especially passionate about human resources and digital marketing. For more than a decade, she has helped clients navigate the employee recruitment and customer acquisition processes, ensuring small business owners have the knowledge they need to succeed and grow their companies.

At business.com, Schooley covers the ins and outs of hiring and onboarding, employee monitoring, PEOs and HROs, employee benefits and more.

In recent years, Schooley has enjoyed evaluating and comparing HR software and other human resources solutions to help businesses find the tools and services that best suit their needs. With a degree in business communications, she excels at simplifying complicated subjects and interviewing business vendors and entrepreneurs to gain new insights. Her guidance spans various formats, including newsletters, long-form videos and YouTube Shorts, reflecting her commitment to providing valuable expertise in accessible ways.