Most business owners pick their first bank based on convenience. Perhaps it was nearby, it was the bank they already used personally or it was the first one that would approve their account. That’s a perfectly reasonable way to get started, but the bank that worked when you were processing a handful of transactions per month may not be the right bank once you’re managing payroll, vendor payments, recurring subscriptions and a growing revenue stream.

Switching business banks isn’t something most people look forward to, but it’s also not the ordeal most people assume it is. Knowing when to make the move and how to do it without disrupting your operations can save you real money and eliminate friction you may have been tolerating for longer than you should.

Why business owners hesitate to switch banks

The biggest reason business owners stay with a bank that no longer serves them well is inertia. And it’s understandable. Your bank account is wired into nearly every aspect of your business operations: auto-payments pull from it, direct deposits flow into it, your payroll provider is linked to it, your merchant services processor deposits revenue into it and your accounting software reconciles against it. The thought of untangling all of those connections often feels overwhelming.

There’s also the comfort of familiarity. You know the bank’s systems, you may have a relationship with a branch manager and the account “works” in the sense that nothing is actively broken. But working and working well are two different things. Inertia has a cost, whether that’s in the monthly fees you’ve stopped questioning, the manual workarounds you’ve built because the bank’s technology can’t keep up, or in the lending opportunities you’re missing because your bank doesn’t offer the products you need.

If you’ve been putting off switching banks but think it’s time to find a new partner, consider our picks for the

best business bank accounts. These service providers offer banking solutions for companies of all sizes and include scalable options that can grow alongside your business.

Clear signs it’s time to switch

Not every frustration with your bank warrants a switch. But certain patterns, especially when they’re persistent and measurable, signal that the relationship has run its course.

Fees are eating into your margins

Bank fees are easy to ignore because they arrive in small, predictable increments. A $15 monthly maintenance charge, a $0.50 per-transaction fee and a cash deposit surcharge that kicks in after your first $5,000 may not feel like a lot on their own. But, taken together and over time, they can add up to hundreds or even thousands of dollars per year.

To get a clear picture, pull your last three months of bank statements and add up every fee: monthly maintenance, transaction charges, cash deposit fees, wire transfer fees, ACH fees and any penalty charges for falling below a minimum balance. That total is your true banking cost.

Now, compare that number against what two or three alternative banks would charge for the same transaction volume and account activity. If the gap is significant, the math makes the case on its own.

Don’t overlook indirect costs, either. If your bank charges for incoming wire transfers, imposes fees on cash deposits above a certain threshold or requires a high minimum balance to waive maintenance charges, those constraints may be influencing how you operate your business in ways that aren’t immediately visible on a statement. Money tied up in a minimum balance requirement is money that isn’t working for you elsewhere.

You’ve outgrown the feature set

Your banking needs at $50,000 in annual revenue are different from your needs at $500,000. If you’re finding that your bank doesn’t integrate with your accounting software, can’t support multi-user access with role-based permissions, lacks international payment capabilities or doesn’t offer the lending products you need as you scale, those are constraints on your growth.

This is worth a deeper evaluation, but as a quick litmus test: if you’ve built workarounds like third-party tools, manual processes or spreadsheets to compensate for things your bank should be handling natively, that’s a sign.

Service quality has declined

Banks change. They merge, they restructure, they close branches and they reassign relationship managers. If you’ve noticed that support response times have increased, that reaching a knowledgeable person requires multiple transfers or that your dedicated banker has been replaced multiple times in the past year, those are indicators of a shifting institutional priority.

The key distinction is between a one-off bad experience and a pattern. Every bank has an off day. But if you’re consistently spending more time managing your banking relationship than your bank is spending managing you, the service no longer justifies the relationship.

Better options now exist

The business banking landscape has changed significantly in the past several years. Online banks and fintechs have expanded their business account offerings with lower fees, higher savings yields and stronger digital tools. Credit unions have broadened their small business services. Even among traditional banks, competitive pressure has led to better integrations, more transparent pricing, and improved mobile banking capabilities.

If you haven’t evaluated your banking options in two or three years, you may be paying more and getting less than what’s currently available. A periodic reassessment, even if it doesn’t result in a switch, ensures you’re making an informed choice rather than a default one. This is especially true if you originally chose your bank based on branch proximity or personal banking convenience rather than a deliberate evaluation of business-specific features and pricing. The bank that was your best option three years ago may no longer hold that position, and a quick comparison of fees, APYs and feature sets can clarify whether you’re still in the right place.

How to switch without disrupting operations

The actual process of switching banks is more methodical than it is difficult. The key is preparation so you know exactly what’s connected to your current account before you start moving things.

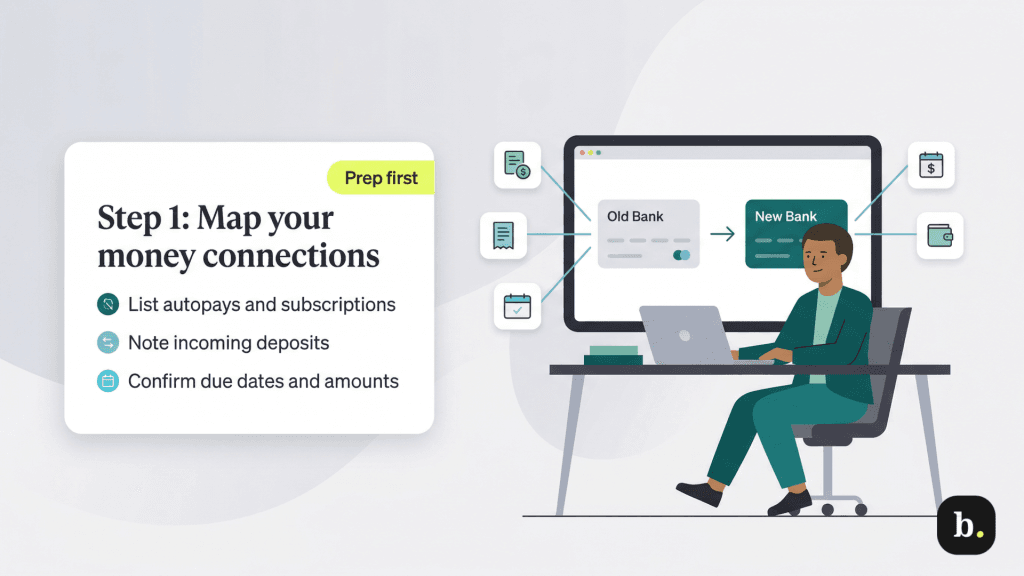

Pre-switch checklist

Before you open a new account, create a complete inventory of everything that touches your current bank account. This includes:

- Automatic payments and recurring charges: Rent, subscriptions, insurance premiums, loan payments.

- Incoming deposits: Client payments, payment processor deposits, marketplace payouts.

- Payroll provider and any direct deposit connections: Merchant services and point-of-sale systems, linked accounts like savings or money market accounts, any tax payment setups such as EFTPS for federal tax deposits and your accounting software’s bank feed connection.

This inventory is the foundation of your transition plan. Missing even one linked payment can result in a failed transaction, a late fee, or a disrupted vendor relationship, so be thorough.

The parallel-run approach

The safest way to switch banks is to run both accounts simultaneously for 60 to 90 days. Here’s how the process works in practice.

- Open your new account first. Get the new account fully set up and funded before you begin redirecting anything. Confirm that all features you need – online banking, ACH transfers, mobile deposit, accounting software integration – are active and working.

- Redirect incoming payments. Start by updating your payment information with clients, invoicing platforms and payment processors so that new revenue flows into the new account. This is typically the most time-sensitive step, since you want income arriving at the right destination as quickly as possible.

- Update outgoing payments systematically. Work through your pre-switch checklist and update each auto-payment, subscription and vendor payment one at a time. Don’t rush this; changing everything simultaneously increases the risk of errors. Prioritize high-consequence payments first: rent, payroll, loan payments, and insurance premiums. Then move through lower-stakes items like software subscriptions and utility bills.

- Keep a buffer in the old account. Leave enough money in your old account to cover any payments that haven’t been redirected yet, plus a cushion for anything you may have missed. Straggling charges, like a quarterly subscription you forgot about or a vendor that processes payments on a delay, are common in the first 60 days. Having funds available in the old account prevents failed payments while you catch and redirect these items.

- Don’t close the old account prematurely. The parallel-run period exists specifically to catch things you missed. Resist the urge to close the old account after the first couple of weeks, even if everything appears to have migrated successfully. Sixty days is the minimum recommended period, while 90 days provides an additional margin of safety.

After the switch

Once you’ve confirmed that all incoming and outgoing payments are flowing through the new account, there are a few final steps to complete the transition.

- Monitor for missed payments. Review your old account statements weekly during the parallel-run period. Any charges that still appear on the old account need to be redirected to the new one. Pay particular attention to quarterly and annual payments that may not cycle during the first month or two.

- Update your accounting software. Disconnect the bank feed for your old account and connect the new one. Ensure that your chart of accounts reflects the new bank and that historical data is preserved. If you use categories, rules or automation in your accounting software, verify that they’re working correctly with the new account’s transaction format.

- Notify key vendors and clients. While most payment redirections happen through your invoicing and payment platforms, some vendors and clients may have your old account’s routing and account numbers on file for direct ACH payments. Send a brief notification with your updated banking information.

- Close the old account. Once you’ve gone a full 60 to 90 days with no activity on the old account and you’ve confirmed that every linked payment has been migrated, contact your old bank to formally close the account. Request written confirmation of the closure for your records.

Switching business banks is a weekend of planning, an hour of paperwork and a couple of months of monitoring; that’s not the operational earthquake most business owners imagine. If your current bank is costing you unnecessary fees, limiting your growth with outdated features or delivering declining service, the discomfort of switching is almost certainly less than the cost of staying. Do the math, make the inventory, run the accounts in parallel and move on to a bank that earns your business.