Even the most profitable companies struggle if customers don’t pay them fast enough. Poor cash flow management remains the leading cause of business failure, with 82 percent of failed businesses citing cash flow problems as a key factor in their closure, according to SCORE. Use this calculator to check the health of your company cash flow and decide whether you need to take action.

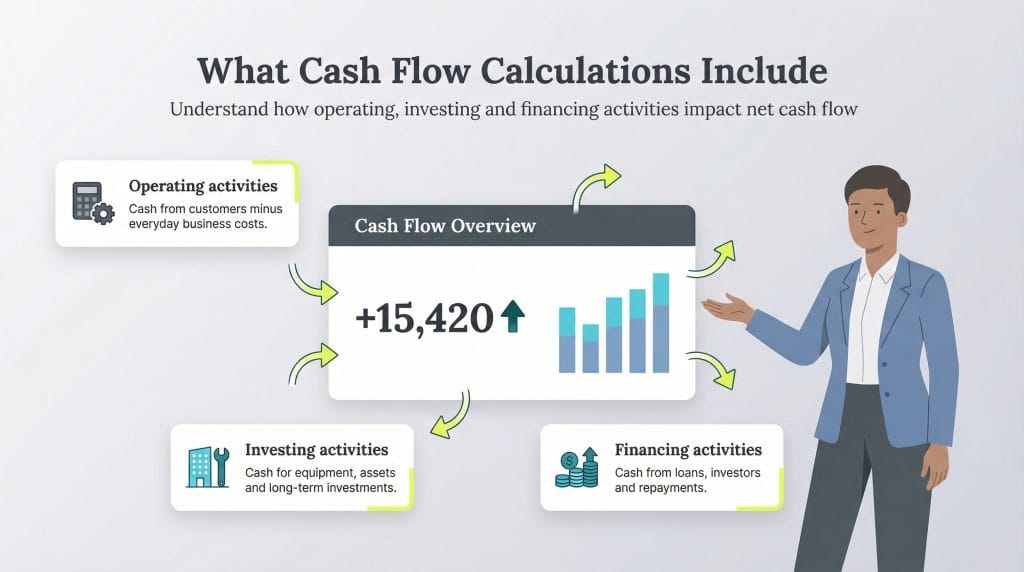

Key terms when using the cash flow calculator

Capital contributions

This is the total cash transferred from shareholders or investors into your business. These payments are classified as capital contributions. Capital contributions are often used to raise money for an expansion or working capital during a downturn. For accounting purposes, contributed capital is added to the shareholder equity section of your company balance sheet.

Capital expenditures

Capital expenditures (CapEx) are longer-term investments made by a business to improve its future cash flows, performance, capacity or profitability.

Examples of CapEx items include acquiring commercial premises to run your business from or investing in new machinery and equipment to increase the volume of products you can manufacture. CapEx items are not regular operational expenses.

Cash at beginning of period

This is how much cash you have in your business at the start of the period you’re measuring.

Cash at end of period

This is the amount of cash you have in your business at the end of your monitoring period. You have positive cash flow if your available cash is higher than it was at the beginning of the period. If you have less available cash, you have negative cash flow.

Dividends paid

Cash dividends are payments made to shareholders from company profits. While dividend taxation varies by individual circumstances, qualified dividends are typically taxed at capital gains rates of between 0 and 20%, depending on your tax bracket. This may be lower than ordinary income tax rates. However, always consult with a tax professional before making dividend distribution decisions.

For insurance

This represents the total premiums paid for all business insurance policies during the measurement period, including general liability, property, workers’ compensation and professional liability coverage.

For inventory

This is the total cash you’ve spent on buying inventory during the time period you are analyzing.

For payroll

Add up all the cash paid out by your company to cover payroll and employment taxes. For many companies, wages are one of the most significant factors affecting cash flow.

Interest paid

Calculate your total interest expenses for the time period you’re analyzing on items like business loans, leases and commercial mortgages.

Loan repayments

Work out how much all loan repayments have cost you for the period you’re analyzing. However, don’t include interest payments; they’re covered by the “Interest paid” variable on the calculator.

Loan repayments encompass principal payments on term loans, equipment financing, lines of credit, credit card balances and lease obligations.

New borrowing

Record how much cash has come into the business through new loans or credit lines. Remember to take into account any repayments made on those facilities in the time period you’re analyzing. You should also include any extensions to existing loans or credit lines.

Other activity

This encompasses cash received from non-operating investment activities, including dividend income from stock holdings, rental income from investment properties, interest earned on bonds and savings accounts, and royalty payments from intellectual property licensing.

Other cash receipts

Calculate all cash received from secondary revenue streams and investment returns that fall outside your primary business operations, such as asset sales proceeds, tax refunds or insurance claim settlements.

Other distributions

Other distributions include money spent on activities such as retiring debt and stock buybacks. Debt retirement involves paying off loan balances ahead of schedule, which can reduce long-term interest costs but creates immediate cash outflows. These transactions often involve a lot of money, and they have a significant impact on your cash flow.

Other payments

This is the sum of all the payments your business has made to meet expenses that don’t fit into the other categories, such as the purchase of office furniture and suppliers, payments to couriers and postage charges. You should include those costs, including one-time expenses, that don’t easily fit into any other categories.

Other use

“Other use” captures cash expenses for investment activities not categorized elsewhere, such as purchasing marketable securities or making loans to other entities.

Purchases

This refers to cash spent acquiring external investments including stocks, bonds, mutual funds, business acquisitions or stakes in other companies.

Received from customers

This is the total cash paid to your company by customers in the time period being analyzed. This includes all forms of payment actually received: cash, checks, electronic transfers and credit card deposits. However, this does not include outstanding accounts receivable.

Sale

This represents cash proceeds from divesting investment holdings, including stocks, bonds, mutual fund shares and ownership stakes in other businesses, net of any transaction fees.

Sale of property

These are cash receipts from disposing of company assets including real estate, equipment, vehicles, intellectual property rights and patents.

Stock issuing

This reflects net proceeds from equity financing activities, including the issuing of new shares, the selling of treasury stock, or completing secondary offerings, after deducting underwriting fees and issuance costs.