Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Turn surplus stock into money you can invest in your business.

If you sell products, you may find yourself with excess inventory at some point — items you thought you’d sell, but for some reason haven’t yet been able to. Excess inventory ties up cash in products, prevents you from ordering more items with a better chance of selling, and incurs additional costs for warehousing and storage.

However, you’re not necessarily stuck with your excess inventory. You can turn that surplus stock into cash that you can invest in other parts of your business.

Excess inventory, also known as overstock, consists of products that haven’t sold yet — and you’re not anticipating they’ll sell anytime soon. Often this surplus stock is kept for weeks, months, and even years without being sold or used.

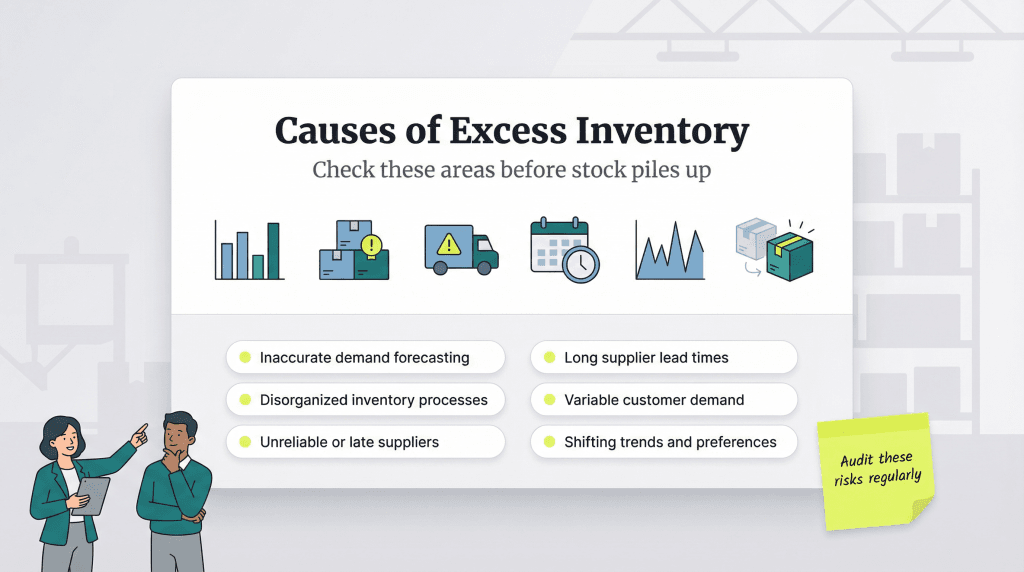

Excess inventory is often a result of poor inventory management, a bad product launch, or unpredictable market demand. It can result in revenue loss and cause other financial burdens.

Here are five ways to cash in on excess inventory. The best method for you depends on the goods — and quantities — you have on hand.

Retailers, wholesalers, manufacturers, distributors and others can sell goods via centralized liquidation auctions. For example, Liquidation.com is a B2B bulk marketplace where companies sell all kinds of excess goods. It welcomes inventory from small businesses to sell on its auction marketplace and has a track record of providing higher returns than other liquidation methods.

Using inventory liquidators is an easy way to get some cash for your excess inventory. Such platforms can be a good way to get the best bang for your buck, and the auction setting can be an excellent format for maximizing your excess inventory’s value.

If you need cash for your excess inventory quickly, you can avoid the bother of auctions by selling to a surplus inventory liquidator like Merchandise USA. These companies buy a wide range of customer-returned and excess inventory.

If you must get rid of your inventory but want more control over the sales channel than you get when using an inventory liquidator, eBay is an excellent option.

Opening a business seller account on eBay can be a great way to sell excess inventory at competitive prices. You can get rid of overstock and expand your revenue sources.

Your incorporated business can earn an above-cost federal income tax deduction, clear out warehouse space, avoid liquidation nightmares, and help schools and nonprofits at the same time, courtesy of Internal Revenue Tax Code Section 170 (e)(3).

The National Association for the Exchange of Industrial Resources (NAEIR) takes donations of new, overstocked or discontinued products such as school and office supplies, toys, games, building materials, clothing, tools and much more. It redistributes these items to schools and nonprofits nationwide; donor companies can receive an enhanced income tax deduction of up to twice the cost of the goods. NAEIR also provides the paperwork to help when filing taxes.

You can deduct the cost of goods sold, as carried on your books, plus half the difference between cost (basis) and the fair market value; the tax deduction cannot exceed twice the cost. For example, items carried on the books at a cost of $100 that have an established fair market value of $200 may be donated, and a deduction of $150 may be taken.

If, however, those items carried at a $100 cost have an established fair market value of $300, they may be donated, and a deduction of $200 may be taken.

Excite loyal customers by giving away discounted items from your excess inventory stash. This helps you recoup money while placing your products in customers’ hands.

“Use the excess inventory items to give out as a reward to loyal customers or those who have accumulated a certain amount of points,” suggested marketing specialist Igor Mitic. “Another way is to create promotions where customers are rewarded for sharing posts on Facebook or Instagram, or participating in online polls or surveys, and convert the excess inventory into marketing.”

Here are a few other giveaway ideas:

There are many reasons why a business might end up with excess inventory. Here are a few typical ones:

Excess inventory can be a serious financial drag for any business because it causes the following problems:

Sometimes keeping your excess inventory is advisable — if you have the space to store it and your products have a longer life cycle. “Having excess inventory definitely helps by removing the risk of revenue loss due to out-of-stock issues,” said Jeremy Ong, vice president of business operations at Delphi Digital. “This is, of course, only applicable if you have products that are nonperishable and have enough operating cash flow to support excess inventory.”

Obviously, holding onto perishable inventory doesn’t make sense. Local grocery stores shouldn’t run giveaways to offload rotten fruit, and you shouldn’t donate expired products.

Excess inventory concerns depend on your business type and industry. However, if overstock negatively affects your cash flow and operations, there are ways you can move forward and keep your business healthy.

Jennifer Dublino contributed to this article. Source interviews were conducted for a previous version of this article.