Business credit card rewards can provide real value for growing companies. Whether you’re earning cash back on everyday purchases, accumulating travel rewards or taking advantage of category bonuses, those perks can help offset routine business expenses over time.

The challenge is making sure each card has a purpose. Without a clear strategy, rewards can become fragmented across multiple programs, annual fees can add up and employees may use the wrong card for key purchases. The businesses that get the most value from multiple business credit cards typically assign each card a specific role and match spending to the rewards structure that delivers the strongest return.

This guide explains how to evaluate reward programs, analyze your spending, build a card lineup, manage employee cards and avoid common mistakes that can reduce the value of your rewards.

How business credit card rewards programs work

Before deciding which cards belong in your wallet, it’s important to take a look at how different rewards programs work. Some cards reward the same rate on every purchase, while others offer bonus rewards in specific categories. Understanding those differences can help you earn more from the spending your business is already doing.

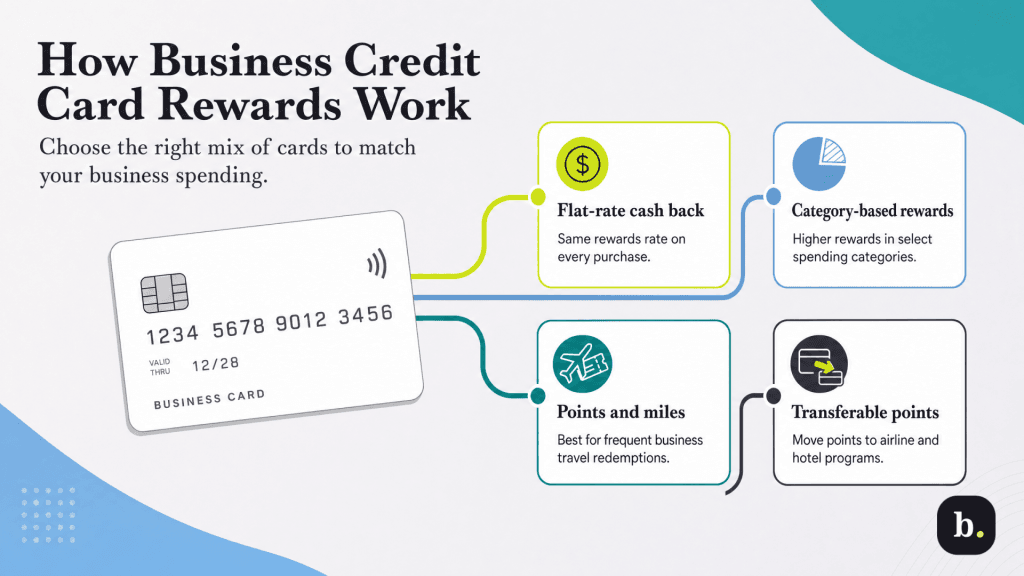

Most business credit cards fall into one of four rewards models:

- Flat-rate cash back: These cards earn the same rewards rate on every purchase, regardless of category. They’re simple to manage and often serve as a catch-all card for expenses that don’t qualify for a bonus category.

- Category-based rewards: These cards offer elevated rewards in specific spending categories, such as travel, online advertising, shipping, office supplies, telecommunications services or dining. Businesses with concentrated spending in those areas can often earn significantly more than they would with a flat-rate card.

- Points and miles programs: These cards earn rewards as points or miles instead of cash back. For businesses that travel regularly, those rewards can sometimes go further than a standard cash-back program. The trade-off is that you’ll usually spend more time managing redemptions and transfer options.

- Transferable points programs: Some issuers let you transfer points to airline and hotel loyalty programs rather than redeeming them directly. It takes a little more effort, but businesses that travel regularly can sometimes get more value from their rewards that way.

There’s no requirement to pick one rewards structure and stick with it. Many businesses use a mix of cards, with one card handling travel expenses, another earning bonus rewards in key categories and a flat-rate card filling the gaps.

How to optimize your business credit card rewards

Once you understand how different rewards programs work, the next step is putting that knowledge into practice. Businesses that get the most value from multiple credit cards don’t randomly collect cards with attractive rewards. Instead, they create a system that routes spending to the card that rewards it best.

The process is fairly straightforward: identify where your business spends money, assign each card a specific role and make sure employee spending follows the same strategy.

Step 1: Audit your business spending.

Optimization starts with knowing where your money actually goes. Reviewing transactions from your business bank account can make it easier to identify spending patterns. Start by pulling up the last three to six months of expenses and looking for patterns. Which categories account for the biggest share of your spending? Those are usually the areas worth focusing on first. After all, a bonus rewards rate on a category where you spend thousands of dollars each month is likely to generate far more value than an elevated rate on a category that only comes up occasionally.

Once you’ve identified your biggest expense categories, compare them against your existing cards’ rewards structures. This exercise often reveals where you’re leaving rewards on the table.

If you’re considering adding another card, here’s a useful rule of thumb: A new card should earn its place by covering a meaningful spending category that your current cards don’t reward well, especially if you’re also working to improve your business credit score. The additional rewards should clearly outweigh any annual fee and the extra management required.

Before adding another card, look at where your business spends the most money. Optimizing one or two major spending categories often delivers more value than juggling several specialized cards. That's one of the easiest ways to

get the most out of your business credit cards.

Step 2: Build your card lineup.

Once you’ve identified your biggest spending categories, it’s time to decide which card should handle each type of expense. Most businesses don’t maximize rewards by putting every purchase on a single card. Instead, they use different cards for different spending categories, with each card earning the strongest rewards where it’s used most.

A well-rounded lineup often includes:

- An anchor card: Usually a flat-rate cash-back card that handles purchases outside your bonus categories. Think of it as your default card — the one you reach for when a purchase doesn’t fit neatly into one of your higher-reward categories.

- Category cards: One or more cards that earn elevated rewards in your largest spending categories, such as travel, online advertising, shipping, telecommunications services or office supplies.

The right mix depends on how your business operates. For example:

- Travel-heavy businesses: Not every business spends heavily on travel, but those that do often make a travel-focused card the workhorse of their lineup. A flat-rate card can fill in the gaps for everyday purchases.

- Marketing-focused businesses: A digital marketing agency or any business with significant advertising expenses may benefit from a card that rewards online ad spending, paired with a flat-rate card for everything else.

- Businesses with varied operating expenses: Some businesses don’t have a single dominant spending category. In those cases, a flat-rate card paired with one or two category cards matched to your largest recurring expenses often works well.

It’s easy to assume more cards automatically mean more rewards, but that’s not always the case. Every card adds another account to manage, another rewards program to track and potentially another annual fee. If a card isn’t earning its keep, it may be more hassle than it’s worth.

Some businesses prefer to keep most of their spending on cards from the same issuer because rewards are easier to pool and redeem. Others don’t mind juggling multiple programs if it means earning better rewards in more categories. Which approach makes sense depends largely on how much time you’re willing to spend managing it all.

Step 3: Include employee spending in your strategy.

Employee cards can dramatically increase the amount of rewards your business earns. Many business credit card programs allow rewards from employee purchases to flow into a central account rather than being split among individual users. That means everyday spending across your team can help build a larger rewards balance.

However, the more employee cards you issue, the easier it becomes for spending to end up on the wrong card. If certain cards are reserved for travel, advertising or other categories, make that clear upfront. Spending limits and category controls can help keep everything organized and support better expense management.

Get more value from the rewards you earn

Building the right card lineup helps you earn more rewards. The next step is making sure you redeem those rewards in a way that delivers the greatest value for your business.

Consider the following decisions before cashing out points, miles or cash-back rewards.

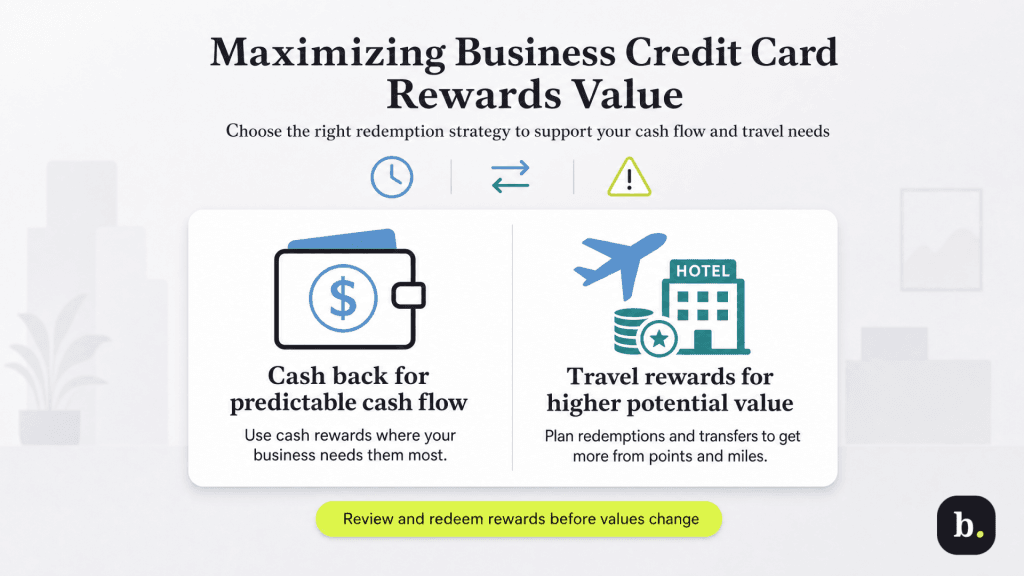

Should you redeem rewards for cash back or travel?

Cash back is simple, flexible and predictable, making it a useful tool for businesses focused on cash flow. Every dollar earned has a clear value, and rewards can typically be applied wherever they’re needed most.

Points and miles can be especially appealing for businesses that travel often. In some cases, a flight or hotel redemption may deliver more value than taking the equivalent amount in cash back. The catch is that getting that extra value usually takes a little more planning. Businesses that prefer a simpler approach may be perfectly happy sticking with cash back.

Are transfer partners worth the effort?

Some rewards programs allow points to be transferred to airline and hotel loyalty programs rather than redeemed directly through the card issuer.

For businesses that travel often, those transfers can sometimes provide more value than redeeming rewards for cash back or statement credits. However, the best opportunities aren’t always available when you need them, so maximizing value may require some patience and planning.

When should you redeem your rewards?

One of the biggest mistakes businesses make is focusing entirely on earning rewards while paying little attention to when they’re used.

Points and miles don’t always hold the same value forever. Loyalty programs can change redemption rates, and some rewards may expire or be forfeited when an account closes. Rather than letting rewards accumulate indefinitely, review your balances periodically and redeem them when they support a business need.

Before closing any credit card account, check whether outstanding rewards need to be redeemed, transferred or converted first. In some programs, unused rewards disappear when the account is closed.

Industry estimates suggest roughly

$6 billion in credit card rewards could go unredeemed in 2026. Earning rewards is only half the equation; redeeming them regularly is what turns points, miles and cash back into real value.

Common rewards optimization mistakes

Rewards can add up over time, but it’s surprisingly easy to leave value on the table. Here are a few mistakes businesses make when trying to get the most from their credit card rewards:

- Opening cards just because of welcome bonuses: A nice welcome offer can be tempting, but a card’s long-term value matters more than any one-time incentive. A welcome bonus may help break a tie between two strong options, but don’t let it drive the decision on its own.

- Letting rewards sit unused: Points, miles and cash-back rewards don’t always become more valuable with time. Some programs adjust redemption rates, and certain rewards can expire or be forfeited. Make reviewing and redeeming rewards part of your regular financial routine.

- Making your card lineup too complicated: Every additional card adds another account to monitor, another rewards program to track and another annual fee to justify. If the extra rewards aren’t worth the added complexity, a simpler setup may be the better choice.

- Carrying a balance to earn rewards: It’s easy to focus on points, miles and cash back, but interest charges can quickly wipe out those gains. If you’re paying interest month after month, the rewards are unlikely to make up the difference. That’s why rewards strategies tend to work best when balances are paid in full.

The best rewards strategy is the one you’ll actually use

The most effective rewards strategy isn’t necessarily the one with the most cards. It’s the one that matches the way your business actually spends money. By identifying your biggest expense categories, assigning each card a clear role and redeeming rewards thoughtfully, you can earn more value from purchases you’re already making.

Review your card lineup periodically as your business evolves and continue building business credit through responsible card use. Spending patterns fluctuate, rewards programs change and new card options become available. Above all, remember that rewards only create value when balances are paid in full. A focused lineup built around your real expenses will usually outperform a complicated collection of cards chosen primarily for welcome bonuses.