Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Maximize your savings with federal tax credits designed specifically for small business owners.

Tax season doesn’t have to drain your business bank account. While most business owners know about tax deductions, many overlook the more powerful option: tax credits. We’re talking about direct, dollar-for-dollar reductions to your tax bill that can save you thousands of dollars each year.

In this comprehensive guide, we’ll walk you through every major small business tax credit available in 2025, explain exactly how to claim them and show you the forms you need. We’ll also clarify the crucial difference between credits and deductions — a distinction that could save you significant money.

Tax credits reduce your tax bill dollar-for-dollar, while deductions only reduce your taxable income. If you owe $10,000 in taxes and have a $2,000 credit, you now owe $8,000. A $2,000 deduction might only save you $500, depending on your tax bracket.

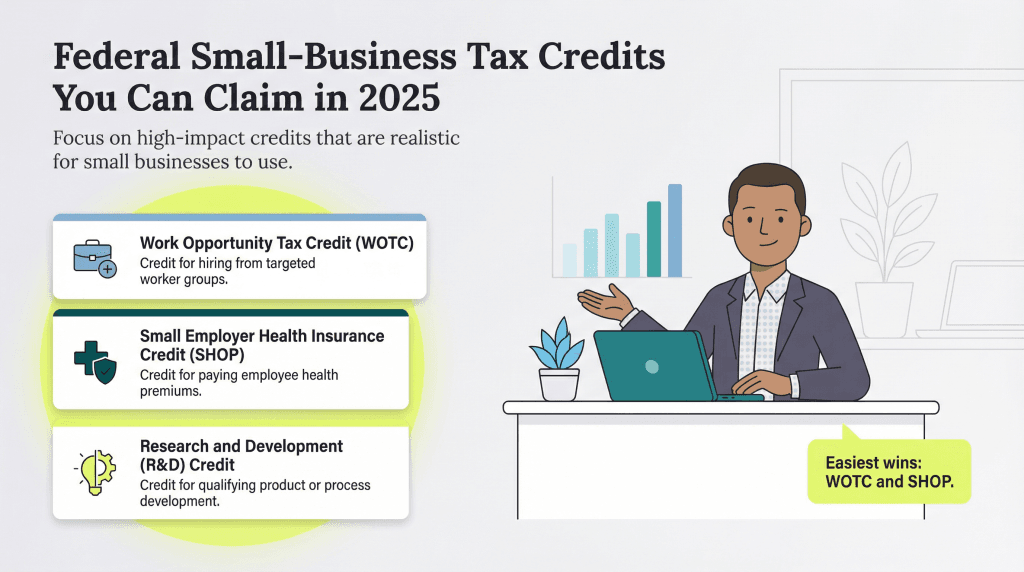

These are the top tax credits for small businesses that you can claim on your 2025 tax return. We’ve organized them by potential impact and ease of claiming:

When business owners search for a “small business startup tax credit,” they’re usually referring to the retirement plan startup credits expanded under SECURE 2.0, which took effect in 2023. Here’s what’s actually available:

These credits make it manageable for small businesses to start and maintain retirement plans for their first few years, addressing one of the biggest barriers to offering employee benefits.

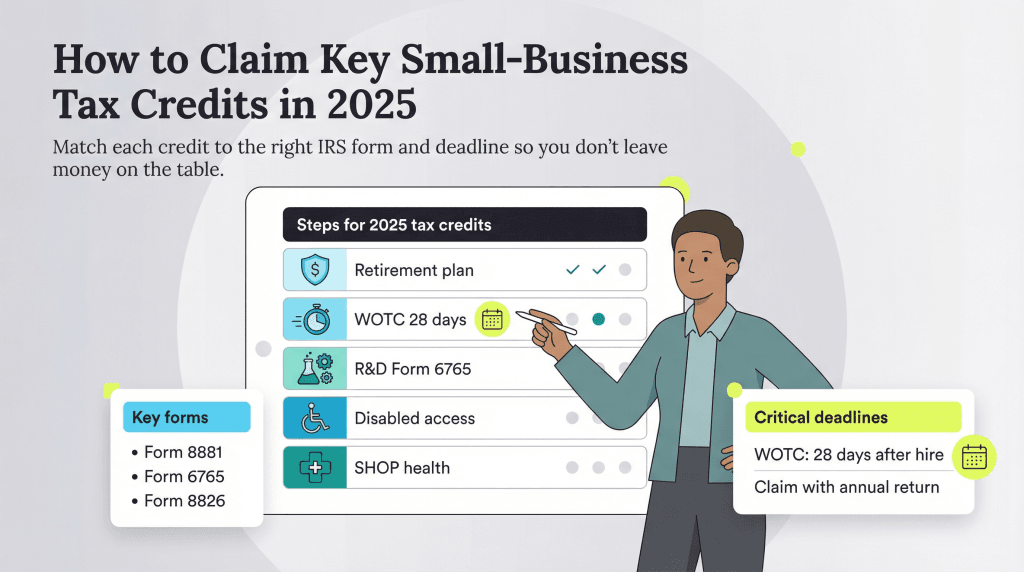

We’ve broken down the exact process for claiming each major small business tax credit. Follow these steps carefully to ensure you receive every dollar you’re entitled to:

Understanding this distinction is crucial for maximizing your tax savings.

Tax Credits | Tax Deductions |

|---|---|

Reduce your tax bill dollar-for-dollar | Reduce your taxable income |

$1,000 credit = $1,000 saved | $1,000 deduction = $220-$370 saved (depending on tax bracket) |

More valuable but harder to qualify for | More common and easier to claim |

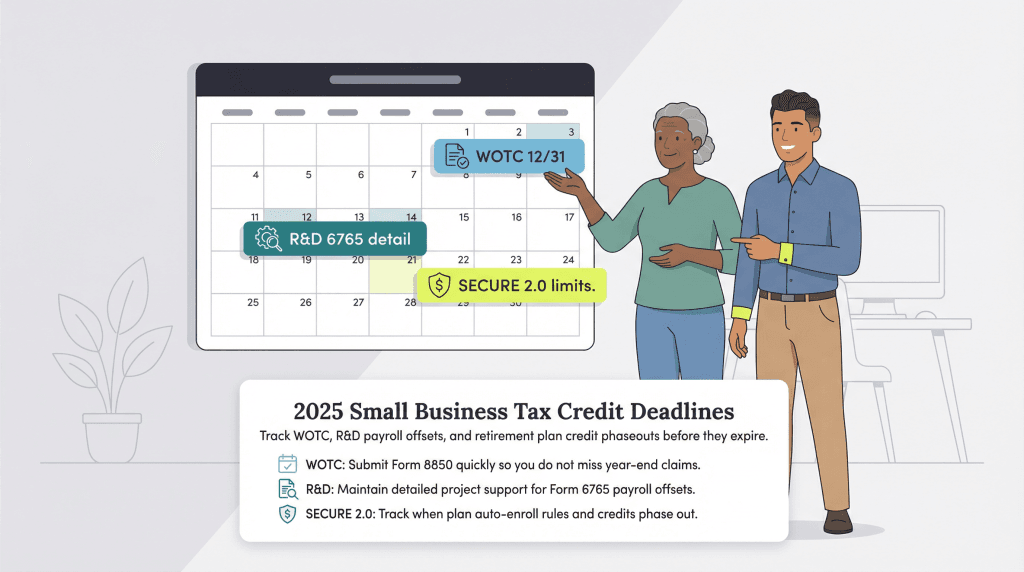

Several important changes and deadlines affect small business tax credits in 2025:

The Work Opportunity Tax Credit is currently authorized through December 31, 2025. Congress typically extends this credit, but businesses should maximize claims this year in case of changes. We recommend submitting all eligible Form 8850s as soon as possible rather than waiting.

Qualified small businesses (QSBs) with less than $5 million in gross receipts can offset up to $500,000 in payroll taxes using the R&D credit. Starting in 2025, businesses must provide additional detail on Form 6765, including specific project descriptions and expense categorizations. The IRS has increased scrutiny on R&D claims, making proper documentation essential.

While the retirement plan startup credits are fully available, some promised features are still being implemented. Automatic enrollment requirements for new plans don’t begin until 2025, but claiming the additional $500 credit for voluntary automatic enrollment remains advantageous. The employer contribution credit phases out completely for businesses with more than 100 employees.

Small business tax credits represent one of the most underutilized opportunities for reducing your company’s tax burden. Unlike deductions that merely reduce taxable income, these credits provide dollar-for-dollar tax savings that can significantly impact your bottom line.

Here’s your action plan for maximizing tax credits for small business in 2025:

We recommend working with a qualified tax professional who specializes in small business taxes to ensure you’re claiming every available credit correctly. The investment in professional tax preparation often pays for itself through additional credits identified and properly documented.

Remember that tax laws change frequently, and new credits become available as Congress passes legislation supporting small businesses. Stay informed about tax law changes and review your eligibility for credits annually. We also recommend keeping detailed records throughout the year rather than scrambling during tax season — this preparation makes claiming credits much easier and ensures you don’t miss any opportunities.

Take action today by reviewing our list of credits, identifying which ones apply to your business, and setting up systems to track qualifying expenses and activities throughout 2025. Your future self will thank you when tax season arrives and you’re able to claim every dollar of credits you’ve earned.