Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

For many small business owners, insurance pricing feels like a black box. You submit an application, wait for a quote, and receive a premium that may or may not seem reasonable — with little visibility into how the number was calculated or what factors influenced the decision. But understanding the process behind that number gives you practical leverage to influence both the price you pay and the terms you receive.

That process is called insurance underwriting. It’s how an insurance company evaluates the risk of insuring your business, decides whether to offer coverage, and determines your premium, deductible, coverage limits, and any special conditions or exclusions. Underwriting happens every time you apply for a new policy, add coverage or renew an existing policy — it’s not a one-time event.

This guide explains the insurance underwriting process step by step, breaks down the factors underwriters evaluate, shows how underwriting differs across coverage types and provides practical guidance to position your business for better underwriting outcomes.

What insurance underwriting is and why it exists

Insurance is fundamentally a risk transfer. You pay a premium to transfer the financial risk of certain losses — property damage, liability claims, employee injuries, data breaches, etc. — from your business to the insurer. The insurer collects premiums from many policyholders and uses those funds to pay claims as they arise. For this model to work, the insurer needs to assess the likelihood and severity of each policyholder’s potential losses, so it can price premiums appropriately and avoid taking on more risk than it can sustain.

Underwriting is the process by which the insurer makes that assessment. Underwriters analyze information about your business — your industry, your operations, your claims history, your financial stability and your risk management practices — and use it to answer several core questions. How likely is this business to file a claim? If a claim occurs, how severe could it be? Does this risk fit within the types and concentrations of risk the insurer wants in its portfolio?

The output of underwriting is your policy terms: what’s covered, what’s excluded, your coverage limits, your deductible and your premium. Businesses that present lower risk to the insurer receive more favorable terms. Businesses that present a higher risk pay more, face more restrictive conditions, or, in some cases, are declined altogether.

Did You Know?

Types of business insurance risks include liability risks, environmental risks, cybersecurity risks and even leadership risks.

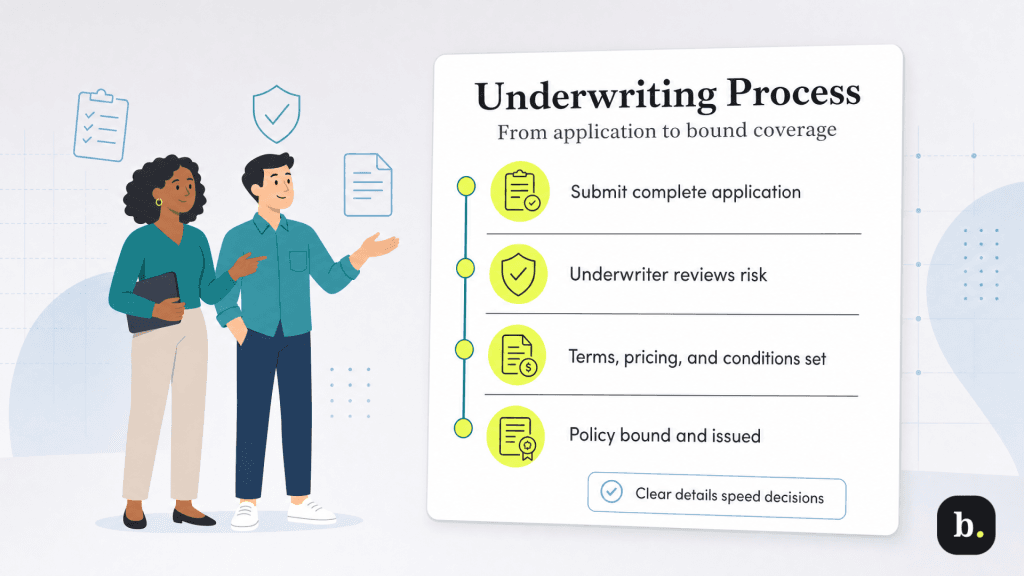

The underwriting process step by step

The business insurance underwriting process can be broken down into four parts.

1. Application and information gathering

The insurance underwriting process begins when you submit an insurance application, either directly with an insurer or through an agent or broker who submits it on your behalf. The application collects foundational information about your business: your legal structure, industry, years in operation, annual revenue, number of employees, physical locations, property values and the specific coverages you’re requesting.

Depending on the coverage type and the complexity of your business, the insurer may request additional information beyond the application. Common supplemental requests include loss runs (claims history reports from your current or previous insurers covering the past three to five years), financial statements, documentation of safety programs and risk management practices, copies of contracts that impose insurance requirements, inspection reports, and details about specific operations or processes that affect risk.

The quality and completeness of your application matter more than many business owners realize. An incomplete or vague application slows the process and forces the underwriter to make assumptions about your risk — assumptions that rarely work in your favor. A thorough, well-organized application with supporting documentation signals that your business is professionally managed and helps the underwriter see the full picture rather than filling gaps with worst-case estimates.

2. Risk assessment

Once the underwriter has gathered the necessary information, they evaluate it against the insurer’s risk appetite and pricing models. This is the analytical core of underwriting — the stage where the underwriter determines how risky your business is relative to others in your industry and decides what terms are appropriate.

Underwriters use a combination of quantitative analysis and qualitative judgment. On the quantitative side, they draw on industry loss data, actuarial models and claims statistics to establish baseline expectations for your type of business. On the qualitative side, they evaluate factors such as the quality of your management, the strength of your safety practices, the stability of your operations, and any unique aspects of your business that make it more or less risky than the industry average.

For some policies, particularly those involving physical property or higher-risk operations, the insurer may send an inspector to evaluate your premises, equipment or operations before making a final underwriting decision. The inspector’s report becomes part of the underwriting file and can influence the terms offered.

3. Decision and terms

Based on the assessment, the underwriter arrives at one of three decisions. The first is to accept the risk as applied for, offering coverage at the standard terms and premium for your risk profile. The second is to accept the risk with modifications — a higher premium than standard, a higher deductible, specific exclusions that limit coverage for certain activities or exposures, or lower limits than requested. The third is to decline the risk entirely, meaning the insurer has determined your business doesn’t fit within its risk appetite.

In cases where the risk is accepted with modifications, the underwriter may also apply subjectivities — conditions that must be met within a specified time frame after the policy is issued. For example, the insurer might require you to install a fire suppression system within 90 days, update your electrical wiring by a certain date or implement a specific safety protocol. Failure to meet subjectivities within the required timeframe can result in policy cancellation or non-renewal.

4. Binding and policy issuance

Once you’ve agreed to the offered terms, the policy is bound — meaning coverage is officially in effect from the agreed-upon start date. Binding can happen quickly; your agent may be able to bind coverage immediately for standard risks. Or, it may require additional time for complex risks that need senior underwriter approval.

After binding, the insurer issues the formal policy document, which details all terms, conditions, exclusions and insurance endorsements. Review this document carefully to confirm the coverage matches what was discussed and agreed upon during the quoting process. If anything looks different from what you expected, raise it with your agent immediately.

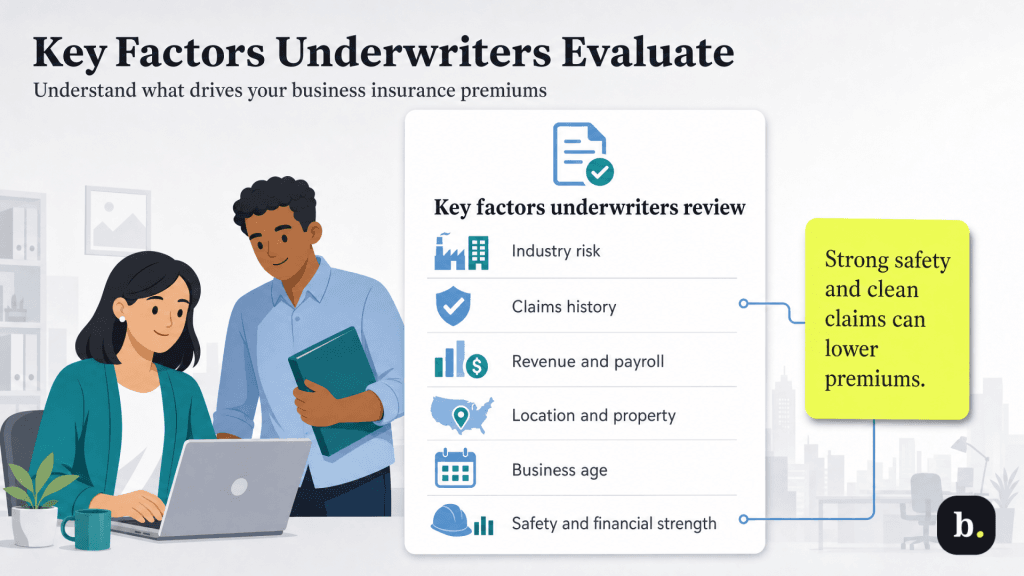

Key factors underwriters evaluate

While every underwriting decision involves some subjective judgment, certain factors consistently carry the most weight across all coverage types. Understanding what underwriters are looking at helps you anticipate their concerns and position your business accordingly. Below are the insurance rating factors evaluated during underwriting.

Industry and business type

Your industry classification is the single biggest factor in determining your base premium. Insurers use classification codes — often based on North American Industry Classification System (NAICS) codes or their own proprietary systems — to categorize your business and assign a baseline risk profile. A roofing contractor and an accounting firm operate in fundamentally different risk environments, and their premiums reflect that difference from the start.

Within industries, the specific nature of your operations matters. Two businesses classified as general contractors may present very different risk profiles depending on whether one does residential renovations and the other does commercial high-rise construction. The more precisely the underwriter understands what your business actually does, the more accurately they can assess your risk, which is why detailed application answers matter.

Claims history

Your past claims experience is one of the most influential factors in your premium and one of the factors most directly within your control over time. Underwriters review your loss runs — detailed reports of every claim filed against your business over the past three to five years, including claim dates, descriptions, amounts paid and amounts held in reserve for open claims.

A pattern of frequent claims, even if individual claim amounts are small, signals to the underwriter that your business has ongoing risk management issues. Large or severe claims raise concerns about the potential for catastrophic losses. Open claims (unresolved at the time of underwriting) are viewed as active liabilities that the insurer may need to account for in its pricing.

Conversely, a clean claims history is one of the strongest factors working in your favor. It demonstrates that your business manages risk effectively, which makes you a more attractive policyholder. Many insurers offer claims-free discounts that directly reduce your premium.

Revenue and business size

Revenue serves as a proxy for exposure in many liability policies. The reasoning is straightforward: higher revenue generally correlates with more customer interactions, more transactions, and more opportunities for something to go wrong and result in a claim. General liability premiums in particular are heavily influenced by revenue.

Employee count and total payroll are the primary rating factors for workers’ compensation. More employees and higher payroll mean more people performing work that could result in injury, and greater potential costs if an injury occurs. Square footage and declared property values drive commercial property premiums. In each case, size is a proxy for exposure.

Location

Where your business operates affects your premium in several important ways. Geography determines your exposure to natural disasters — businesses in hurricane-prone coastal areas, earthquake zones or flood plains face higher property insurance premiums. Local crime rates affect property and theft-related premiums. The litigation environment in your jurisdiction influences liability premiums — some regions have significantly higher average claim settlements than others.

State regulatory requirements also play a role. Workers’ compensation rules, minimum coverage mandates, and insurance market regulations vary by state and affect both availability and pricing. Businesses operating in multiple states may see different premium structures for each location based on local conditions and regulatory frameworks.

Years in operation

Newer businesses are generally considered higher risk because they lack an established track record. A business that has operated successfully for several years with a clean claims history has demonstrated its ability to manage risk. A startup, regardless of how well-managed it may be, is an unknown quantity from the underwriter’s perspective.

This doesn’t mean startups can’t get insurance, but they may face higher premiums, more restrictive terms or limited coverage options until they build an operating history. As a general rule, the first three to five years of operation are when underwriters apply the most scrutiny. After that, assuming the claims history is clean and operations are stable, the business’s track record begins to work in its favor.

Safety and risk management practices

Underwriters don’t just evaluate how much exposure your business has; they also evaluate what you’re doing to manage that exposure. Documented safety programs, employee training records, equipment maintenance schedules, workplace safety records, OSHA compliance history, and security measures like alarms, cameras and fire suppression systems all signal proactive risk management.

For workers’ compensation in particular, your safety practices and experience modification rate (EMR) have a direct, measurable impact on your premium. The EMR is a multiplier — typically calculated by a rating bureau based on your historical claims — that adjusts your base premium relative to other businesses in your industry and state. An EMR of 1.0 indicates average claims experience. A modifier below 1.0 means better-than-average performance and reduces your premium, while a modifier above 1.0 reflects worse-than-average experience and increases your premium. A formal safety program that reduces workplace injuries over time directly lowers your EMR and, by extension, your premium.

Some insurers offer premium credits for specific risk management certifications, safety training programs or loss control measures. Ask your agent whether any credits are available for actions your business has already taken or is willing to implement.

Financial stability

For larger policies or higher-risk businesses, underwriters may review your financial statements as part of the assessment. A financially stable business is more likely to maintain its risk management programs, invest in safety, keep its operations in good condition and remain a policyholder for the long term — all of which make it a more attractive risk for the insurer.

Financial distress, on the other hand, can be a red flag. Businesses under financial pressure may defer equipment maintenance, cut safety programs, reduce staffing in ways that increase per-employee workload and injury risk, or take on riskier projects to generate revenue. From the underwriter’s perspective, these behaviors all increase the likelihood of claims.

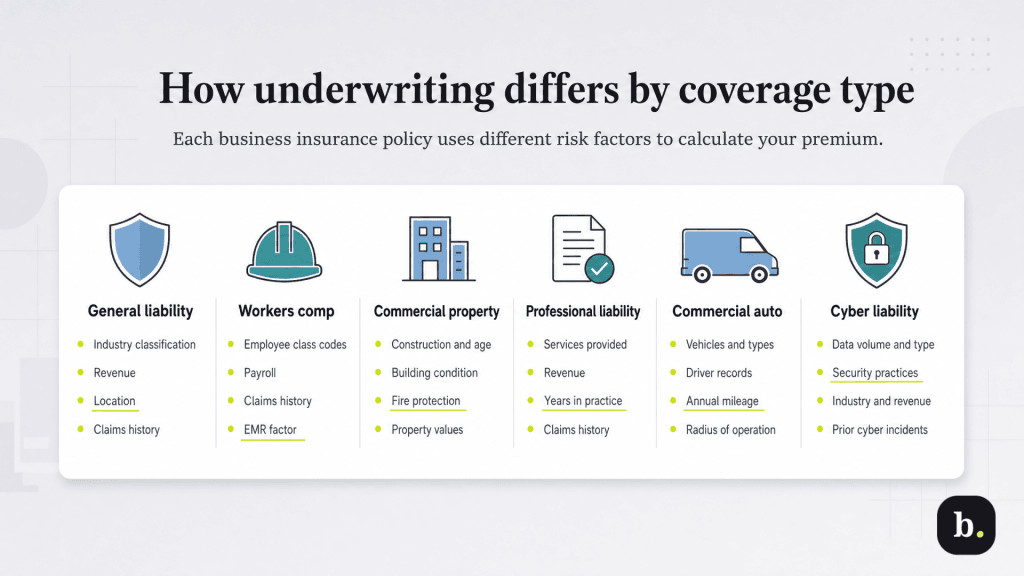

How underwriting differs by coverage type

While the general underwriting process is consistent across coverage types, each type of insurance has its own primary rating factors. Understanding what drives pricing for each coverage helps you focus on the factors that matter most for the insurance your business requires. The chart below outlines the primary rating factors for common business insurance policies.

Coverage Type

Primary Rating Factors

General Liability

Industry classification, revenue, location, claims history

Building construction type, age and condition, fire protection, occupancy, property values

Professional Liability

Type of professional services, revenue, years in practice, claims history, engagement size

Commercial Auto

Number and type of vehicles, driver records, annual mileage, radius of operation, cargo type

Cyber Liability

Data volume and type, security practices, industry, revenue, prior incidents, regulatory compliance

How to improve your underwriting outcome

While you can’t change your industry classification, many of the factors that influence underwriting are within your control. Here’s how to position your business for the most favorable terms available.

Maintain thorough and accurate records. A clean, complete application with supporting documentation receives better underwriting treatment than an incomplete or vague submission. Provide detailed descriptions of your operations, including documentation of your safety programs, and respond promptly and thoroughly to any supplemental information requests from the underwriter. The more clearly the underwriter can see your risk, the less they need to rely on conservative assumptions.

Invest in loss prevention. Documented safety programs, regular employee training, proper equipment maintenance, workplace safety audits and physical security measures all signal to underwriters that your business takes risk management seriously. These investments pay for themselves twice — once through reduced claims and again through lower premiums. For workers’ compensation in particular, a formal safety program that reduces workplace injuries over time will lower your EMR and produce measurable premium savings.

Manage your claims proactively. Report claims promptly, cooperate fully during the claims process and implement corrective actions after a loss to prevent recurrence. When considering whether to file a claim, weigh the claim amount against the potential impact on premiums. Very small claims that you can absorb out of pocket may not be worth filing if the premium increase over subsequent years would exceed the claim payout.

Work with a knowledgeable agent or broker. An experienced commercial insurance broker understands how underwriters evaluate risk and can present your business in the most favorable light. They know which information to emphasize, how to provide context for past claims and how to frame unusual operations so underwriters can assess them accurately. A good broker also knows which carriers have the strongest appetite for your type of risk, which means your application is being evaluated by insurers that are predisposed to write your kind of business.

Shop strategically. Different insurers have different risk appetites, and a business that one carrier declines or prices aggressively may be a preferred risk at another carrier that specializes in your industry. Insurers that focus on specific sectors — construction, healthcare, technology, hospitality — often offer more competitive terms than generalist carriers because they understand the nuances of your risk profile. Your agent or broker can identify which carriers are the best fit for your specific business.

Address known issues proactively. If you know an underwriter will flag something about your business — an older building with aging systems, an unusual operation, a past claim with a large payout — address it in your application rather than waiting for the underwriter to discover it. Provide context, explain what you’ve done to mitigate the risk and include documentation of any improvements. Proactive disclosure with supporting evidence is always more favorably received than having the underwriter uncover the issue independently and draw their own conclusions.

Tip

Ready to start the underwriting process? Get connected with leading insurers through business.com's guide to the best business insurance providers.

Demystifying business insurance underwriting

Insurance underwriting is the process that determines your coverage terms and your premium. While it may feel opaque from the outside, the factors that underwriters evaluate are well-defined and largely within your influence over time. Your industry classification and location are fixed, but your claims history, your safety practices, the quality of your application and the way your business is presented to the insurer are all factors you can actively manage.

The businesses that consistently receive the best underwriting outcomes are those that demonstrate professional management, invest in loss prevention, maintain clean claims records, and work with knowledgeable agents or brokers who understand the underwriting process. None of these things requires significant expense — they require attention, discipline, and the recognition that how you present your business to an insurer has a direct impact on what you pay for coverage.

Understanding underwriting doesn’t just help you get better insurance pricing; it also helps you understand your insurance coverage. That helps you run a better business. The same practices that make you a more attractive risk to an insurer — strong safety programs, careful risk management, thorough documentation and proactive problem-solving — make your business more resilient, more efficient and better positioned for long-term success.

Adam Uzialko, the accomplished senior editor at Business News Daily, brings a wealth of experience that extends beyond traditional writing and editing roles. With a robust background as co-founder and managing editor of a digital marketing venture, his insights are steeped in the practicalities of small business management.

At business.com, Adam contributes to our digital marketing coverage, providing guidance on everything from measuring campaign ROI to conducting a marketing analysis to using retargeting to boost conversions.

Since 2015, Adam has also meticulously evaluated a myriad of small business solutions, including document management services and email and text message marketing software. His approach is hands-on; he not only tests the products firsthand but also engages in user interviews and direct dialogues with the companies behind them. Adam's expertise spans content strategy, editorial direction and adept team management, ensuring that his work resonates with entrepreneurs navigating the dynamic landscape of online commerce.