Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Insurance Is Required for My Type of Business?

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

One of the most common questions new and established business owners ask is which types of insurance they actually need. The answer isn’t one-size-fits-all. Your insurance obligations depend on a combination of factors, including:

Your business structure

The industry you operate in

The state (or states) where you do business

Whether you have employees

The contractual requirements imposed by your landlord, clients and lenders

Some insurance is legally mandated — you’re required by law to carry it, and operating without it can result in fines, penalties or worse. Other insurance isn’t technically required by law, but is effectively mandatory because you can’t sign a lease, win a contract or obtain a professional license without it. And some insurance falls into neither category but is financially prudent given the risks your business faces.

This guide walks through each category, explains the most common types of business insurance and maps specific requirements to common business types so you can identify what applies to your situation.

Tip

Our roundup of the best business insurance can connect you with leading insurers offering legally sound policies at competitive rates.

Insurance that’s legally required

Legally required insurance is mandated by federal or state law. Operating without it isn’t just risky — it’s a compliance violation that can result in fines, criminal penalties and personal liability for the business owner. Below are the insurance policies that are legally required for almost all business owners.

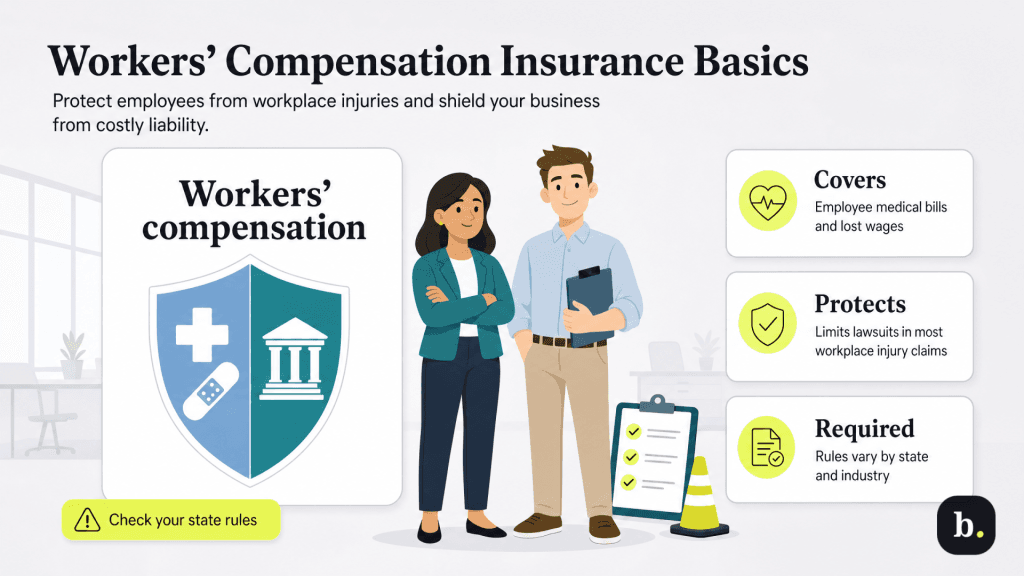

Workers’ compensation insurance

Workers’ compensation is required in nearly every state once your business has employees. It covers medical expenses and a portion of lost wages for employees who are injured or become ill in the course of their employment. It also protects employers — in most states, workers’ compensation is the exclusive remedy for workplace injuries, meaning employees who receive benefits generally cannot sue the employer for the same injury.

The specific threshold for when coverage becomes mandatory varies by state. Some states require it with your very first employee, while others set the threshold at two, three, four or five employees. Certain industries face stricter rules regardless of headcount — construction is the most common example, where many states require workers’ compensation coverage even for sole proprietors and business owners with no employees.

Penalties for non-compliance are severe and vary by state. They can include substantial fines (sometimes calculated on a per-day or per-employee basis), criminal misdemeanor or felony charges, stop-work orders that shut down your operations and personal liability for the business owner if an uninsured employee is injured on the job. Given the severity of these consequences, workers’ compensation should be at the top of your insurance checklist as soon as you hire your first employee.

A note on state variation: Texas allows employers to opt out of workers’ compensation coverage (known as non-subscription), but doing so removes important legal protections, including limits on employee lawsuits. In contrast, a small number of states — Ohio, North Dakota, Washington and Wyoming — operate monopolistic state funds, meaning employers must purchase workers’ compensation coverage through the state (with limited exceptions for self-insured employers). Always confirm your specific state’s requirements through your state’s department of labor or workers’ compensation board.

Unemployment insurance

Unemployment insurance is required at both the federal and state levels for businesses with employees. Unlike other types of business insurance, this isn’t a policy you purchase from an insurance carrier. It’s a payroll tax obligation funded through employer-paid taxes that support the unemployment benefits system.

At the federal level, the Federal Unemployment Tax Act (FUTA) imposes a tax on employers. At the state level, each state administers its own unemployment tax program (commonly referred to as SUTA or SUI) with its own rates and wage bases. State unemployment tax rates are experience-rated, meaning your rate is adjusted based on your history of former employees filing unemployment claims — the more claims, the higher your rate.

Registration with your state’s unemployment agency is required when you hire your first employee. Most payroll providers handle the ongoing tax calculation, withholding and reporting automatically.

State-mandated disability insurance

A small number of states require employers to provide short-term disability insurance to employees. Currently, California, Hawaii, New Jersey, New York, Rhode Island and Puerto Rico mandate this coverage. It provides partial wage replacement for employees who are unable to work due to a non-work-related illness or injury — distinct from workers’ compensation, which covers work-related conditions.

The funding mechanism varies by state. In some states, the cost is funded entirely through employee payroll deductions. In others, employers are required to contribute. And in some, the arrangement can go either way depending on the plan. If you operate in one of these states, confirm your obligations through the state’s disability program website or your payroll provider.

It’s also worth noting that several states have implemented or are implementing paid family and medical leave (PFML) programs, which may impose additional employer obligations. These programs are expanding, and the requirements differ significantly from state to state. Monitor developments in the states where you operate to stay compliant.

Commercial auto insurance

If your business owns or leases vehicles, commercial auto insurance is legally required just as personal auto insurance is required for personal vehicles. State minimum liability requirements apply, and your business must carry at least the minimum coverage mandated by each state where the vehicles operate.

An important nuance: Personal auto insurance policies typically exclude business use. If your employees drive their personal vehicles for work purposes — visiting clients, making deliveries, running business errands — their personal auto policies may not cover accidents that occur during business use. To address this gap, your business may need hired and non-owned auto (HNOA) coverage, which provides liability protection when employees use personal or rented vehicles for business activities.

Some types of insurance aren’t mandated by law but are required as a condition of doing business with specific parties. Landlords, clients, lenders and licensing bodies frequently require proof of certain coverages before they’ll sign a lease, award a contract, approve a loan or issue a license. For many small businesses, these contractual requirements make the following coverages effectively mandatory.

General liability insurance

General liability insurance covers claims of third-party bodily injury (e.g., a customer slips and falls at your business), property damage (your employee accidentally damages a client’s property) and advertising injury (claims of libel, slander or copyright infringement in your marketing materials). It’s the most foundational business insurance policy and the one most frequently required by third parties.

While general liability is not legally required in most states, it is required by virtually every commercial landlord as a condition of signing a lease, by many clients (particularly enterprise and government clients) as a condition of awarding a contract, and by many professional licensing boards and industry associations. A common baseline for general liability coverage is $1 million per occurrence and $2 million in aggregate. However, some contracts, clients and landlords may require higher limits depending on the nature of the business.

For most small businesses that interact with customers, operate from a leased space or work on contract for other businesses, general liability is non-negotiable.

Professional liability (errors and omissions) insurance

Professional liability insurance, also known as errors and omissions (E&O) insurance, covers claims arising from mistakes, negligence or failure to deliver professional services as promised. If a client alleges that your professional advice, design or work product caused them financial harm, professional liability coverage pays for legal defense costs and any resulting settlements or judgments.

Some states require professional liability for specific licensed professions — medical malpractice insurance for healthcare providers is the most well-known example, but requirements also exist for architects, engineers, real estate agents and other licensed professionals, depending on the state. Beyond legal mandates, many clients in industries like consulting, accounting, IT services, architecture and engineering require professional liability coverage as a contractual condition.

General liability insurance doesn’t cover professional services claims, so businesses that provide advice, expertise or specialized services need a separate professional liability policy.

Surety bonds

Surety bonds are not insurance policies in the traditional sense, but they’re frequently grouped with insurance requirements because they serve a similar risk-transfer function and are often obtained through insurance providers.

A surety bond is a three-party agreement that guarantees a business will fulfill its obligations. If the business fails to perform, the bond pays the harmed party. Many states require surety bonds for specific licensed professions and industries, including general contractors, auto dealers, freight brokers, mortgage brokers, notaries public and various other regulated occupations. The bond amount and requirements vary by state and license type.

Insurance requirements by business type

While the specific requirements depend on your state, contracts and individual circumstances, the following sections detail the insurance considerations and requirements most commonly associated with each major business type.

Home-based businesses

If you operate a business from your home, your homeowner’s or renter’s insurance policy almost certainly doesn’t cover your business activities. Most homeowner’s policies explicitly exclude business-related claims, business equipment beyond a low sublimit and liability arising from business operations conducted on the premises.

Depending on the nature and scale of your home-based business, you may need:

A home business endorsement added to your homeowner’s policy (appropriate for very small, low-risk operations)

A standalone business insurance policy (general liability and business property coverage designed for home-based businesses)

A full commercial insurance program (if your operation has grown beyond what a home business endorsement can cover)

If clients visit your home, general liability becomes particularly important. If you store significant business inventory or equipment at home, confirm that it’s covered — your homeowner’s policy’s personal property coverage likely won’t protect business assets.

Retail and brick-and-mortar businesses

Retail businesses operating from a physical location typically need the broadest range of standard business insurance coverages.

General liability is almost always required by the landlord and is essential for any business where customers enter the premises.

Commercial property insurance covers your inventory, fixtures, equipment and any tenant improvements you’ve made to the space.

Business interruption insurance covers lost income if a covered event (fire, storm, vandalism) forces you to close temporarily.

If you have employees, add workers’ compensation to the list. If you sell physical products, product liability coverage is important. It’s often included within your general liability policy, but if your products carry elevated risk (food, children’s products, electronics, health supplements), you may need higher limits or standalone product liability coverage. A business owner’s policy (BOP), which bundles general liability, commercial property and business interruption coverage, is a cost-effective starting point for most retail operations.

Service-based businesses

Businesses that sell services rather than physical products have a different risk profile, and professional liability (E&O) insurance is typically the most important coverage beyond general liability. If your business provides advice, designs, strategies or specialized expertise, the risk that a client alleges your work caused them financial harm is your primary exposure. General liability does not cover these claims.

Depending on your service type, you’ll also need:

General liability, as required by most landlords and clients

Workers’ compensation if you have employees

Cyber liability insurance if you handle client data

Businesses that provide IT services, manage client databases, process payments or handle sensitive personal information should treat cyber liability as a core coverage, not an optional add-on.

Construction businesses face some of the most extensive insurance requirements of any industry. General liability is universally required by project owners, general contractors and clients — you will not win work without it. Workers’ compensation is required in most states, with few or no exemptions for the construction industry, and many states extend the requirement to sole proprietors and business owners in construction trades.

Inland marine or contractor’s equipment coverage for tools and equipment that move between job sites

Surety bonds, a licensing requirement in many states

The specific requirements vary by trade, license type and the contracts you pursue, but construction businesses should expect to carry a broader insurance portfolio than most other small businesses.

Food and hospitality businesses

Restaurants, bars, cafes, catering companies and food manufacturers share a common set of insurance needs built around the risks inherent in food service and customer-facing hospitality. General liability, commercial property, workers’ compensation and business interruption form the baseline requirements. Product liability coverage is important for any business that prepares or serves food — a foodborne illness outbreak or contamination can result in significant claims.

If your business serves alcohol, liquor liability insurance is essential. Most states and landlords require it, and general liability policies typically exclude or limit coverage for alcohol-related incidents. Liquor liability covers claims arising from injuries or damages caused by intoxicated patrons — including incidents that occur after the patron leaves your establishment.

Healthcare and medical practices

Healthcare providers face a distinct insurance landscape centered on professional liability. Medical malpractice insurance is legally required in some states and practically required everywhere — no healthcare provider should practice without it. Malpractice coverage protects against claims alleging medical errors, misdiagnosis, improper treatment or failure to treat.

Beyond malpractice insurance, healthcare practices also need:

General liability

Workers’ compensation

Commercial property

Cyber liability

Cyber insurance is particularly important for healthcare businesses because of the sensitivity of protected health information (PHI) under HIPAA. A data breach involving patient records triggers notification requirements, potential regulatory fines and significant reputational damage. Cyber liability insurance covers breach notification costs, regulatory defense and related expenses.

E-commerce and online businesses

Online businesses sometimes assume they don’t need traditional business insurance because they don’t have a physical storefront. This is a misconception. If you sell physical products online, you have product liability exposure, whether you manufacture the products yourself or resell them from other sources. Some e-commerce platforms and fulfillment partners even require proof of general liability and product liability coverage as a condition of using their services.

Additionally:

Cyber liability insurance is increasingly essential for e-commerce businesses that collect customer payment information, personal data and account credentials. A data breach can trigger notification costs, regulatory investigations and lawsuits.

If you manage your own fulfillment, shipping and cargo insurance protects against loss or damage to products in transit.

If you have employees, the same workers’ compensation and employment-related requirements apply regardless of whether your business operates from a warehouse, a home office or a co-working space.

Insurance requirements summarized by business type

The following table provides a quick reference for common insurance needs by business type. Note that this is a general guide — your specific requirements may differ based on your state, contracts and individual circumstances.

Business Type

Common Insurance Needs

Home-Based

General liability, home business endorsement or standalone policy, business property

Retail / Brick-and-Mortar

General liability, commercial property, business interruption, workers’ comp, product liability

Service-Based

General liability, professional liability (E&O), workers’ comp, cyber liability

General liability, commercial property, workers’ comp, product liability, liquor liability, business interruption

Healthcare / Medical Practices

Malpractice and professional liability, general liability, workers’ comp, cyber liability, commercial property

E-Commerce / Online

General liability, product liability, cyber liability, shipping and cargo, workers’ comp

How to determine your specific insurance requirements

Because insurance requirements are driven by a combination of state law, industry regulations and contractual obligations, the ideal approach is to work through each source systematically. We recommend following these best practices to determine your specific insurance requirements via key sources.

Check your state’s requirements. Your state’s department of insurance, department of labor and workers’ compensation board are the authoritative sources for state-mandated insurance requirements. These agencies publish clear guidance on workers’ compensation thresholds, state disability requirements and any industry-specific mandates. If you operate in multiple states, you must comply with each state’s requirements.

Review your lease and rental agreements. Most commercial leases specify the types of insurance, minimum coverage limits and additional insured requirements the tenant must maintain. These requirements are non-negotiable conditions of the lease — failure to comply can be a lease violation.

Review your client contracts and RFPs. Many clients, particularly larger companies and government agencies, specify insurance requirements in their contracts and request for proposal (RFP) documents. These requirements often include minimum general liability limits, professional liability coverage, workers’ compensation verification, and sometimes umbrella or excess coverage.

Check professional licensing requirements. Some professions and industries require specific insurance or bonding as a condition of obtaining or maintaining a license. Check with your state’s licensing board for your profession or trade.

Consult a licensed commercial insurance agent or broker. An experienced commercial insurance professional can assess your specific situation, identify requirements and exposures you may not be aware of, and help you build a coverage program that meets all of your legal, contractual and risk management needs. This is particularly valuable when you’re setting up insurance for the first time or when your business is undergoing a significant change, such as adding employees, signing a new lease or entering a new market.

The right insurance to protect your business

The insurance your business needs is determined by a combination of legal mandates, contractual obligations and practical risk management. At a minimum, most businesses with employees need workers’ compensation and unemployment insurance. Most businesses with a physical location need general liability and commercial property coverage. Businesses that provide professional services typically need professional liability coverage. And virtually all businesses benefit from at least a basic general liability policy, regardless of size or structure.

Beyond the minimums, the right insurance program depends on your industry, your clients’ requirements, the specific risks your business faces and the financial consequences of an uninsured loss. Start with the legal requirements, layer in your contractual obligations and then evaluate what additional coverage makes financial sense given your risk exposure. The cost of comprehensive business insurance is almost always a fraction of the potential cost of an uninsured claim. Plus, the peace of mind that comes with knowing you’re properly protected allows you to focus on running your business rather than worrying about what could go wrong.

Adam Uzialko, the accomplished senior editor at Business News Daily, brings a wealth of experience that extends beyond traditional writing and editing roles. With a robust background as co-founder and managing editor of a digital marketing venture, his insights are steeped in the practicalities of small business management.

At business.com, Adam contributes to our digital marketing coverage, providing guidance on everything from measuring campaign ROI to conducting a marketing analysis to using retargeting to boost conversions.

Since 2015, Adam has also meticulously evaluated a myriad of small business solutions, including document management services and email and text message marketing software. His approach is hands-on; he not only tests the products firsthand but also engages in user interviews and direct dialogues with the companies behind them. Adam's expertise spans content strategy, editorial direction and adept team management, ensuring that his work resonates with entrepreneurs navigating the dynamic landscape of online commerce.