When you apply for a business credit card, one of the first decisions you’ll face is which tax identification number to provide: your Social Security number (SSN) or your Employer Identification Number (EIN). The choice may seem administrative, but it can affect your personal liability, your credit and even whether you’ll be approved at all. For many business owners, the answer isn’t entirely a matter of preference — it depends on their business structure, the card issuer’s requirements and the type of card they’re pursuing.

This guide explains how each number is used on a business credit card application, the practical differences between them and when an SSN, EIN or both may come into play.

What is an SSN, and how is it used on business credit card applications?

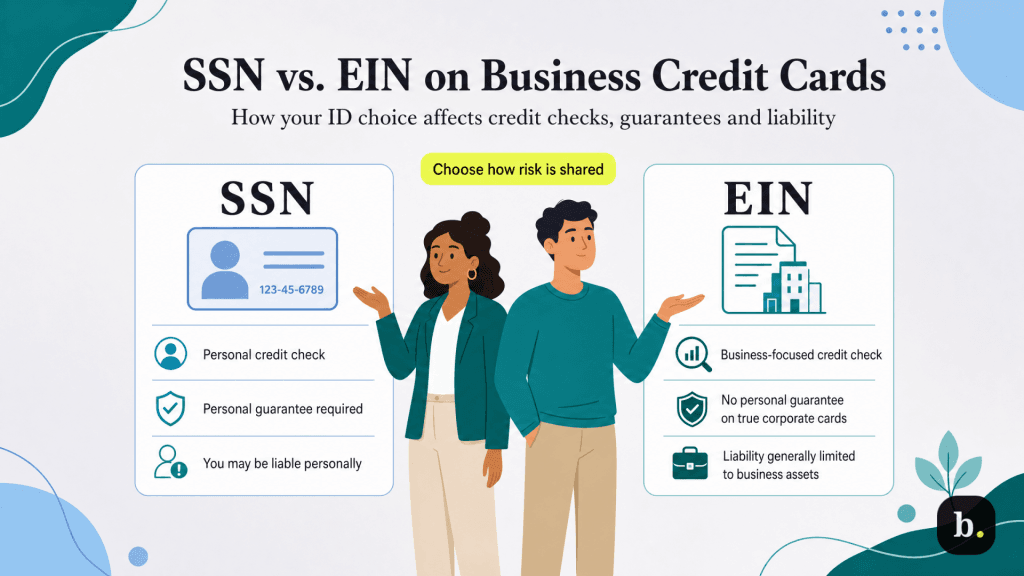

Your Social Security number is a nine-digit identifier issued by the Social Security Administration to track your personal income and benefits. On a business credit card application, issuers typically use your SSN to pull your personal credit report, verify your identity and assess your creditworthiness as an individual.

Most small business credit cards require an SSN, even if your business has its own EIN. The reason is the personal guarantee: most business cards are unsecured, and issuers want a specific person to be legally responsible for the debt if the business can’t pay it. Your SSN is how they tie that obligation to you.

How does an SSN affect your personal credit and liability?

Applying for a business credit card with your SSN usually results in a hard inquiry on your personal credit report. That can cause a small, temporary drop in your credit score, although it’s typically short-lived.

The bigger consideration is the personal guarantee. If the business can’t repay the debt, you’re still on the hook for it. Depending on the circumstances, creditors may be able to pursue your personal assets if the account falls seriously behind or goes into default.

Your personal credit may also be affected after you’re approved. Some issuers report business card activity to the personal credit bureaus, while others report only missed payments, serious delinquencies or defaults. Because reporting practices vary, it’s worth checking your issuer’s policy before you apply.

Who typically uses an SSN on a business credit card application?

Sole proprietors commonly apply for business credit cards using their SSN because they are not legally separate from their businesses. In fact, when you apply for a business credit card as a sole proprietor, an SSN is usually the primary tax identification number issuers use to evaluate your application. Even if you’ve obtained an EIN for tax or banking purposes, most traditional business card issuers still require an SSN as part of the application process.

Many LLC owners, freelancers, independent contractors and other small business operators also provide an SSN when applying for a business credit card, even when they have an EIN. Chase, for example, says it does not offer business credit cards that require only an EIN.

Even when a business has its own EIN, most traditional card issuers still want an SSN as part of the application process. Personal credit history and personal guarantees remain a big part of how those approval decisions are made.

What is an EIN, and when can you use it?

An Employer Identification Number (EIN) is a nine-digit number the IRS assigns to a business for tax purposes — essentially a Social Security number for your company. Banks and other financial institutions use it to identify your business and evaluate whether it qualifies for services such as business loans and credit cards.

An EIN can be useful for taxes, banking and establishing your business, but it usually won’t replace your SSN on a credit card application. Most traditional business cards still require both. True EIN-only approval is generally limited to corporate cards that evaluate the business itself rather than the owner.

How do you obtain an EIN?

The easiest way to get an EIN is through the IRS’s online application. In most cases, you’ll receive your EIN immediately after completing the form, and there’s no fee to apply.

You’ll identify yourself as the “responsible party” and provide information such as your SSN or ITIN, business name, business structure and principal business activity.

Sole proprietors aren’t required to have an EIN unless they hire employees or meet certain other IRS requirements. However, obtaining one can help separate business and personal finances and present a more established profile to vendors, lenders and other business partners.

Sole proprietors can often

open a business bank account without an EIN by using their SSN instead. However, some business owners choose to obtain an EIN anyway to avoid sharing their SSN with customers, vendors and financial institutions.

What is an EIN-only business credit card, and who qualifies?

EIN-only cards — those that don’t require a personal guarantee and may not require an SSN from the applicant — are almost always corporate cards rather than traditional small business credit cards. Many are offered by fintech companies such as Brex, Ramp, BILL Divvy, Rho and Stripe. Instead of evaluating your personal credit, these issuers underwrite your business directly, looking at factors such as cash balances, revenue, transaction history and, in some cases, your business credit score.

The catch is that these cards aren’t available to every business. Most providers expect applicants to have a registered U.S. entity, a business bank account and an established business with revenue or cash reserves. Sole proprietors typically don’t qualify for true EIN-only corporate cards.

Key differences between using an SSN and EIN on a business credit card application

At first glance, the difference between using an SSN and an EIN may seem administrative. In reality, it can affect your personal credit, your liability for the debt and what happens if your business runs into financial trouble. While many business owners provide both numbers during the application process, the way issuers use them can vary significantly.

Here’s how those differences play out in practice.

Impact on your personal credit

- SSN: When you apply for a traditional business credit card using your SSN, the issuer will typically pull your personal credit report as part of the approval process. Depending on the issuer, the account may also appear on your personal credit report or be reported if you miss payments or default on the debt.

- EIN: With a true EIN-only corporate card, your personal credit generally isn’t part of the approval process. Because the issuer is looking at the business instead, the account typically doesn’t show up on your personal credit report.

Personal guarantee requirements

- SSN: Most traditional small business credit cards require a personal guarantee. That means you’re personally agreeing to repay the debt if the business can’t.

- EIN: Corporate cards are usually set up differently. Instead of asking the owner to personally guarantee the account, the issuer relies on the business’s finances when making approval decisions.

Business default liability

- SSN: If you’ve signed a personal guarantee, the card issuer can pursue you personally for unpaid business debt. Depending on the circumstances, that may put personal assets at risk.

- EIN: Without a personal guarantee, the issuer’s recourse is generally limited to the company and its business assets.

Which should you use: SSN or EIN?

If you’re trying to decide between using an SSN or EIN on a business credit card application, the answer may be simpler than you think. For many small business owners, it isn’t really a choice. Most traditional business credit cards require an SSN, even if your business also has an EIN.

The decision becomes more relevant if you’re considering an EIN-only corporate card. In that case, your business structure, financial profile and willingness to sign a personal guarantee all come into play. Here’s what to consider:

- Business structure: Sole proprietors will generally need to use an SSN when applying for a business credit card. LLCs and corporations have more options. While many still apply for traditional business cards that require an SSN and personal guarantee, some may also qualify for EIN-only corporate cards.

- Business financial profile: If your business is new or doesn’t have much credit history of its own, traditional card issuers will usually look closely at your personal credit. Corporate card issuers take a different approach. They’re often more interested in how the business is performing, including factors such as revenue, cash reserves and banking activity.

- Liability: For many owners, the biggest distinction isn’t the tax identification number itself — it’s the personal guarantee. If you’re comfortable backing the account personally, a traditional business credit card may provide the broadest range of options. If avoiding personal liability is a priority and your business qualifies, an EIN-only corporate card may be worth exploring.

An EIN can help establish your business's identity and build

business credit, but it usually doesn't replace your SSN on a business credit card application. Most traditional issuers still require an SSN to verify your identity, review your personal credit and support a personal guarantee.

Can you apply with an EIN and no personal guarantee?

Yes, but it’s much less common than many business owners realize. Most traditional business credit cards require both an SSN and a personal guarantee. The primary exception is a category of products known as corporate cards.

Traditional issuers such as Chase and American Express build their small business credit cards around personal credit and a personal guarantee. Corporate card providers such as Brex and Ramp take a different approach, evaluating the business itself rather than the owner’s personal credit history.

That’s what makes EIN-only approval possible. It isn’t a feature you can opt into when applying for a traditional business credit card — it’s a fundamentally different type of product.

What businesses need to qualify

Because corporate card issuers are evaluating the business rather than the owner, they want evidence that the company can support the credit line on its own. Requirements vary by provider, but most look at factors such as revenue, cash reserves, banking activity and overall financial stability. Depending on the issuer, you may also be asked to provide financial documents such as a cash flow statement or profit-and-loss statement during the application process.

Most businesses that qualify for EIN-only corporate cards have a formal business structure, such as an LLC or corporation, along with a business bank account. Sole proprietors usually don’t qualify because the business and owner are treated as the same legal entity.

Requirements vary by provider. Some publish their set minimum qualifications, while others review businesses on a case-by-case basis. Since those requirements can change, it’s worth checking directly with the card provider before you apply.

One important tradeoff to consider

There’s another difference to keep in mind: many corporate cards are charge cards rather than traditional credit cards. That means the balance must be paid in full each billing cycle instead of being carried month to month.

If your business occasionally needs to revolve a balance or finance larger purchases over time, a traditional business credit card may offer more flexibility.

Understanding your options

For most small business owners — and nearly all sole proprietors — the answer is fairly straightforward. Applying with an SSN is both the default and the practical reality because that’s what traditional business credit cards require.

The EIN-only route exists, but it’s generally limited to corporate card issuers that evaluate the business rather than the owner’s personal credit. Those products can help separate business and personal liability, but they typically require an established business, a formal business entity and sufficient financial resources to qualify.

If avoiding a personal guarantee and creating more separation between your personal finances and business debt are priorities, an EIN-only corporate card may be worth exploring. For everyone else, a traditional business credit card that uses your SSN is usually the most accessible way to access financing, separate business spending and begin building business credit.